Knight-Swift Transportation Holdings Inc. (KNX) completed the acquisition of AAA Cooper Transportation for an enterprise value of $1.35 billion and will firmly position KNX in the less-than-truckload (LTL) space. Shares of the truckload motor shipping carrier jumped 3.9% and closed at $47.29 on July 6.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

AAA Cooper is an LTL carrier with a wide network of approximately 70 facilities (90% owned), consisting of a terminal door count of over 3,400, strategically located across the southeastern and midwestern United States, with a fleet of nearly 3,000 tractors and 7,000 trailers.

The purchase price included $1.3 billion in cash, $10 million in Knight-Swift shares, and approximately $40 million in assumed debt. The cash portion of the deal was funded through a new $1.2 billion term loan provided by Bank of America and existing Knight-Swift liquidity. (See Knight-Swift Transportation stock chart on TipRanks)

Dave Jackson, CEO of Knight-Swift said, “In seeking our first LTL partner, we had three main requirements – the scale for entry with significant market share, the profitability, and management depth to operate independently and provide a platform for compelling growth opportunities, and world-class culture. We were excited to have identified AAA Cooper as a partner that meets all three requirements.”

The acquisition is expected to be EPS accretive in the third quarter, and long term, both companies have identified multiple areas of revenue and cost synergies that are expected to lead to growth and margin expansion.

AAA Cooper is expected to earn approximately $780 million in revenue, $140 million in EBITDA, and $80 million in operating income for full-year 2021.

Following the news, Stifel Nicolaus analyst Joseph DeNardi reiterated a Buy rating on the stock and lifted the price target to $62 (31.1% upside potential) from $61.

DeNardi believes LTL provides a more stable revenue source and said, “Knight’s decision to enter the LTL market does not come as much of a surprise given the already wide net it casts across TL, Intermodal, and 3PL, and we think the deal is a win-win for both carriers. Essentially, ACT gets capital and scale and Knight gets a platform to build upon.”

The analyst expects more M&A activities in the truckload industry as driver challenges weigh and free cash generation remains robust.

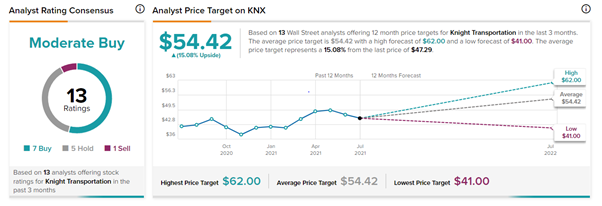

Overall, the stock has a Moderate Buy consensus rating based on 7 Buys, 5 Holds, and 1 Sell. The average Knight-Swift Transportation price target of $54.42 implies 15.1% upside potential to current levels.

Related News:

PepsiCo Earnings Preview: Here’s What To Watch for

IBM Shares Fall 5% as President Steps Down

Virgin Galactic Announces First Fully Crewed Spaceflight; Shares Soar 4%