There is no doubt that the pandemic has impacted consumers’ shopping behavior. People are spending more on essentials, including groceries and household supplies and have cut down on their discretionary spending. Grocery sales are increasing as people are spending more time in their homes and avoiding eating at restaurants.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

Also, online shopping has increased due to stay-at-home orders and lockdowns. As per Brick Meets Click, 45.6 million US customers ordered groceries online using delivery and pickup services in June, up from 43.0 million in May.

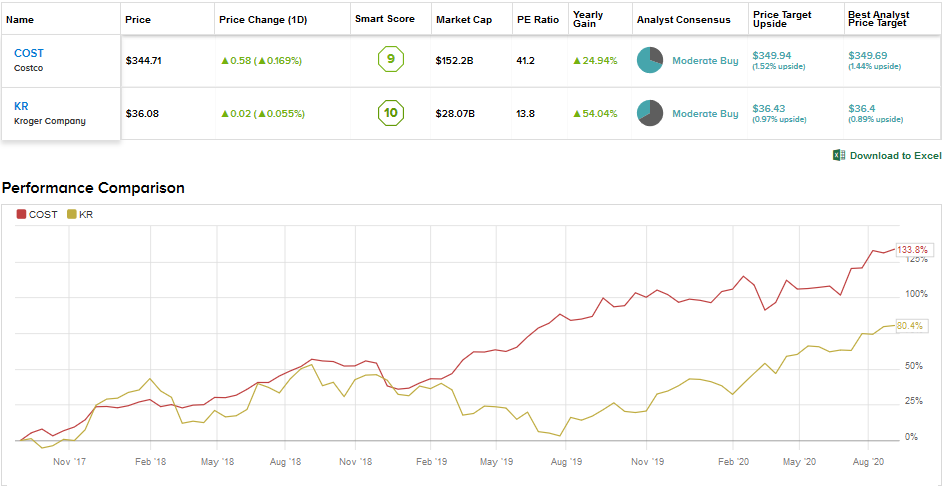

Let’s now compare two key players in the grocery space—Kroger and Costco and using the TipRanks’ Stock Comparison tool we will analyze which stock is a better investment opportunity.

Kroger (KR)

Pre-COVID, Kroger was under pressure due to growing competition in the grocery space from Amazon and Walmart as the two giants invested heavily in online grocery. Under its Restock Kroger plan, the company accelerated its digital and e-commerce initiatives.

Kroger partnered with British online retailer Ocado in 2018 to build 20 automated customer fulfillment centers over a period of three years. Moreover, the grocery chain now has more than 2,000 pickup locations and 2,400 delivery locations, reaching 97% of its customers.

Stockpiling amid lockdown and a spike in spending on groceries due to shelter-at-home orders helped Kroger deliver impressive results for its fiscal first quarter, which ended on May 23. The company’s first-quarter revenue rose 11.5% Y/Y to $41.5 billion. And its identical sales or comparable sales (excluding fuel) grew 19.0%.

Demand for cleaning and paper products and non-perishables drove the top-line growth. The company’s digital sales surged 92% and contributed more than 3% of the comparable sales. Kroger’s private brands also witnessed strong demand and delivered sales growth of 21.1%.

The company also highlighted a 32% rise in sales from its Simple Truth plant-based offerings, reflecting evolving customer choices. Aside from digital sales and private brands, Kroger sees its fresh food offerings as a key growth driver. The first-quarter adjusted EPS increased 69.4% Y/Y to $1.22 driven by higher sales and margin expansion.

Management disclosed that comparable sales grew by mid-teens in the fiscal second quarter on a month-to-date basis (as of June 18) and cautioned that sales might continue to taper in the rest of the quarter. (See KR stock analysis on TipRanks)

