Apple (NASDAQ:AAPL) is banking on its new iPhone lineup to kickstart another period of growth but the data available so far does not offer conclusive evidence that it is an all-out success.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

According to J.P. Morgan’s Samik Chatterjee, a 5-star analyst rated in the top 4% of the Street’s stock pros, there are early signs of a robust product cycle. However, the launch has shown slower initial momentum for the premium models compared to previous cycles.

“The difference in the lead times relative to prior years in the early weeks points to a more muted momentum in early orders for the Pro models relative to our original expectations,” Chatterjee went on to say.

The analyst attributes this to the unavailability of AI capabilities, as consumers are likely postponing their purchases until these features are accessible and the value proposition is “better understood.”

As a result, Chatterjee has adjusted his near-term iPhone unit forecast, now expecting ~126 million units in the second half of 2024, down from the previous estimate of ~130 million and ~132 million a year ago. Nonetheless, he remains optimistic about a robust AI cycle in the medium term, emphasizing that the “near-term estimates only represents a modest push out from volumes to later in the cycle.”

Basically, what Chatterjee is saying is that he expects sales are going to pick up as the cycle gets underway. As AI features become more widely available, including support for additional languages (with English expected in the second half of 2024 and other languages following in 2025), Chatterjee anticipates a growing appetite for AI-based iPhones, including the 16 Series.

In fact, the analyst expects total sales for the 16 Series in the next four quarters will surpass those of the 15 and 14 Series, remaining only slightly below the 13 and 12 Series. Meanwhile, the peak of the AI cycle should be reached once the 2025 iPhone Series hits the shelves.

“To that end,” Chatterjee summed up, “while we are lowering our near-term revenue and earnings forecast on the slower start to the AI cycle than originally anticipated, the out-year forecast remains largely unchanged as we continue to expect a robust multi-year AI-upgrade cycle, presenting solid upside opportunity for the shares.”

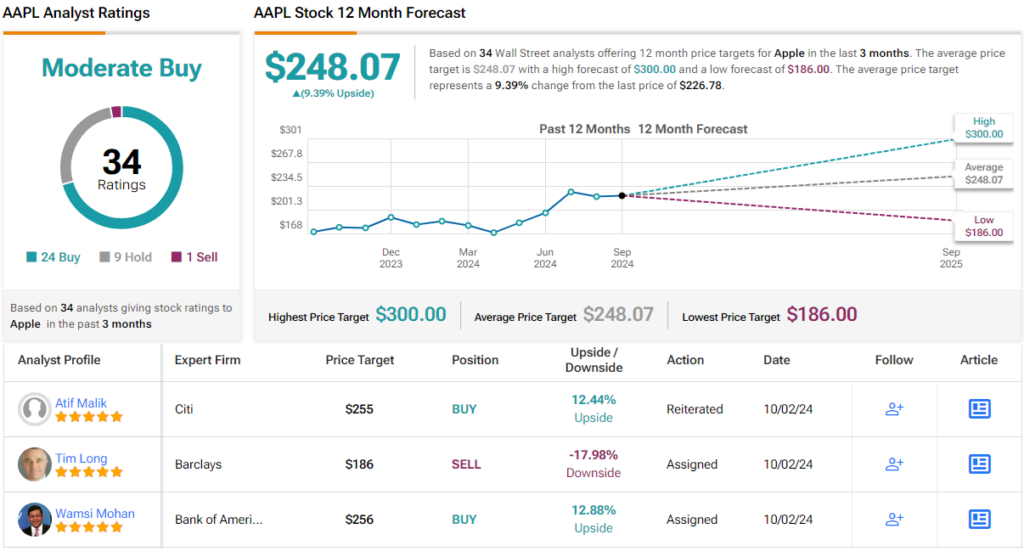

That upside, according to Chatterjee, who rates Apple shares as Overweight (i.e., Buy), currently stands at ~17%, with a price target of $265. (To watch Chatterjee’s track record, click here)

23 other analysts join JPMorgan in the bull camp and with an additional 9 Holds and 1 Sell, the consensus view is that Apple stock is a Moderate Buy. Going by the $248.07 average price target, a year from now, shares will be changing hands for a ~9% premium. (See Apple stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.