U.S. stocks staged a comeback on Friday, with the S&P 500 surging 1.59% and reversing a sharp sell-off driven by fears that Donald Trump’s tariffs could disrupt the world’s largest economy.

Among the day’s winners, biotech stocks joined the rebound, with the SPDR S&P Biotech ETF (XBI) gaining 1.85%. The sector has struggled to gain momentum over the past year, but Jefferies analyst Michael Yee sees a window of opportunity.

“XBI is trading roughly flat YTD and it has been a mixed bag overall for the sector with some big wins (e.g., AKRO) and big M&A but has also been a tougher tape for many SMID-cap companies with a prevailing higher-for-longer narrative for rates and investor nervousness around RFK and policy uncertainty. Our analysis finds that an increasing number of biotech companies are trading below cash which reflects the mixed tape – but we believe leads to opportunities for many companies with important catalysts coming this year,” Yee opined.

And these opportunities could translate into significant gains. Few sectors offer the kind of extreme return potential found in biotech, where triple-digit gains – 300%, 400%, even 500% – are not uncommon. But, as Yee stresses, unlocking biotech’s biggest winners comes down to identifying the right catalysts – clinical trials, regulatory approvals, and strategic launches. When those pieces start falling into place, savvy investors should take notice.

Jefferies’ analysts have done the legwork and pinpointed two biotech stocks with strong upside potential – one of which could skyrocket by nearly 500% in the coming months.

And Jefferies isn’t alone in its bullish call. According to TipRanks, both stocks boast a ‘Strong Buy’ rating from the analyst consensus. Let’s dive in and uncover what’s fueling the excitement.

Alto Neuroscience (ANRO)

We’ll start with Alto Neuroscience, a clinical-stage biotech company focused on developing new drugs for the treatment of central nervous system (CNS) and psychiatric disorders. The company applies the principles of precision medicine to psychiatry, aiming to build a pipeline of drug candidates that target core brain processes and address difficult-to-treat conditions such as major depressive disorder (MDD), bipolar depression, and chronic schizophrenia.

What sets Alto apart is its deep understanding of a major challenge in psychiatry: medications don’t work the same way for everyone, and mental health conditions often evolve faster than available treatments. To tackle this, Alto has developed an AI-driven program that analyzes biomarkers from over a decade of testing data.

Alto’s key drug candidate, ALTO-300, is currently undergoing a Phase 2b clinical trial for the treatment of MDD. Designed as a novel antidepressant, ALTO-300 leverages Alto’s biomarker-based approach to provide faster, more effective relief for patients who haven’t responded well to existing therapies. Alto recently shared interim trial results for ALTO-300, which supported continuing the study with a targeted biomarker population of around 200 patients for final analysis. The company is on track to reveal topline results by mid-2026.

In addition to the MDD study on ALTO-300, several other catalysts are lined up for the coming months. The company is set to release Phase 2a proof-of-concept data on ALTO-203 in the first half of 2025. This drug candidate addresses anhedonia, a symptom of MDD and schizophrenia that reduces the ability to experience pleasure and remains difficult to treat with existing therapies. ALTO-203 specifically targets neural pathways involved in reward processing, and positive results could position it as a key advancement in addressing treatment-resistant symptoms.

Meanwhile, data from a Phase 2 proof-of-concept trial for ALTO-101, a potential treatment for cognitive impairment associated with schizophrenia (CIAS), is expected in the second half of 2025. Unlike standard schizophrenia medications that focus on hallucinations and delusions but offer little help for memory deficits, attention difficulties, and impaired decision-making, ALTO-101 aims to address these overlooked cognitive symptoms.

Last but not least, ALTO-100’s Phase 2b trial is underway, with topline data expected in 2026. Though an earlier MDD study fell short of statistical significance, the drug remains a compelling candidate for bipolar depression. By targeting stress-related brain circuits, ALTO-100 introduces a novel approach that could unlock meaningful benefits for a more targeted patient population.