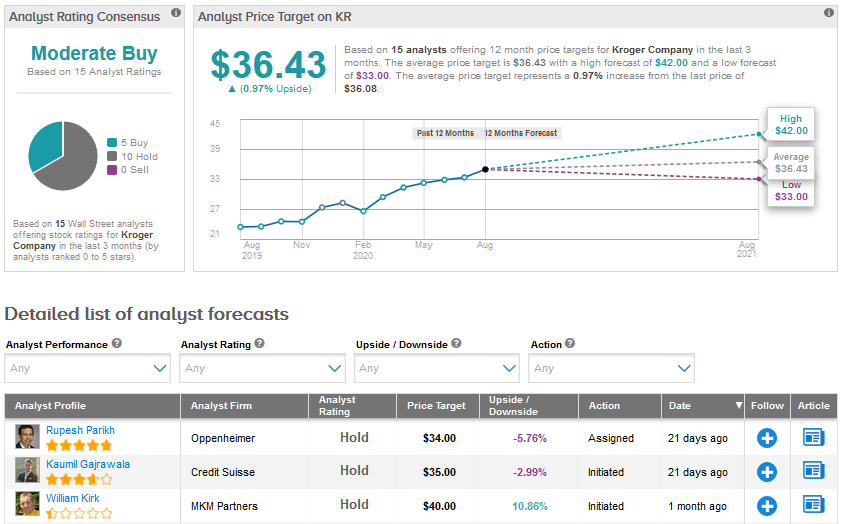

Following a meeting with Kroger’s senior management earlier this month, Oppenheimer analyst Rupesh Parikh, stated “We overall walked away still confident on the nearer-term grocery backdrop and increasingly positive on the company’s ability to navigate an evolving competitive and omni-channel grocery landscape.”

However, Parikh continues to have a Hold rating for Kroger with a price target of $34, writing “We continue to remain sidelined primarily due to valuation. KR shares very much remain on our radar.”

Overall, Kroger has a Moderate Buy consensus based on 5 Buys and 10 Holds. An average price target of $36.43 suggests a possible upside of just 1%, with Kroger stock already up 24.5% year-to-date (as of August 25).

Costco Wholesale Corporation (COST)

Earlier this month, Costco reported sales of $13.04 billion for the retail month of July (ended August 2), which reflected a robust Y/Y growth of 14.1%. The warehouse club operator’s comparable sales grew 13.2% in July backed by a 75.3% rise in e-commerce sales.

The company disclosed that the comparable sales growth in food and sundries was in low 20s and was the strongest compared to other departments. Notably, demand was high for frozen food, liquor and fresh food.

In an update provided on August 13, Oppenheimer’s Rupesh Parikh noted, “Right now, the company is really firing on all cylinders, in our view, benefiting from its leading value position in the grocery category, increased consumer appetite for at home related products, and accelerating growth in e-commerce.”

He added, “Going forward, we believe share gains could be stickier than most given the company’s superior value proposition, merchandising efforts in categories such as white goods, price investments, digital efforts, and benefits from a large number of retail bankruptcies.” Parikh has a Buy rating for Costco with a price target of $380. (See COST stock analysis on TipRanks)

Costco’s sales for the third quarter of fiscal 2020, which ended May 10, increased 7.3% Y/Y to $36.5 billion and comparable sales grew 4.8% despite lower sales in April. After gaining from stockpiling at the beginning of the quarter, Costco’s comparable sales declined 8% in April, marking the first-ever decline since July 2009. April sales reflected the impact of stay-at-home orders and social distancing, especially on the sales of discretionary goods.

Costco’s third-quarter EPS declined 7.8% to $1.89 due to incremental wages and COVID-19 related expenses. The company’s membership renewal rates were 91% in the US and Canada and 88.4% worldwide. Costco sells its goods at very low prices and its membership fee contributes a major chunk of its profits.

Meanwhile, Costco continues to strengthen its online capabilities. It acquired logistics company Innovel Solutions in March for $1 billion to boost online sales of “big and bulky” merchandise like appliances and furniture.

The Street’s Moderate Buy for Costco is based on 16 Buys, 7 Holds and no Sells. Costco had risen 17.3% year-to-date as of August 25. An average price target of $349.94 indicates a potential upside of only 1.52% over the next 12-months.

Bottom line

Both Costco and Kroger have a Moderate Buy consensus. About 70% of analysts covering Costco have a Buy recommendation, while 33% of the analysts covering Kroger assigned a Buy rating. Currently, Wall Street’s average price target indicates only a modest upside in both the stocks over the next 12-months. However, the price targets for these companies might be raised if their upcoming results beat expectations and reflect continued growth.

Costco’s valuation multiple is quite high compared to Kroger. Also, its dividend yield of 0.8% is lower than Kroger’s 2.0%. But, Costco’s performance has been comparatively consistent compared to Kroger even before the pandemic. Aside from groceries, Costco sells discretionary goods as well, sales of which might improve as the economy recovers.

Overall, Costco’s business model, customer loyalty as reflected in strong membership renewal rates, consistent performance, and a more diversified merchandise base make it more attractive compared to Kroger.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment