The market has been volatile since the start of 2025, as investors fret about the elevated valuations of some of the market’s leaders (particularly the mega-cap tech stocks of the ‘magnificent seven’) after these stocks fueled massive returns for the S&P 500 (SPX) and Nasdaq (NDX) over the past two years.

However, blue-chip stocks are still trading at surprisingly cheap levels, like healthcare giant Johnson & Johnson (JNJ). I’m bullish on Johnson & Johnson based on its inexpensive valuation, impressive size, and scale, which allow it to pursue attractive acquisition opportunities, dividend yield, and an unassailable dividend track record.

A Diversified Healthcare Giant

Founded 138 years ago and based in New Brunswick, New Jersey, Johnson & Johnson is one of the world’s largest and most diversified healthcare companies. It operates across two business segments, pharmaceutical and medical devices, after spinning off its consumer business, which became Kenvue (KVUE), a $40 billion company, in 2023.

According to Morningstar, the pharmaceutical segment makes up about two-thirds of the company’s business, while medical devices account for one-third. No single product or device dominates sales in either segment, so the company features a nice mix of diversification with various revenue streams. As CEO Joaquin Duato said at the JPMorgan (JPM) Healthcare Conference, “We are not a one-trick pony company; that’s not who we are.”

Flexing Its Muscles

In addition to its diversified business model, Johnson & Johnson’s immense size and scale allow it to pounce on attractive acquisition opportunities when they arise, which is exactly what it has been doing in recent years.

The company has flexed its financial muscle in acquiring cutting-edge medical device makers like Shockwave Medical for $13.1 billion in 2024 and Abiomed for $16.6 billion in 2022. At this week’s JPMorgan Healthcare Conference, Johnson & Johnson announced the acquisition of biotech Intra-Cellular Therapies (ICTI) for $14.6 billion. The New York City-based biotech focuses on products for the central nervous system, like Calypta, its treatment for schizophrenia and bipolar disorder. Intra-Cellular has been posting rising revenue and received a major boost this week when a patent settlement extended patent exclusivity for Calypta from 2036 to 2040. Promisingly, Intra-Cellular is also reportedly in line to earn approval for a potential treatment for major depressive disorder.

As Duato explained at the conference, “…our broadly diversified model in health care means that we can go where medicine is going and that we can constantly reinvent ourselves as we have done over time.”

Valuation Unbecoming of a Blue-Chip Company

As a widely recognized household name and a longtime member of the Dow Jones Industrial Average, Johnson & Johnson is a blue-chip company, but you wouldn’t guess that from its valuation.

Shares trade for just 13.4 times the consensus 2025 earnings estimates, which is incredibly cheap in today’s market. For comparison, the S&P 500 index trades for a substantially higher average multiple of 24.8 times earnings.

Against a market backdrop in which investors have grown concerned about signs of froth in the market and the rich multiples of many top growth stocks, Johnson & Johnson’s undemanding valuation is attractive. This low multiple should offer investors a strong degree of downside protection in the event of a market selloff and also leave ample room for upside.

On this note, there is also plenty of room for Johnson & Johnson to revert to the mean and join the broader market’s rally. Mega-cap tech stocks raced higher over the past year, spurring a 21.8% gain for the S&P 500 over the past 12 months, but Johnson & Johnson is down 10% over the same time frame. It, therefore, has the potential to catch up with the broader market if and when investors take profits and rotate out of some of the market’s recent winners and into some of its laggards in more defensive sectors like healthcare.

Over Six Decades of Growing Dividend Payments

Shares of Johnson & Johnson yield an attractive 3.5% on a forward basis, significantly higher than the S&P 500, which only yields 1.3%.

It’s not just the high yield that makes Johnson & Johnson an attractive dividend stock. Few companies in the market can match the incredible longevity of its dividend or its long-term track record of dividend growth. The 138-year-old company has been paying dividends to its shareholders for the past 62 years in a row, and it has increased the size of its payout in each of these 62 years.

This type of steadfast consistency is an attractive feature in a market where few things are certain, so Johnson & Johnson’s reputation as a favorite stock for income investors is well-earned.

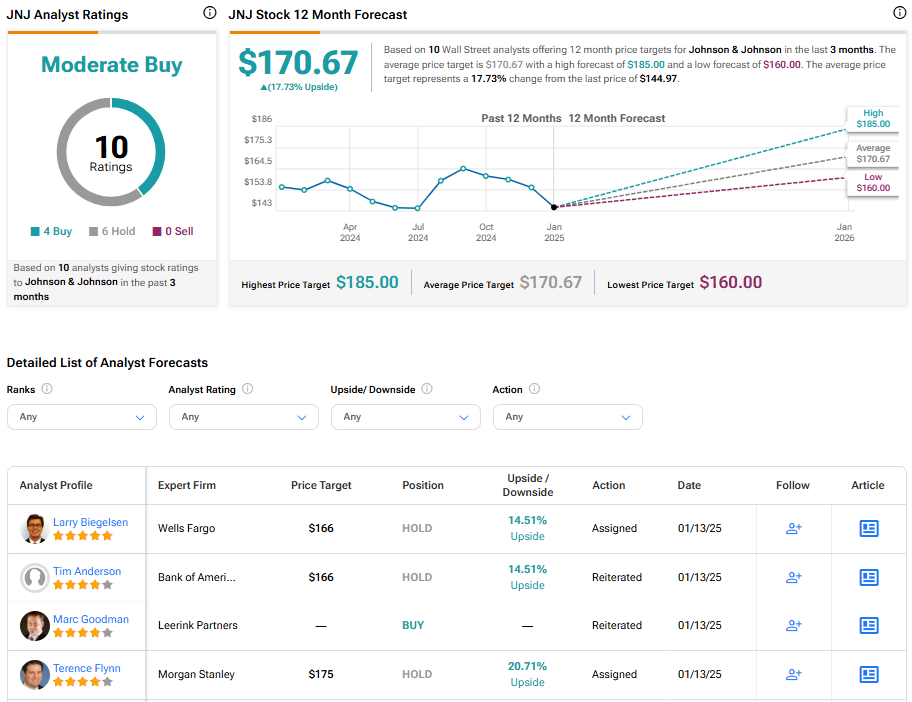

Is JNJ Stock a Buy, According to Analysts?

Turning to Wall Street, JNJ earns a Moderate Buy consensus rating based on four Buys, 11 Holds, and zero Sell ratings assigned in the past three months. The average analyst JNJ stock price target of $170.67 implies a 17.73% upside potential from current levels.

Looking Ahead

I’m bullish on Johnson & Johnson based on its undemanding valuation, which stands out in a broader market trading at an elevated level; its attractive 3.5% dividend yield; and its long history of dividend growth, which goes back over six decades. I also like how the company has used its enormous scale and financial firepower to aggressively pursue attractive acquisitions to bolster its product portfolio and position itself for long-term growth, culminating in this week’s Intra-Cellular Therapies deal.

Questions or Comments about the article? Write to editor@tipranks.com