Sometimes, the best stock market bargains hit you when you’re not looking for them. You wouldn’t consider a $3,000 share price to be a bargain – and neither would anyone else, including company management.

That brings us to the stock split, one of the corporate world’s great tricks. Companies use it to reduce their share price without altering their market cap valuation. The split gives every shareholder a specified number of shares for each share they already own – so a 10-to-1 split will turn a 100-share holding into 1000 shares. Since the holding has the same value, each share is now worth 1/10 the previous price. Stock splits effectively reduce the share price, making the stock more affordable to a larger base of investors.

For investors, splits open up new opportunities. Stock prices can rise for many reasons, but a high share price is typically a flashing neon indicator of a quality company. So, when shares with very high prices – we’re talking 4-digit prices – split, it’s a chance to buy in at a new, lower price – and hold on to reap long-term gains. Statistical studies have shown that post-split stocks will significantly outperform the S&P 500 in the year following the split action.

Some of the Street’s top analysts are bullish on a couple of recent stock-split plays, saying it’s time to load up on them. We’ve used the TipRanks database to gather the latest scoop on both stocks, finding that each has a Buy consensus rating and double-digit upside potential. Here are the details.

Chipotle Mexican Grill (CMG)

First up is Chipotle, the Mexican-styled fast-food chain. Chipotle brings a recognizable brand image to the table, an important advantage in the fast-food world. The company has a reputation for quality food, which goes far to support the brand image. Chipotle operates over 3,400 locations, with stores in all 48 states of the continental US, as well as in Canada and Europe. The chain’s largest footprint is in California, where it has 478 stores, and in Ohio and Florida, where it has 243 and 242 respectively. Chipotle also offers catering and group order services.

Mexican food is popular across the US, and Chipotle has gained a loyal customer base. The company’s stock has seen the benefits, and in June of this year it was trading at close to $3,200 per share. That made CMG one of Wall Street’s most expensive stocks, and management announced a 50-to-1 stock split in response. That split took effect on June 26, and made headlines – it was one of the largest such splits in Wall Street history. Company management said explicitly that they wanted to make the shares more affordable for investors and employees.

After the split took effect, the stock price was recalculated at approximately $64. Shares are down 20% since then. The share price decline comes as online customers have complained that the company reduced portion sizes while increasing prices, an indication that persistent inflation remains a risk in the fast-food business.

On the financial side, Chipotle is expected to release its Q2 results today after the markets close. Analysts are expected to see a top line of $2.94 billion, and earnings of 32 cents per share. Chipotle’s quarterly earnings have been consistently above $2 billion for the last two years, with the previous release, 1Q24, showing a top line of $2.7 billion. That was up almost 14% year-over-year and beat the forecast by $30 million. The Q1 earnings were released prior to the stock split, and were reported as $13.37 per share by non-GAAP measures; adjusted for the split, that figure is 27 cents per share, or 3 cents better than had been anticipated.

Chipotle’s solid earnings were bolstered by a 7% year-over-year increase in comparable restaurant sales, and the company reported an increase in the operating margin from 15.5% to 16.3%.

Covering this stock from Deutsche Bank, 5-star analyst Lauren Silberman takes a bullish stance. She is upbeat on the company’s Q2 projections, and writes, “Sentiment on CMG remains positive as CMG is likely to beat in 2Q and fundamentals remain strong amidst a challenging restaurant backdrop, though we believe positioning is less crowded than the last couple of quarters given expectations for moderating SSS exiting the quarter and into 3Q. We expect 2Q SSS to be the highest of the year, though traffic and SSS should remain strong in 2H, supported by a strong innovation and marketing pipeline (likely to bring back Brisket for the first time in three years), while throughput remains one of the most meaningful multi-year traffic drivers.”

For the near-term, Silberman expresses confidence in continued growth: “We continue to have conviction in the near-term and long-term outlook and see a path to upside to numbers on better-than-expected SSS and restaurant margin (DB/sellside incremental margins imply ~33% flow-through vs ~40% guide for model).”

