Leaf Group’s long-term shareholder, Boyle Capital Opportunity Fund, has rejected the proposed buyout offer of $8.50 per share from education and media company, Graham Holdings.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Leaf Group’s (LEAF) shareholder Boyle said in a letter to the company’s board that the $8.50 per share offer is “grossly inadequate” and significantly undervalues the company. Boyle Capital added that the offer will not be able to compensate shareholders as the company’s segments are at inflection points. Meanwhile, Leaf Group has significant growth opportunities in the tokenized art market to capitalize on.

Notably, Graham (GHC) had agreed to purchase consumer internet company, Leaf Group, for a cash deal worth $323 million on April 5. The deal is expected to close in June or July, but the company would need the approval of Leaf Group shareholders.

On that day, Leaf’s chairman of board of directors, Deborah Benton, said, “Through this transaction, we are pleased to maximize value and deliver a significant, immediate cash premium to Leaf Group’s shareholders.” Benton added that “After thoroughly reviewing the strategic alternatives available to Leaf Group, the Board of Directors concluded that this all-cash premium transaction with Graham Holdings achieved the Board’s long-term objective of fully recognizing the value of the business and delivers immediate and substantial cash value to our shareholders.” (See Leaf Group stock analysis on TipRanks)

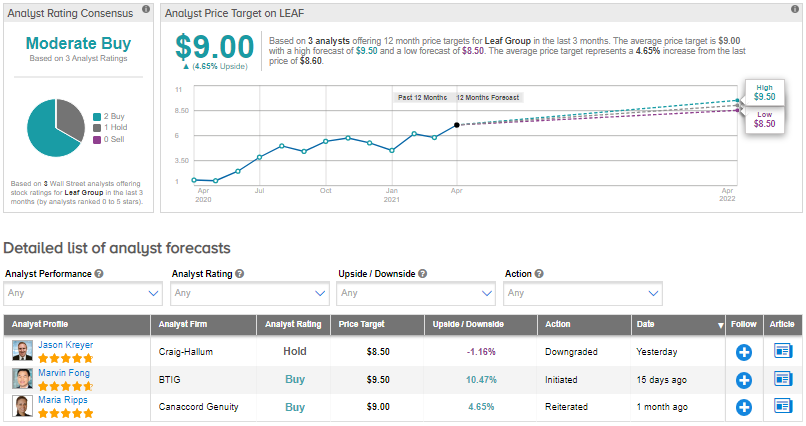

On April 6, Craig-Hallum analyst Jason Kreyer downgraded Leaf Group stock to Hold from Buy, but lifted the price target to $8.50 (1.16% downside potential) from $7.50. The analyst believes that the Leaf-Graham deal should benefit the Leaf’s shareholders.

Meanwhile, the Street has a Moderate Buy consensus rating on the stock based on 2 Buys and 1 Hold. The average analyst price target of $9 implies upside potential of about 4.7% to current levels. Shares have gained 566.7% in one year.

Related News:

QuickLogic Gains Over 5% On Distribution Agreement With Mouser

Maxeon Slips 6% On Weaker-Than-Expected 1Q Revenue Outlook

Signet Acquires Rocksbox, Expands Services Offerings