Advanced Micro Devices (NASDAQ:AMD) shares have been on a rollercoaster over the past year. At the start of 2024, the chip giant was widely seen as Nvidia’s strongest challenger in the AI chip market. But that optimism has faded. In recent months, sentiment has turned, with many now doubting AMD’s ability to secure a meaningful share of the market from Nvidia.

Now, with AMD set to report Q4 earnings after today’s close, the bears are firmly in control of the narrative with the stock showing trailing twelve-month losses of 34%.

But the situation is hardly as dire as current sentiment would suggest, says Rosenblatt’s Hans Mosesmann, an analyst ranked in the 5th spot amongst the thousands of Wall Street stock experts.

“We see the Street overly bearish into a 4Q24 and 1Q25 guide that should be in-line with seasonal PC (gaining share), solid CPU data center (gaining share), and flat to down MI300 GPU compute off of high levels,” the 5-star analyst said.

Mosesmann thinks that embedded, comms, industrial, and automotive markets are all expected to show “continued weakness into 2025,” but that has little to do with the bearish sentiment.

The key factor here is solely the MI300. For “whatever reason,” says Mosesmann, analysts have been cutting their 2025 estimates on the assumption that AMD is losing momentum. “No,” Mosesmann retorts on this take, claiming that “estimates were too high and AMD’s roadmap remains quite competitive, if not incrementally more competitive vs. Nvidia Blackwell with better ROCm compiler technology and continued chiplet advantage that helps offset the CUDA Nvidia moat.”

There’s also an “increasingly curious area of bearishness” concerning both AMD and Nvidia in accelerated computing – namely, the idea that custom ASICs are suddenly gaining market share at the expense of GPUs. While market shifts in data centers are ongoing, Mosesmann stresses these trends have been in motion for years.

“Nobody is shifting business away from AMD or Nvidia this year on the fly to a custom destined DC solution,” argues Mosesmann. Moreover, custom ASICs have almost no presence at the edge, where the real competition lies with merchant silicon for “tricked out” CPUs.

For those with a decidedly bearish slant on AMD, Mosesmann takes a contrasting view, placing faith in Lisa Su’s astute leadership.

“We like the setup of hate for AMD into the print,” he summed up. “Lisa’s team will capture double-digit DC GPU accelerated/AI compute unit share in next few years, and experience a market $ TAM of $500B, which is half of the GPU gaming share of ~30% for the last generation.”

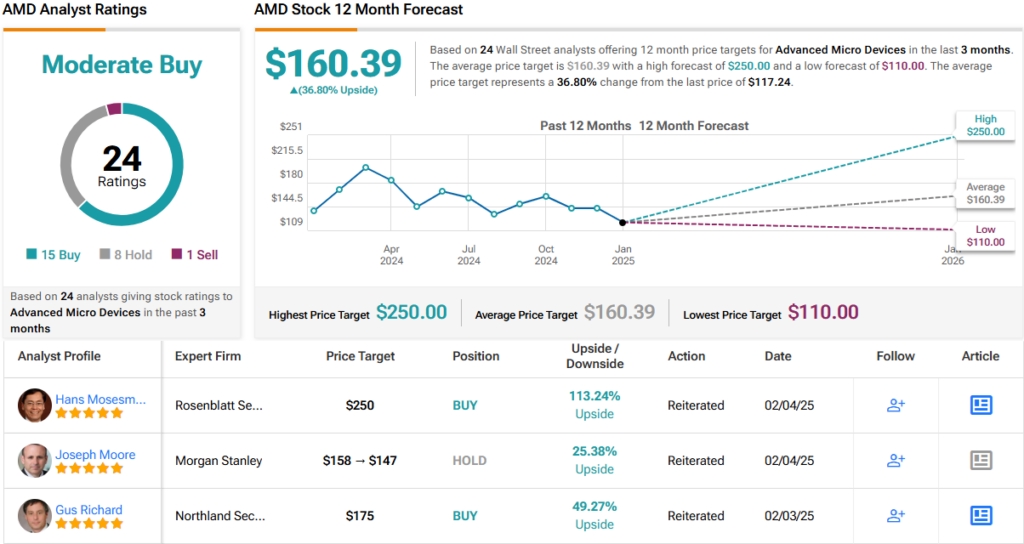

To this end, Mosesmann rates AMD shares as a Buy, while his Street-high $250 price target factors in a one-year gain of 119%. (To watch Mosesmann’s track record, click here)

14 other analysts join Mosesmann in the bull enclave and with an additional 8 Holds and 1 Sell, the consensus view is that this stock is a Moderate Buy. Going by the $160.39 average price target, a year from now, shares will be changing hands for a ~37% premium. (See AMD stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com