These comments back up the analyst’s Buy rating on CMG, and her $72 price target points toward a one-year upside potential of more than 37%. (To watch Silberman’s track record, click here)

Overall, Chipotle’s stock gets a Moderate Buy rating from the analyst consensus, based on 24 recent analyst reviews that include 17 Buys to 7 Holds. The shares are priced at $51.73 currently, and the $68.11 average target price suggests a gain of 32% on the one-year horizon. (See CMG stock forecast)

Broadcom (AVGO)

Next up is Broadcom, one of the industry leaders in the semiconductor chip sector. From its Palo Alto base in Silicon Valley, Broadcom has built up more than 60 years of experience in high tech – and with its market cap of nearly $760 billion, counts itself as the world’s third-largest chip company. Broadcom’s annual revenues – at $42.6 billion for the four quarters from 2Q23 to 1Q24, placing it in fifth place among its peers.

Broadcom is a global company, with a reputation for engineering excellence in a demanding field. The company’s product lines include data center switches and routers; cable modems; ethernet NICs, filters, and amplifiers; fiber optic solutions; wireless connectivity solutions; embedded processors – it’s a long list. The company’s products have found wide acceptance in the data center, wireless service, and cybersecurity fields, among others.

Like Chipotle above, Broadcom was long known for its high stock price, and in mid-June, with the share price running near $1,700, the company announced a 10-to-1 split. The split was executed on Friday, July 12, and was reflected in trading starting on Monday, July 15, when the share price came down to approximately $170.

In addition to the split, Broadcom announced fiscal 2Q24 revenues of $12.49 billion. This was up an impressive 43% year-over-year, and came in $480 million higher than had been anticipated. The company’s non-GAAP EPS was reported as $10.96 pre-split; post-split, this was adjusted to $1.10 per share, or a penny over the forecast.

This high-end tech stock has caught the attention of JPMorgan analyst Harlan Sur. Sur, who is rated in the top 1% of the Street’s analysts by TipRanks, notes Broadcom’s market share leadership in multiple chipset fields, and sees the company’s sheer size as a tangible asset. He writes of the chip company, “In Datacenter/AI Ethernet switching/routing chipsets, Broadcom continues to maintain its #1 market share (~80% of $5-7B market) and very high barriers to entry as the team continues to drive a 2x Moore’s Law like performance boost with its Tomahawk switching chipset… Very few competitors have the R&D scale/IP to be able to match the cadence/capabilities of Broadcom’s networking silicon franchises and the company continues to stay one/ two steps ahead of its competitors.”

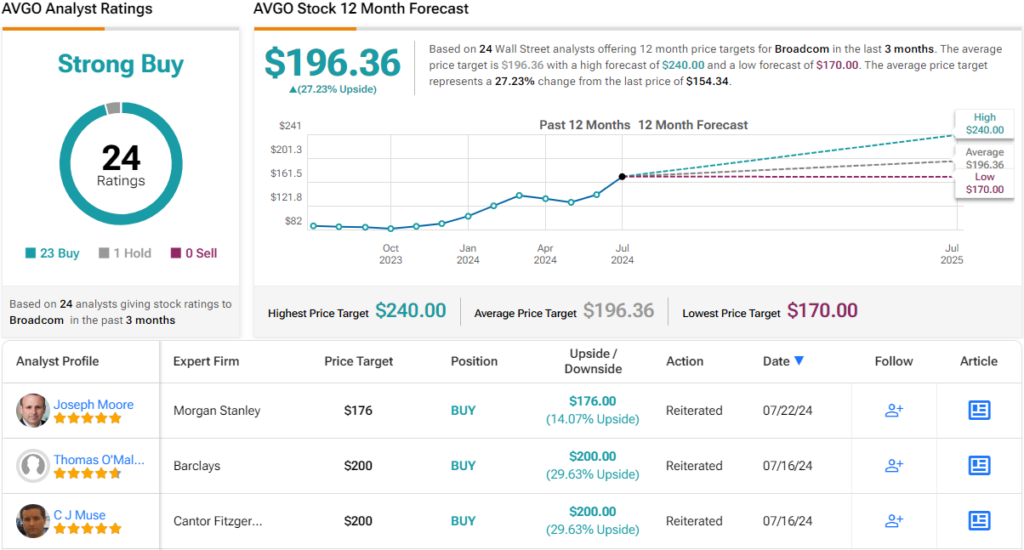

Sur goes on to rate AVGO shares as Overweight (i.e. Buy), and his price target, now set at $200, implies a 12-month upside for the shares of ~30%. (To watch Sur’s track record, click here)

All in all, Broadcom has earned a Strong Buy consensus rating on Wall Street, based on 24 analyst recommendations that feature a lopsided split of 23 Buys to 1 Hold. The stock is trading at $154.20 and its $196.36 average price target indicates potential for a ~27% increase in the coming year. (See AVGO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.