With a focus on revamping mission-critical infrastructure, Limbach Holdings (LMB) has observed staggering growth of over 1150% in its share value over the past three years – outpacing even NVIDIA (NVDA). This impressive performance is attributed to robust operating outcomes, high-margin business expansion, and lucrative M&A activity. The company has acquired Consolidated Mechanical, Inc. and Kent Island Mechanical to enhance its footprint and service offerings. Meanwhile, its latest financials show robust results, with revenue and EBITDA beating expectations. With these strategic moves and positive financial outcomes, Limbach is creating a strong position in the niche of building systems solutions. Investors take notice!

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Limbach Aggressively Expands its Footprint

Limbach Holdings is a building systems solution company that provides mechanical, electrical, and plumbing infrastructure to critical facilities across various sectors, such as healthcare and data centers. The company operates in two segments: General Contractor Relationships and Owner-Direct Relationships.

The company has announced the acquisition of Consolidated Mechanical, Inc., for an initial price of $23 million. Consolidated’s services include mechanical, millwright, and plumbing construction, maintenance, and outage services to industrial sector owners of complex process systems. Beginning in 2025, Consolidated is expected to generate an annualized revenue of about $23 million. This acquisition boosts Limbach’s operations in the industrial sector, especially in power generation, manufacturing, and other related markets in Kentucky, Illinois, and Michigan.

This follows the successful acquisition of Kent Island Mechanical for a purchase price of $15 million. Kent is a leading service provider for maintaining complex building systems. This acquisition expands Limbach’s design, engineering, maintenance, and emergency mechanical solutions capabilities. The acquisition is anticipated to contribute approximately $30 million in revenue and over $4 million in EBITDA annually beginning in 2025.

These acquisitions, funded from available cash, align with Limbach’s strategic growth plan. The company focuses on enhancing its service offerings and expanding its footprint. It seeks to maintain a pace of two to three acquisitions per year.

Limbach Sees Higher Revenue

The company recently posted results for Q3 2024. Revenue of $133.92 million, up 4.8% from the same period in 2023, exceeded analysts’ expectations by $4.42 million. Organic growth was driven by consolidation with existing customers and the continued vertical demand. At the same time, the acquisition of Kent Island Mechanical has added to market share growth in the Greater Washington, D.C. metro region. This expansion adds to the capacity while gaining efficiencies and incorporating new customers into the ODR business, which has experienced a 41.3% increase in revenue.

Gross profit also increased due to a higher revenue and margin segment from ODR. SG&A saw an increase of $2.8 million due to increased payroll and stock-based compensation expenses. Net income increased by 4.1%, with adjusted EBITDA seeing a significant rise of 27.2% and earnings per share (EPS) of $0.62, beating the consensus estimate by $0.10.

As of the quarter’s end, the company reported cash and cash equivalents amounting to $51.2 million, current assets of $217.1 million, and current liabilities of $138.2 million. The current ratio demonstrated a slight increase from the previous period, moving from 1.50x at the end of 2023 to 1.57x. The company’s working capital also increased by $7.1 million, reaching $78.9 million. On the liabilities side, $10.0 million was owed in revolving credit facility borrowings and $4.3 million for standby letters of credit.

FY 2024 Guidance Raises the Bar

Following Limbach’s third-quarter earnings, LMB’s management has updated its financial guidance for FY 2024. The projected revenue range has been increased from the previous estimate of $515 million – $535 million to a projection of $520 million – $540 million. Furthermore, the anticipated adjusted EBITDA has also been raised from $55 million – $58 million to $60 million – $63 million.

Bullish Sentiment Over LMB

The stock has been on an upward trend, recently climbing over 47% in the past three months. It trades near the high end of its 52-week price range of 52-Week Range of $35.24 – $107.00 and shows positive price momentum as it trades above the 20-day (96.82) and 50-day (88.37) moving averages. In a reflection of its above-average growth rates, it trades at a premium to industry peers, with a P/S ratio of 2.12x compared to the Industrials sector average of 1.64x,

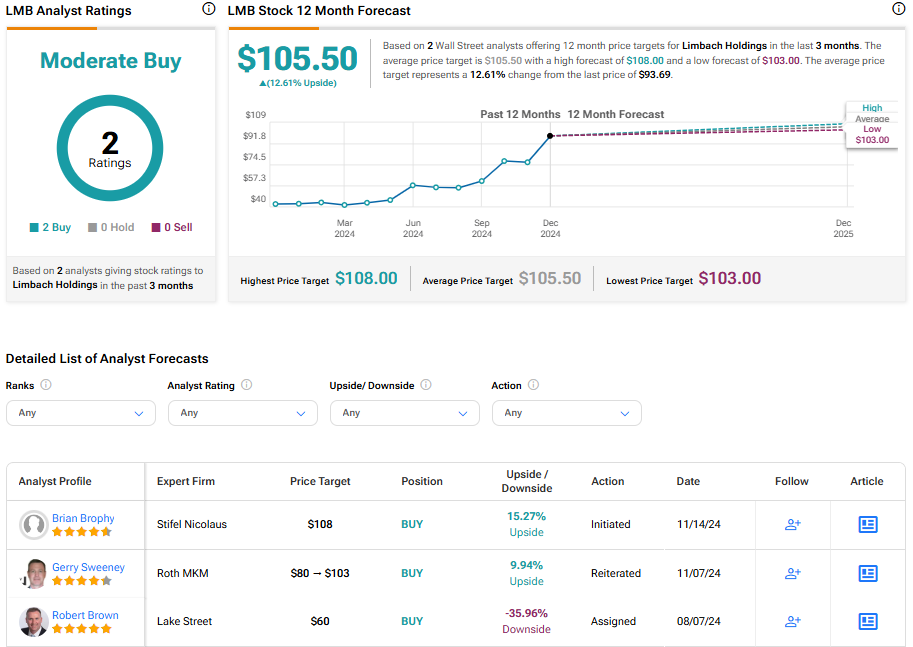

Analysts covering the LMB stock have been bullish. For instance, Stifel analyst Brian Brophy, a four-star analyst according to Tipranks’ ratings, recently initiated coverage of Limbach with a Buy rating and a $108 price target. Brophy noted the company’s strong free cash flow conversion and expectations of organic growth accelerating in 2025.

Two analysts recommend Limbach Holdings as a Moderate Buy overall. The average price target for LMB stock over the next 12 months is $105.50, representing a potential 12.61% upside from current levels.

Limbach in Review

The remarkable growth of Limbach’s share value over the past three years can be credited to its strategic acquisitions, high-margin business expansion, and strong financial outcomes. The company’s acquisitions have considerably expanded its service offerings and geographical presence in the industry. Furthermore, Limbach has demonstrated a solid financial performance with expectations to continue on an upward growth trajectory. Limbach Holdings is a compelling option in the construction industry, grabbing the attention of savvy investors.