SoFi Technologies (NASDAQ:SOFI) was a standout performer in 2024, and its momentum has carried into 2025, with the stock surging ~15% year-to-date. In fact, this rally has propelled the stock to levels not seen in three years, defying a broader downturn in the fintech sector even amid rising Treasury yields and reduced expectations for rate cuts in 2025.

With the neobank set to report Q4 earnings before the market opens tomorrow (January 27), investors will be hoping the company can deliver a strong print and build on the current momentum.

Looking ahead to the readout, J.P. Morgan analyst Reginald Smith takes an upbeat stance on what is about to unfold.

“Ultimately,” Smith notes, “we are positive into the print, despite rising treasury yields, which could be a ~$100M headwind to loan FVs (net of hedges and cushion from 3Q24), as we think SoFi’s Loan Platform business, which contributed >$50M in high-margin revs in 3Q24, could be a source of upside this quarter and a meaningful (and underappreciated) profit driver in ‘25.”

The capital-light Loan Platform Business’ momentum was the big surprise last quarter. Here, SoFi originates loans and right away transfers them to third parties, earning referral or origination fees. The company had previously not brought much attention to this channel, but in 3Q24, SoFi originated approximately $1 billion in personal loans, generating $56 million in high-margin fees – a year-over-year increase of more than 5x.

“We like this business,” Smith adds, “as it allows SoFi to monetize applicants that may have otherwise been rejected (SoFi rejects >70% of PL applicants), without burdening its own balance sheet or capital ratios, which could ultimately boost ROE and drive multiple expansion.”

Looking ahead, Smith expects SoFi’s 2025 guide will likely factor in low 20% revenue growth and around 30% EBITDA margins, inline with Street expectations. Smith also points out that the company has a track record of beating and raising targets as the year progresses.

As for what to do with the stock, Smith’s advice is to load up on any post-print weakness, but he refrains from getting on board right now. While positive on 2025, given the recent strength, shares “could take a breather on the print.”

“Looking to 2025,” the analyst summed up, “we expect the conversation to shift to Financial Service monetization, the Loan Platform business, Tech Platform deals and balance sheet growth, while acknowledging inflation and rising rates could reignite debates around fair value marks and credit losses.”

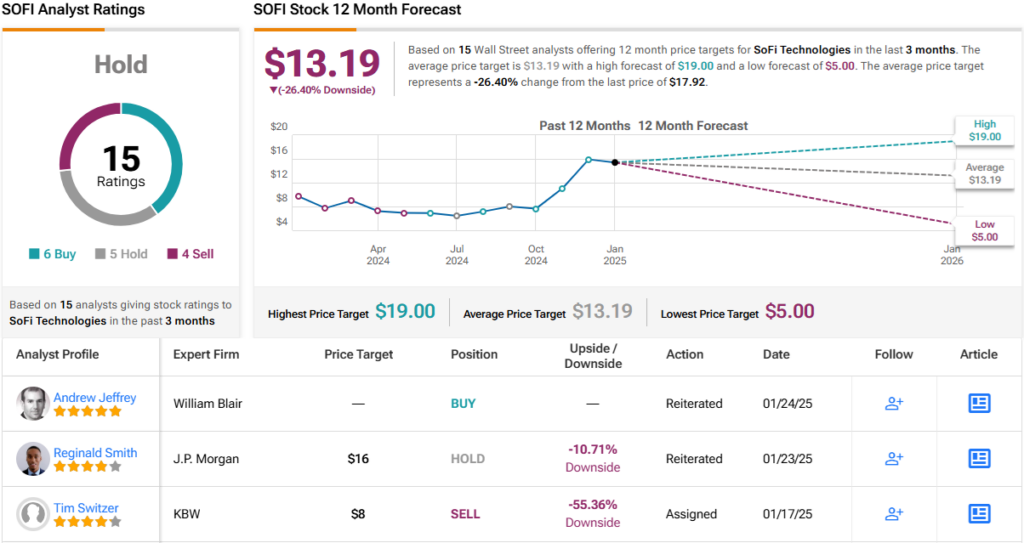

All told, Smith assigns a Neutral rating for SoFi shares, along with a $16 price target, suggesting an ~11% downside from the current share price. (To watch Smith’s track record, click here)

Smith isn’t alone in playing it safe. 4 other analysts are also sitting on the fence, while 6 are betting on Buys and four are waving the Sell flag. The consensus? A Hold (i.e., Neutral) rating. The broader view suggests SoFi may be flying too high, with the $13.19 average price target pointing to a potential 26% drop over the next year. (See SOFI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.