With a pipeline full of upcoming catalysts and innovative approach to psychiatric drug development, Jefferies analyst Andrew Tsai views Alto’s $2.80 share price as a compelling entry point.

“In 2025, we think the stock has the potential to recover on 3+ Phase II datasets, where (+) data could instill investor confidence that mgmt’s biomarker approach of tailoring treatments to maximize efficacy can be viable in psychiatry… the risk/reward looks favorably skewed,” Tsai opined.

Regarding ALTO-300, in particular, Tsai notes several reasons for optimism: “(1) ALTO-300 is already approved in the EU/Australia for MDD broadly. However, it was not approved in the US as the former sponsor (NVS) was unable to have the same dose succeed in two Phase III studies, which speaks to level of inconsistency that comes with all-comer studies, (2) ALTO-300’s prior open-label 8-week Phase IIa data showed a -17 point MADRS benefit in bio+ vs -12.3 points in bio-, (3) We think ‘300’s safety is manageable at the lower dose of 25mg, (4) Note mgmt prospectively removed N=52 patients from this ‘300 study following site/subject case reviews, which raises the chances the Phase IIb is enrolling actual MDD patients.”

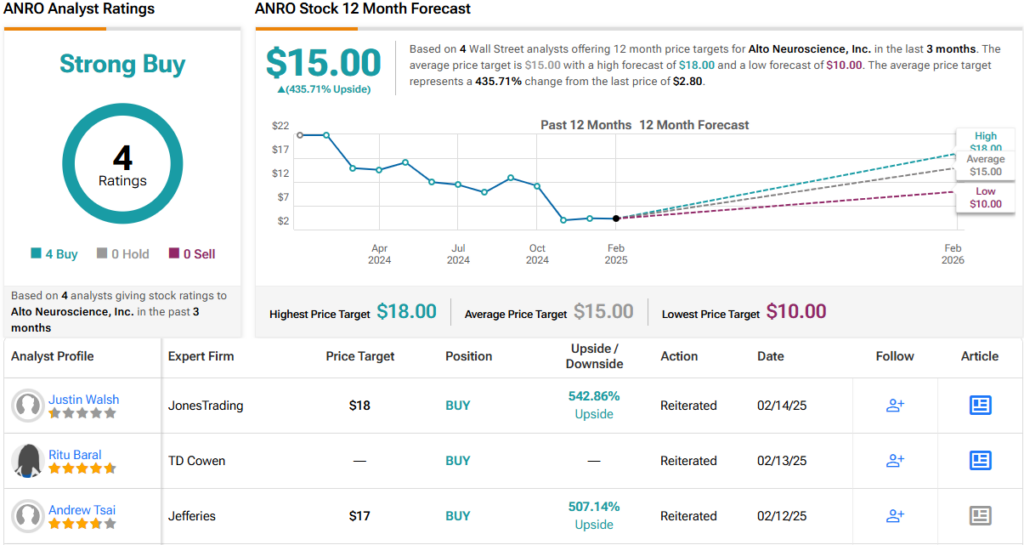

With these factors in play, Tsai rates ANRO a Buy with a $17 price target, implying a robust 507% upside from current levels. (To watch Tsai’s track record, click here)

Wall Street echoes his bullish stance. ANRO holds a Strong Buy consensus rating based on 4 unanimous positive reviews in the past 3 months. With an average price target of $15, the stock could surge 435% higher in the next year. (See ANRO stock forecast)

Instil Bio (TIL)

Next up is Instil Bio, a clinical-stage biopharmaceutical company that has undergone a transformation. Initially, the company was centered on developing tumor-infiltrating lymphocyte (TIL) therapies. However, as part of a strategic pivot, Instil has shifted its focus toward in-licensing bispecific antibodies.

This transformation gained momentum in August 2024, when Instil entered into a partnership with Chinese company ImmuneOnco Biopharmaceuticals to develop two drug candidates: SYN2510, a PD-L1xVEGF bispecific antibody, and IMM27M, a next-generation anti-CTLA-4 antibody. Through this collaboration, Instil secured global development and commercialization rights for these assets outside of Greater China.

