Jabil, Inc. (JBL) reported mixed results for the fiscal fourth quarter of 2021, topping earnings estimates, but falling slightly short of revenue expectations due to ongoing supply constraints.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Shares of Jabil dropped 6.1% to close at $57.23 on September 29 following the news but gained 2.3% in the extended trading session on optimistic Fiscal 2022 guidance.

Markedly, shares of the global manufacturing solutions provider with operations across 100 plants in 30 countries have risen 67% over the past year. (See Jabil stock charts on TipRanks)

Encouragingly, Q4 adjusted earnings of $1.44 per share grew 47% year-over-year and beat analysts’ expectations of $1.38 per share. Comparatively, the company reported earnings of $0.98 per share in the prior-year period.

However, net revenues grew 1.5% year-over-year to $7.4 billion and were short of consensus estimates of $7.67 billion. Segment-wise, Diversified Manufacturing Services revenues grew 10%, whereas Electronics Manufacturing Services declined 6% year-over-year.

Jabil Issues Guidance for Q1 and Fiscal 2022

Based on the Q4 results, management provided financial guidance for the first quarter and full-year of Fiscal 2022.

For Q1, the company forecasts adjusted earnings in the range of $1.70 to $1.90 per share, while the consensus estimate is pegged at $1.75 per share. Furthermore, revenues are forecast to grow 5% year-over-year to between $8 and $8.6 billion, versus the consensus estimate of $8.25 billion.

For Fiscal 2022, the company forecasts core EPS of $6.35 and net revenues to grow 7.5% to $31.5 billion.

CFO Mike Dastoor commented, “As we move ahead, the momentum within our business is expected to continue into FY22.”

Dastoor further added, “In a world where increasingly complex hardware needs to be built, Jabil is incredibly well-positioned to benefit from secular growth we’re experiencing across vehicle electrification, connected healthcare and infrastructure development, to name a few.”

Following the Q4 results, Stifel Nicolaus analyst Matthew Sheerin upgraded Jabil from Hold to Buy and increased the price target from $63 to $68 (18.8% upside potential).

Sheerin said, “We see the pullback in shares post earnings (6% vs. flat for the S&P) as a buying opportunity, particularly given Jabil’s robust outlook for FY22.”

Sharing his views on the upside, the analyst added, “Driving that growth are programs in higher-margin end markets where Jabil has made significant investments, including auto/transportation (expected to grow 41% in FY22), healthcare, industrial and cloud.”

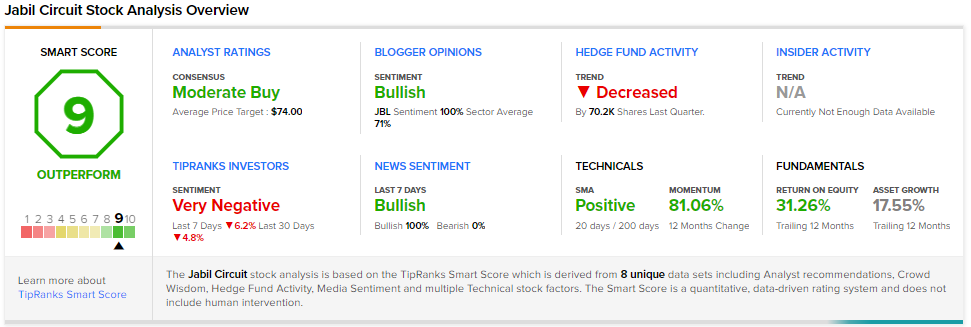

Consensus among analysts is a Moderate Buy based on 2 unanimous Buys. The average Jabil price target of $74 implies 29.3% upside potential to current levels.

JBL scores a 9 out of 10 on TipRanks’ Smart Score rating system, indicating that the stock has strong potential to outperform market expectations.

Related News:

Thor Industries’ Shares Leap 8% on Stellar Q4 Beat

United Airlines Partners with Airlink to Expand Travel Connectivity in Southern Africa

Ovintiv Launches 26M Share Buy-Back Program; Shares Rise