Micron (NASDAQ:MU) is about ready to deliver its November quarter (FQ1) report, which will be released today once the market action comes to a halt.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Ahead of the print, a theme appears to be developing on Wall Street. There’s fairly widespread agreement that the memory giant is about to dial in a strong readout, hampered by a guide that will miss analyst expectations.

That is also the opinion of J.P. Morgan Harlan Sur, a 5-star analyst ranked in the top 1% of Wall Street stock experts.

Due to favorable mix-adjusted DRAM pricing, driven by a higher proportion of HBM3e shipments on the back of robust demand for NVidia’s H200 platform, Sur anticipates both revenue and EPS will exceed consensus estimates. This, combined with a recovery in traditional server demand, is expected to more than compensate for weakening DDR4/DDR5 performance caused by ongoing softness in PC, smartphone, and consumer markets.

However, as traditional DRAM pricing headwinds are expected to persist, the analyst thinks Micron’s February quarter (FQ2) guide for revenue, gross margin, and EPS will all come in below Street expectations. That said, Sur does think this impact should be partially offset by a more favorable mix shift toward HBM, including an improved 8-Hi mix and the initial ramp of 12-Hi, with Micron seemingly “gaining some share” on major Nvidia platforms.

So, basically, Sur is expecting a classic letdown scenario – a robust readout followed by a disappointing guide. However, that only tells half the story here. Because heading into the second half of next year, the backdrop is expected to turn favorable for Micron as the company “executes on cost reductions and HBM becomes a larger part of the shipment/revenue mix.”

While Sur notes that the JPM global memory team anticipates DDR4/DDR5 to weigh on DRAM ASPs over the next 2–3 quarters, he expects the downcycle will be brief, as memory suppliers increasingly shift capacity to HBM (~20–25% of total DRAM capacity by 2025), and PC and smartphone customers “resume memory procurement” in the second half of the year, driven by rising memory content needs for edge AI applications (~40–60% higher).

“On this backdrop,” Sur went on to add, “we believe blended DRAM pricing will begin to inflect higher in C2H25 as conventional DRAM potentially becomes under-supplied and HBM demand continues to remain robust through the entirety of next year and potentially into CY26.”

With MU shares having dropped about 29% since the June peak, Sur thinks “bearish sentiment is somewhat priced in,” and as the market anticipates a significant recovery in memory pricing later in 2025, the analyst thinks the stock will “start to outperform in early/1H 2025.”

Accordingly, Sur rates Micron shares an Overweight (i.e., Buy), backed by a $180 price target. The implication for investors? Potential upside of 63% from current levels. (To watch Sur’s track record, click here)

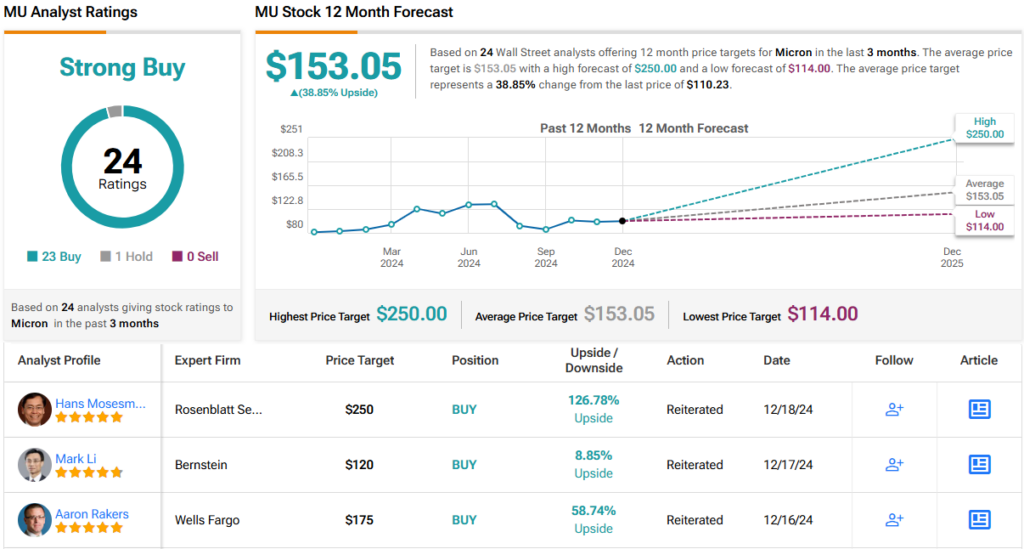

There’s barely any disagreement with that stance amongst Sur’s colleagues. Barring one skeptic, all 23 other analyst reviews are positive, making the consensus view here a Strong Buy. The average price target stands at $153.05, implying shares will gain ~39% in the months ahead. (See Micron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.