U.S. bank JPMorgan Chase (JPM) recorded profitability above its medium-term objective in this year’s third quarter and I expect the bank to outperform analyst estimates for the fourth quarter as well. The robust performance is likely to continue in 2025 against the backdrop of solid U.S. economic growth and declining interest rates. However, these positive developments are already reflected in the share price, which I estimate will provide a 7% return in 2025. As such, I rate JPM stock a Hold.

JPMorgan Chase Earnings Overview

Third-quarter financial results are one reason I rate JPM stock a Hold. JPMorgan Chase reports results in four main business segments – Consumer & Community Banking at 42% of Q3 2024 net revenue, Commercial & Investment Bank at 40%, Asset and Wealth Management at 13%, and a Corporate segment at 7% of revenues.

Consumer & Community Banking was the worst-performing segment in Q3 as its net income plunged 31% year-over-year. Results were impacted by weaker deposit margins, resulting in lower net interest income, as well as higher provisions for credit losses. The Commercial & Investment Bank segment recorded a 13% year-over-year increase in Q3 net income, driven by strength in both Banking & Payments and Markets & Securities Services.

Asset and Wealth Management delivered a 5% lower net income in Q3 as a 9% increase in revenue was offset by a 16% jump in expenses, reflecting higher compensation expenses and growth in private banking, as well as higher legal and distribution fees. The Corporate division recorded a 123% increase in net income as it benefitted from gains on its securities portfolio. On a consolidated basis, JPMorgan Chase recorded a return on tangible common equity of 19%, marginally above the bank’s 17% long-term target. Earnings per share (EPS) was $4.37, up 1% year-over-year. The tangible book value stood at $96.42 a share.

Fourth-Quarter Earnings Preview

The upcoming fourth quarter results of JPMorgan Chase are another reason to be cautious with this stock. The bank will report fourth quarter earnings on January 15. Analysts expect earnings of about $3.87 per share, reflecting the seasonally lower profitability commonly observed in the year’s final quarter. Results will also be impacted by a cumulative 0.75% in Fed interest rate cuts, further denting profitability in the Consumer & Community Banking segment. That said, the reserve build cushion outlined above should mitigate the negative effect in the near term.

I expect the Commercial & Investment Bank and Asset and Wealth Management segments to continue doing well as they are more service-oriented and benefit from robust capital markets activity. The Corporate segment will likely deliver weaker results as the recent increase in market interest rates will decrease the value of the bank’s securities portfolio.

In all, we can conclude that businesses accounting for 53% of the bank’s revenue should continue to do well in Q4 2024, while the remainder of the bank will likely deliver more muted profitability. Overall I would expect the bank to report EPS of about $4.10 a share, beating the $3.87 per share analyst consensus forecast.

Valuation and Outlook

The valuation and outlook for JPM stock are other reasons to rate shares of the bank a Hold. I estimate JPMorgan Chase will deliver $16.50 a share in earnings in an average year. For 2025 the IMF projects U.S. economic growth of about 2.2%, weaker than the 2.8% expected for 2024 but ahead of the 1.8% long-term GDP growth estimated by the Federal Reserve.

While the Fed is normalizing its monetary policy, interest rates remain above the 2.9% neutral rate expected in the long run. Stronger GDP growth and high interest rates should enable JPMorgan Chase to deliver an above average rate of return in 2025. As such, I would expect the bank to report earnings marginally below $18 a share, resulting in a 7% total return for shareholders.

This is a relatively low return potential for a bank given the inherent risks associated with investing in the industry. As such I think a Hold rating is appropriate for JPMorgan Chase. I expect JPMorgan Chase to benefit only marginally from potentially weaker capital requirements under a new Trump administration as the bank is already well-capitalized and trades at a premium valuation. Instead, I anticipate smaller lenders to provide a larger upside as they trade at lower valuations and generally do not hold as much capital as JPMorgan Chase.

Is JPMorgan Chase a Buy?

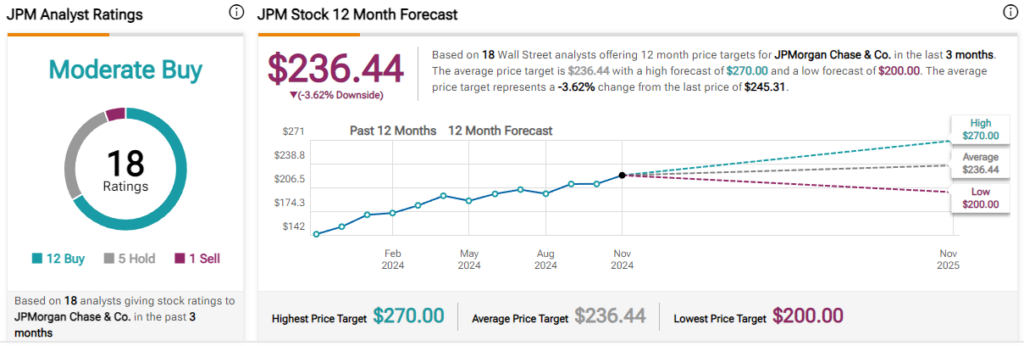

Turning to Wall Street, JPMorgan Chase earns a Moderate Buy consensus rating on TipRanks based on twelve analyst Buy ratings, five Hold ratings, and one Sell rating. Additionally, the average JPM price target of $236.44 implies 4% potential downside risk.

Read more analyst ratings on JPM stock

Conclusion

JPMorgan Chase recorded an EPS of $4.37 per share in Q3, driven by the Commercial & Investment Bank and Corporate segments. Looking to Q4, profitability should dip as is usually the case with banks and their year-end performance. That said, I expect the bank to outperform analyst estimates for $3.87 a share in quarterly earnings. The 2025 outlook is also robust as U.S. GDP is likely to grow at an above-trend pace, coupled with Fed policy remaining restrictive. This should allow the bank to outperform. However, the rosy outlook is already reflected in the stock price as I estimate the shares to offer a 7% total return for 2025, which is quite low for the banking sector. As such I rate JPM stock a Hold.