AI has been responsible for driving growth amongst plenty of names in the semiconductor space, and made its presence felt again in the latest quarterly readout from Micron (NASDAQ:MU).

In its May quarter results (FQ3), the memory giant beat expectations on both the top-and bottom-line. Revenue came in at $6.81 billion, amounting to a substantial 81.6% year-over-year increase while beating the Street’s forecast by $140 million. The company put much of the sales growth down to AI, with the demand boosting 50% of its quarter-over-quarter data center revenue growth. At the other end of the scale, EPS of $0.62 outpaced the prognosticators’ forecast by $0.09.

As for the outlook, Micron guided for FQ4 revenues of $7.60 billion (± $200 million) compared to consensus at $7.58 billion, while adj. EPS is anticipated to reach $1.08 (± $0.08) vs. the Street’s call of $1.04.

Against a backdrop of a constrained leading-edge supply environment, the company anticipates DRAM and NAND prices to rise sequentially throughout the second half of the year and into 2025, driven by AI server demand boosting growth in HBM/DDR5 and enterprise SSDs.

That said, the strong results received an initial lukewarm reaction from investors, based on higher revenue expectations for the FQ4 guide. However, scanning the print, J.P. Morgan’s Harlan Sur, a 5-star analyst rated in the top 1% of the Street’s stock pros, has only good things to say about the company’s prospects.

“We believe the team is well-positioned to capture memory content on the strong AI /accelerated compute server deployments with HBM3e capacity already sold out through CY25 and we believe the team is beginning to have visibility into CY26 demand,” explained the 5-star analyst. “AI is also fueling demand for their enterprise SSD (eSSD) products. Gross margins for HBM3e and eSSD are both accretive to their respective segments and we believe that should structurally augment their profitability profile in combination with cyclical demand/supply related pricing increases.”

As the market continues to “discount improving revenue/margin/earnings power,” Sur thinks the stock “should continue to outperform” through 2024 and into 2025. As such, the analyst has raised his price target from the prior $130 to $180, suggesting the shares could gain 36% over the next year. Sur’s rating stays an Overweight (i.e., Buy). (To watch Sur’s track record, click here)

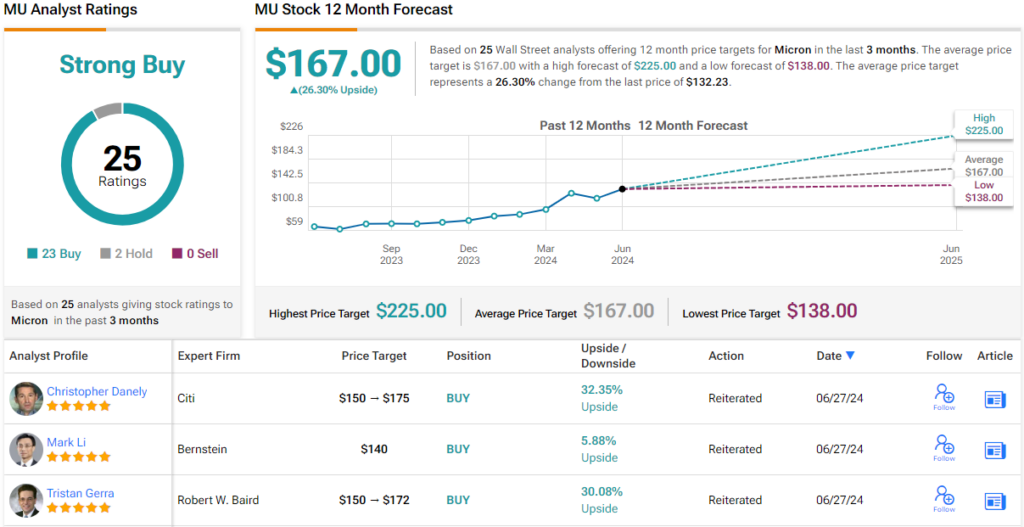

Sur is just one of many analysts boosting their price target for Micron right now. The current Street average price target stands at $167, making room for 12-month returns of 26%. Based on a lopsided mix of 23 Buys vs. 2 Holds, the stock claims a Strong Buy consensus rating. (See Micron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.