J.P. Morgan is on the cusp of paying $1 billion to settle an US investigation into the alleged market manipulation of metals futures and Treasury securities trading, according to a Bloomberg report.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

The potential record penalty for a settlement involving alleged spoofing could be announced as soon as this week, according to the report. The settlement would put an end to probes by the US Justice Department, the Commodity Futures Trading Commission and the Securities and Exchange Commission into whether traders on JPMorgan’s (JPM) precious metals and treasuries desks rigged markets.

Last year, US prosecutors filed criminal charges against individual J.P. Morgan traders, saying the bank’s precious metals desk operated as an illicit enterprise within the bank for almost a decade. The government’s settlement with the US bank is not expected to result in any restrictions on its business practices, according to the report.

Spoofing typically involves flooding derivatives markets with orders that traders don’t intend to execute to trick others into moving prices in a desired direction. The practice has become a focus for prosecutors and regulators in recent years after lawmakers specifically prohibited it in 2010, according to the report. While submitting and then canceling orders isn’t illegal, it is unlawful as part of a strategy intended to dupe other traders.

According to the Bloomberg report, the Justice Department used racketeering laws more commonly used in mafia and drug gang prosecutions, alleging the bank’s precious metals desk effectively became a criminal enterprise for eight years.

J.P. Morgan shares have been hit hard plunging 33% so far this year as the coronavirus pandemic hurts its businesses. (See JPM stock analysis on TipRanks)

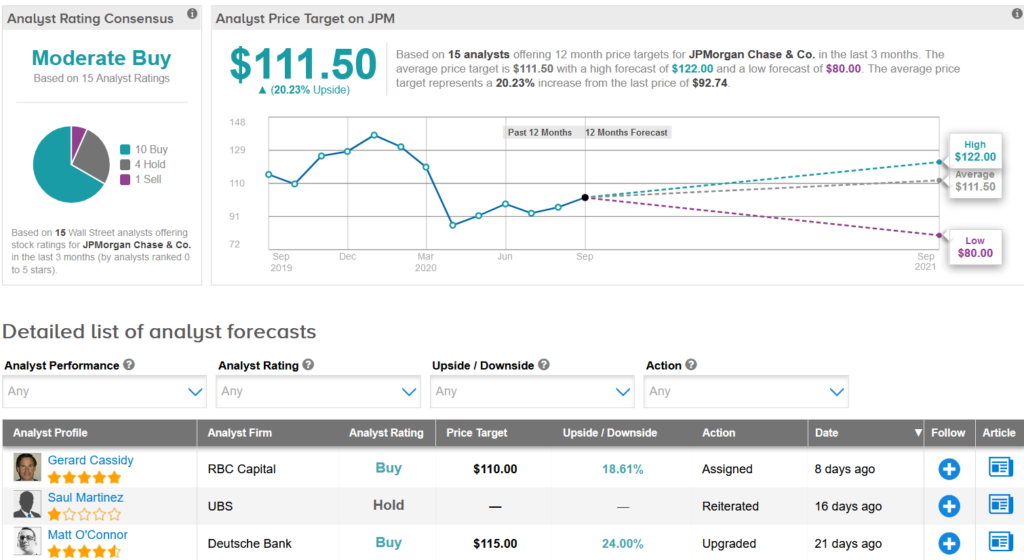

Meanwhile, RBC Capital analyst Gerard Cassidy last week raised the stock’s price target to $110 from $99 and reiterated a Buy rating, following recent company comments on Q3 trends.

“We have revised our full-year 2020 and 2021 EPS estimates to $6.41 and $8.62 from $5.21 and $9.25, respectively, to reflect recent commentary on weaker net interest income being more than offset by stronger capital markets revenues and a lower loan loss provision for 2020,” Cassidy wrote in a note to investors. “We lowered our 2021 EPS estimates to primarily reflect lower net interest income in 2021 than earlier expected.”

The rest of Wall Street is cautiously optimistic on the stock. The Moderate Buy analyst consensus shows 10 Buys versus 4 Holds and 1 Sell. The $111.50 average analyst price target implies 20% upside potential over the coming year.

Related News:

Gilead To Pay $97M To Settle Kickback Debacle Over Letairis Drug

Lululemon Resumes Share Buyback; Shares Rise 3%

KKR Snaps Up $755M Stake In Reliance’s Retail Unit; Street Is Bullish