J.M. Smucker Co. has entered into an agreement with B&G Foods Holdings (BGS) to divest its Crisco oils and shortening business for about $550 million.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

As per J.M. Smucker (SJM), the divestiture of the Crisco line is in alignment with its decision to exit the US baking space and focus on the company’s core growth platforms of pet food, coffee and snacking.

The Crisco business contributed net sales of about $270 million in the fiscal year ended Apr. 30, 2020. The deal includes oils and shortening products sold under the Crisco brand, certain trademarks and licensing agreements, as well as dedicated manufacturing and warehouse facilities located in Cincinnati, Ohio. It also includes the company’s oils and shortening business outside of the US, primarily in Canada.

Meanwhile, J.M. Smucker expects the Crisco divestiture to have an adverse impact of $0.45 to $0.55 on its full-year adjusted EPS, before taking into account any potential benefit from the sale proceeds. The company is set to complete the transaction in the third quarter of fiscal 2021, subject to regulatory approvals.

In a separate press release, B&G Foods’ CEO Kenneth G. Romanzi said, “Crisco is an excellent complement to our existing portfolio of brands, including our Clabber Girl and other baking powder brands. This acquisition is consistent with our longstanding acquisition strategy of targeting well-established brands with defensible market positions and strong cash flow at reasonable purchase price multiples.”

B&G Foods expects the acquired business to generate adjusted EPS of between $0.45 to $0.50 in 2021.

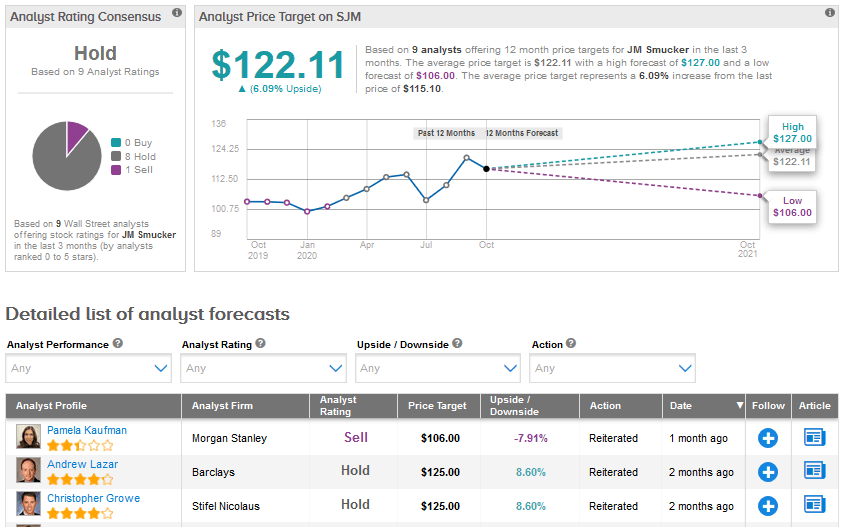

Last month, Morgan Stanley analyst Pamela Kaufman lowered the price target for J.M. Smucker to $106 from $114 and reiterated a Hold rating. In addition to viewing the company as a lesser beneficiary of elevated packaged food demand, she cites its exposure to the Pet category, “inconsistent” innovation and marketing and share losses across key categories as causes for concern.

Pointing to Nielsen data, the analyst stated that the company lost market share in the pet treats, peanut butter and dog food categories in the last four weeks. (See SJM stock analysis on TipRanks)

The Street is cautious about J.M. Smucker. Its Hold analyst consensus is based on 8 Holds and 1 Sell, with no Buy ratings assigned. The $122.11 average analyst price target suggests an upside potential of 6.1% in the months ahead. Shares have risen 10.5% year-to-date.

Related News:

Bloomin’ Brands Tops 3Q Results As Restaurant Sales Improve

Dunkin’ Brands In Takeover Talks With Inspire Brands

Coca-Cola European Partners In Talks To Buy Australian Bottler – Report