JD.com (NYSE:JD), China’s e-commerce giant, kicked off 2024 on a high note. The company’s Q1 results showed robust revenue growth and improved profitability. In fact, JD has finally approached the required scale to significantly expand its margins, which has led to its free cash flow surging. Despite this progress, Wall Street continues to overlook JD’s investment case, resulting in the stock trading at just under 6x free cash flow. For this reason, I believe that JD is severely undervalued at its current levels, and I am bullish on JD stock.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

Q1 2024: A Masterclass in Achieving Economies of Scale

JD’s Q1 report was, above all, a masterclass in achieving economies of scale, resulting in a notable surge in the company’s free cash flow. You see, the company runs a relatively low-margin business model. This is primarily because JD, unlike many of its competitors, operates its own extensive logistics network. The company invests heavily in warehousing, delivery infrastructure, and technology to ensure efficient and timely delivery services.

Additionally, JD offers a wide range of products at competitive prices to attract and retain customers, which further compresses its profit margins. However, with the right scale, the business has tremendous potential to achieve significant economies of scale over time. This is exactly what we saw play out in Q1, with the company’s continuous growth leading to a strong enough margin expansion to drive fantastic profitability.

Specifically, JD reported net revenues of $36.0 billion, marking a 7% increase year-over-year. This result can be attributed to several drivers that bolstered the company’s performance across its various business segments. The most notable one was the increased user engagement and active user base, which directly resulted from increased focus on user experience.

In the earnings call, JD’s CEO, Sandy Xu, stressed that the emphasis on delivering a superior combination of selection, speed, quality, and price attracted more Chinese consumers nationwide.

Other initiatives, including introducing an AI digital representative for live streaming, which gathered over 20 million views in the first hour of launch, also played a strong role in improving JD’s content ecosystem and consumer engagement.

With revenue growth outpacing growth in operating expenses, the company’s operating margin came in at 3.0%, up from 2.6% in the previous year. As you can see, JD’s margins remain razor-thin. However, tiny improvements in margins can be leveraged to drive exceptional growth in earnings. Evidently, the growth in revenues, along with the modest margin expansion, led to JD’s operating income growing by a much more significant 19.8% to $1.1 billion.

The very same logic applies to free cash flow. With operating cash flow climbing to $9.67 billion over the past 12 months and capital expenditures remaining relatively flat, free cash flow came in at $7.01 billion, up 166% compared to the prior-year period.

JD’s Valuation Is Too Cheap To Keep Ignoring

Given JD’s significant surge in free cash flow in recent quarters, paired with a relatively static share price, I believe the stock has become too cheap to ignore. JD stock is now trading at levels reminiscent of its IPO price a decade ago. This is even as its revenues and free cash flow have increased multiple times over during this period.

In fact, the stock is now trading at just 5.9 times its last-12-month free cash flow despite sustaining robust growth. I don’t see how the company can keep growing its free cash flow without eventually breaking out. In the meantime, the company’s capital returns potential remains on the rise. Between January 1st, 2024, and May 15th, 2024, when JD posted its Q1 results, management bought back $1.3 billion worth of stock, 3.1% of outstanding shares.

There is no doubt that the stock warrants a discount, considering the inherent risks linked to investing in a Chinese company. However, when you see an industry leader trading at such a cheap valuation while actively returning capital to shareholders, it forces you to pause and reflect. Is a stagnant stock price even sustainable at this pace? I don’t think so.

Is JD.com Stock a Buy, According to Analysts?

Regarding Wall Street’s view on the stock, JD has a Strong Buy consensus rating based on 15 Buys and four Holds assigned in the past three months. At $38.99, the average JD stock price target implies 45.6% upside potential.

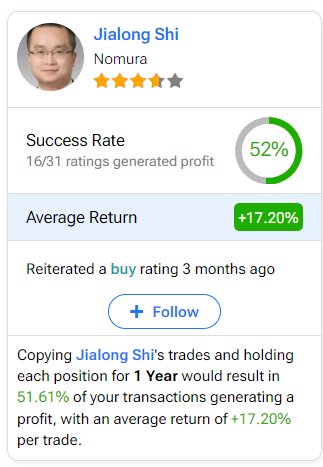

If you’re uncertain which analyst you should follow if you want to buy and sell JD stock, the most accurate analyst covering the stock (on a one-year timeframe) is Jialong Shi from Nomura, with an average return of 17.20% per rating and a 52% success rate. Click on the image below to learn more.

The Takeaway

JD’s Q1-2024 results underscored the company’s ability to leverage its rising revenues to drive higher margins and free cash flow. More importantly, these results essentially exposed that the stock’s valuation may have finally become too cheap. After years of consistent growth against a falling share price, we may have reached the point where investors may not be able to afford to miss the stock’s investment case. This is particularly true, given that JD has been repurchasing and retiring shares rapidly lately.