In mid-January 2025, ImmuneOnco initiated the first dose in a Phase 1b/2 clinical trial of SYN2510, in combination with chemotherapy, for patients with advanced non-small cell lung cancer (NSCLC) in China. Initial clinical data is expected in the second half of 2025. Meanwhile, Instil plans to begin enrollment in a U.S. trial evaluating SYN-2510 in combination with chemotherapy as a treatment for first-line (1L) NSCLC in 2H25, pending regulatory approval.

In addition to NSCLC, Instil Bio is exploring the potential of SYN2510 for treating triple-negative breast cancer (TNBC). A Phase 1b/2 trial in China is planned to evaluate SYN2510 in combination with chemotherapy for first-line TNBC patients, with the study expected to begin in 1H25.

Among the supporters is Jefferies analyst Kelly Shi, who sees considerable potential in the stock.

“TIL’s initial focus is on NSCLC (Ph2 to start in 2H25) and TNBC with China partner running trials in multiple other indications with dose escalation data update in 1H25. SYN2510 presents a unique molecular design: 1) VEGF arm uses ‘Trap’ (VEGFR fusion protein) vs bev (mAb) used in ivo and BNT327; 2) an intact Fc domain vs silenced in ivo and BNT327; 3) PD-L1 (same w/ BNT327) vs PD-1 in ivo. The early (subtherapeutic doses) dose-esc data showed similar ORR vs BNT327. So far, we don’t see enough evidence for differentiation. However, even the base case scenario (similar clinical profile to SMMT’s or BNTX’s) should reflect a largely undervalued opportunity. As the third asset with global trials in plan, we see significant upside for TIL shares,” Shi stated.

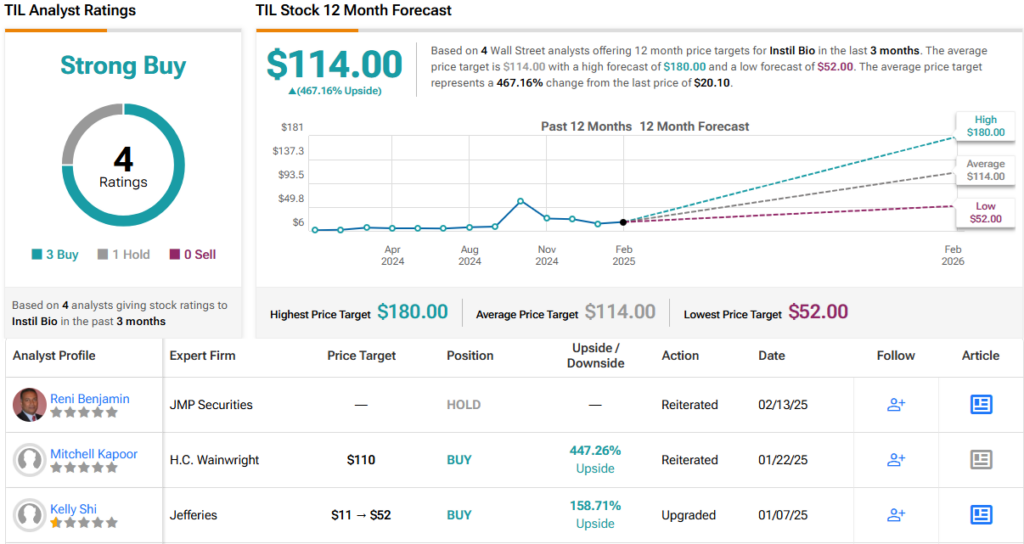

These comments support Shi’s Buy rating on TIL, and her $52 price target suggests a potential one-year upside of 158%. (To watch Shi’s track record, click here)

For the most part, other analysts are on the same page. With 3 Buys and 1 Hold, the word on the Street is that TIL is a Strong Buy. The stock’s $20.10 trading price and $114 average price target together imply an upside of 467% for the coming year. (See TIL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.