Logitech’s quarterly revenue soared 75% as the computer products maker continued to profit from the work-at-home shift exacerbated by the coronavirus pandemic.

Logitech’s (LOGI) second-quarter sales of fiscal 2021 surged 75% to $1.26 billion year-on-year, exceeding the Street consensus by $414 million. This marked the first time its quarterly revenue shot past the billion-dollar mark. Non-GAAP operating income jumped 295% to $354 million in 2Q versus the same period last year. Non-GAAP EPS grew 274% to $1.87, compared to $0.50 in the same quarter a year ago. The EPS figure beat analysts’ expectations by $1.29.

On the back of the robust results, Logitech raised its 2021 outlook to between 35% and 40% sales growth in constant currency, and a range of $700 million to $725 million in non-GAAP operating income. According to the previous outlook, it expected between 10% and 13% sales growth in constant currency, and a range of $410 million to $425 million in non-GAAP operating income.

“The growth trends that drive our business have accelerated as society adjusts to its new reality. The organization leaders I speak to envision people increasingly working from multiple locations, a hybrid work culture that is emerging as the norm,” said Logitech CEO Bracken Darrell. “And at home, the rise of gaming as a spectator and participant sport continues with no end in sight. Our products are essential to helping customers work, play and create wherever they are. Logitech is well positioned for long-term growth.”

At the end of the second quarter, cash flow from operations amounted to $280 million, compared to $107 million in the same period a year ago.

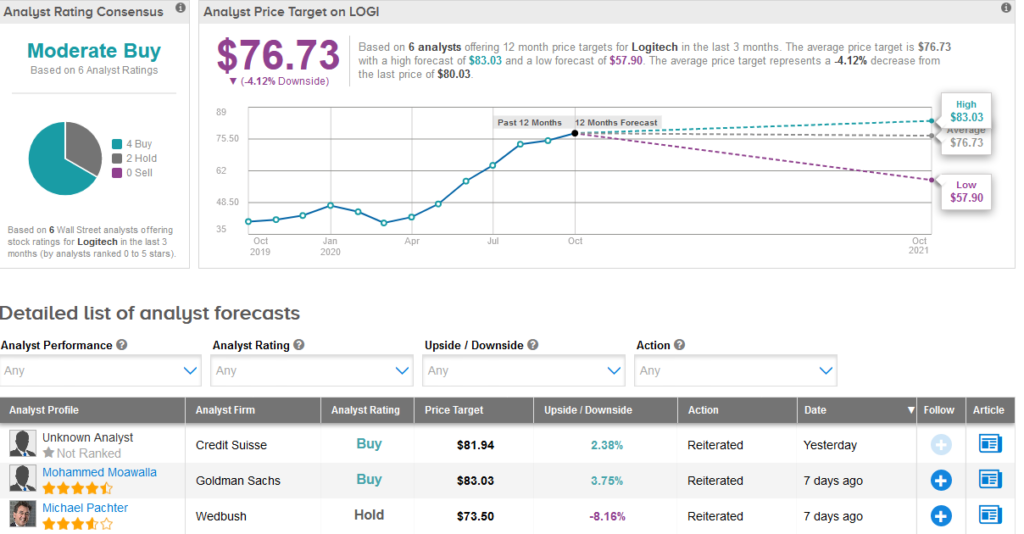

Shares in Logitech have more than doubled since hitting a low in mid-March and are now up 67% since the start of the year. In light of the stock’s outperformance, the $76.73 average analyst price target implies 4.1% downside potential in the next 12 months.

Last week, Wedbush analyst Michael Pachter reiterated a Hold rating on the stock with a $73.50 price target (8% downside potential), saying that the stock’s valuation is “full” and room for multiple expansion is limited.

“Logitech’s consistent earnings growth with investor-friendly capital allocation should support shares of LOGI near the high-end of its historical range, given the boost from quarantines,” Pachter wrote in a note to investors. “As people continue to work from home to prolong safety, we expect demand to remain elevated for Logitech’s PC peripherals to enhance home offices, and Gaming to enhance home entertainment.”

Looking ahead, “as people eventually return to the office, but with limited capacity or desire to travel in the coming months, we expect Video Collaboration products that enhance workers’ ability to attend conferences and meetings remotely to continue to benefit,” the analyst added.

The rest of the Street is cautiously optimistic on the stock’s outlook. The Moderate Buy analyst consensus brings together 4 Buys versus 2 Holds. (See Logitech stock analysis on TipRanks)

Related News:

Visa Nabs Strategic Stake In UK Fintech Company GPS

Halliburton 3Q Sales Miss The Street; Shares Decline

AMD Could Ink $30B Xilinx Deal As Soon As Next Week- Report

Questions or Comments about the article? Write to editor@tipranks.com