Since Donald Trump’s election win in November last year, Lockheed Martin stock (LMT) has been on a gradual descent, drifting from its 52-week high as concerns over tighter government spending and tariff clouds darkened its export prospects. The specter of the Musk-run GOGE trimming the fat, especially in areas where the U.S. government is charged outrageous amounts by contractors, has unnerved investors.

Yet, beneath this turbulence, Lockheed’s unique strengths, like its deep government ties and critical role, form a shield against such risks. Far from faltering, the company is poised to thrive. At the same time, the stock is now trading at a valuation that screams bargain-basement opportunity. I’m bravely bullish on a defense stock that is well-placed to capitalize on brewing geopolitical instability.

Tariffs Tamed: Lockheed’s Quiet Advantage

Lockheed Martin’s global footprint, with 26% of last year’s revenue coming from exports, might suggest tariff vulnerability. Still, President Trump’s 90-day pause on reciprocal tariffs announced yesterday, reverting rates to the 10% baseline set on April 5, softens the blow.

For exports, its linchpin F-35 program operates through Foreign Military Sales (FMS), where the U.S. government inks deals with allies like Japan or the UK. Many don’t know that these contracts, often fixed years ahead, dodge foreign tariffs, as importing nations prioritize security over trade spats.

Even as the EU, now at 10%, weighs 25% retaliatory duties on $23 billion of U.S. goods, defense gear historically slips through unscathed in such cases, which is a diplomatic perk Lockheed will bank on.

Of course, imports face the 10% baseline from the EU post-pause, with steel and aluminum still at 25%, but Lockheed’s playbook mitigates this. Long-term supplier deals, like those with Leonardo (DRS) for F-35 avionics, lean on fixed pricing or escalation clauses, a strategy that, if you recall, dulled 2018’s tariff sting. With critical minerals exempted in early 2025 and a hefty domestic sourcing shift (60% of F-35 content is U.S.-made), the 10% tariff is nothing to be bothered for a firm with $159 billion in backlog cushioning its books.

But what indeed fortifies Lockheed here is its geopolitical leverage. China’s rare earth export ban, set last week, for instance, throttles supply chains, and with each F-35 needing 920 pounds of these scarce materials, the pressure will be undeniable. Then again, this dependence elevates Lockheed’s stature, as its role in countering China’s move makes it a linchpin in Western security, driving demand even as costs rise.

Primed for a Defensive Renaissance

Now, it’s true that DOGE’s budget-slashing shadow looms large, but I believe Lockheed’s recent victories pierce the gloom. Last month brought a $13.3 million tweak to Lockheed’s Long-Range Anti-Ship Missile deal, followed by $54.2 million for submarine warfare tech in April, superb wins of a thriving pipeline. The F-35, fueling nearly 30% of sales, carries a backlog reaching 2040, with 165 jets delivered last year alone. Also, Trump’s pledge of $2.5 trillion in defense spending over five years to face down China and Russia from earlier this week mirrors his first-term Pentagon lift, which proved a strong tailwind for Lockheed.

Then you have Europe’s $841 billion “REARM Europe” plan, which throws more coal on the fire, with F-35s and missile systems like the Patriot PAC-3 topping wish lists. On top of that, Taiwan’s jitters over Trump’s “pay for protection” stance sparked F-35 talks, while Canada’s 88-jet order review last month feels more like saber-rattling than retreat. Lockheed’s one-of-a-kind ability to thrive during times of increased global tension (think Russia’s Ukraine invasion boosting NATO orders) positions it as a profiteer, not a victim.

Dividend Gem at a Bargain

From its 52-week high of ~$619, Lockheed’s stock has retreated by about 25%, pushing its forward P/E to just 17x, well below its five-year average of about 20x. Given that this occurred when Lockheed was set to benefit tremendously, I find the current valuation a notable bargain.

In the meantime, the stock appears particularly appealing for dividend growth investors following its lengthy decline. The stock trades at a 3% yield, backed by a 22-year streak of unbroken increases. By 2028, LMT will claim dividend aristocrat status (25+ years), forming a beacon for income funds, which could also prove a valuation tailwind as certain institutions pile in.

Is LMT a Good Stock to Buy Now?

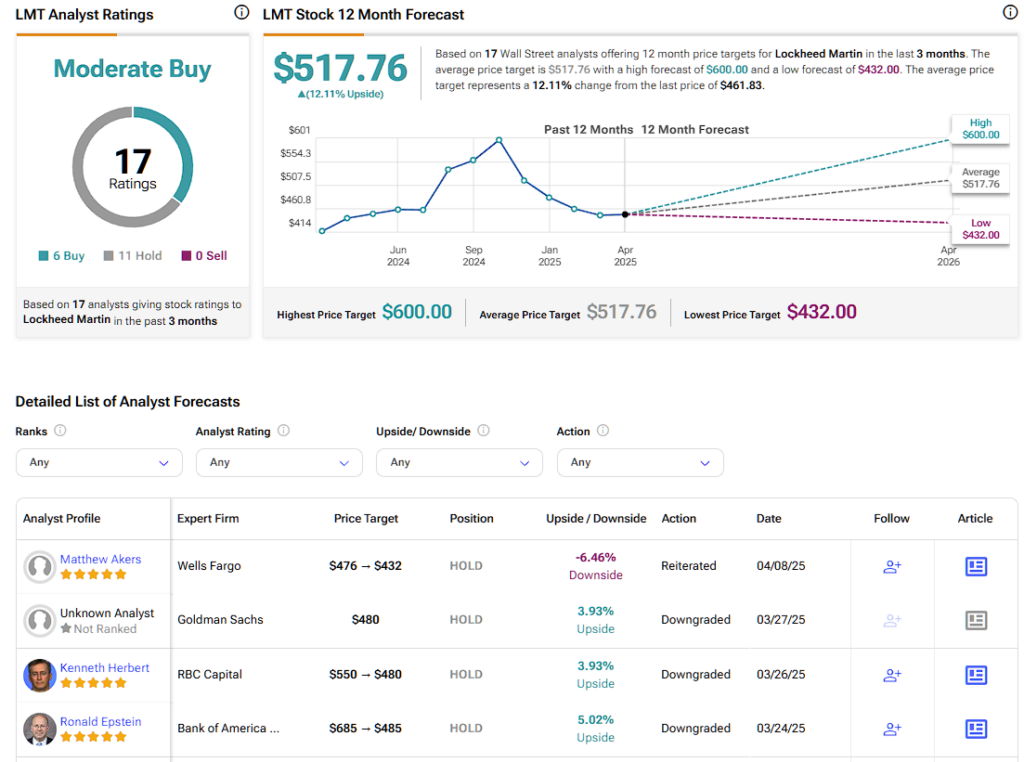

On Wall Street, analysts appear relatively bullish on LMT stock. The stock has a Moderate Buy consensus rating based on six Buy and eleven Hold ratings over the past three months. LMT’s average price target of $517.76 implies a ~12% upside potential over the next twelve months.

Stalwart Stock Serves as Income Generator

Lockheed Martin’s stock has slumped since Trump’s election, with Wall Street daunted by tariff fears and DOGE’s budget axe. However, its fortress stands firm. With tariffs tamed, defense wins stacking up, and a massive spending pledge in today’s geopolitical environment, the defense giant is primed to thrive. At current prices, Lockheed is offering a 3% yield and is trading 17x forward P/E, creating a bargain opportunity that blends growth, income, and safety in today’s Trump-fueled tariff storm.