My strategy as a dividend investor is to buy the most dominant businesses on the planet at reasonable valuation. This is because well-known companies tend to enjoy competitive advantages. That allows them to consistently grow earnings and pay higher dividends to shareholders.

The world’s largest publicly traded payments processor Visa (V) is one such stock in my portfolio. Along with the release of its Fiscal fourth-quarter earnings, the company hiked its quarterly dividend by 13.5% to $0.59 a share. After Visa’s latest quarterly results, I believe the stock could be an intriguing dividend growth play for long-term investors. As such, I am bullish on V stock.

Visa’s Strong Growth

A big reason why I’m bullish on Visa is the company’s strong growth. On October 29, Visa announced its Fiscal fourth-quarter earnings. The company’s revenue rose 11.7% year-over-year to $9.6 billion. This respectable topline growth was powered by a 7% growth rate from a year ago in Visa’s cardholder base to 4.6 billion. Payments volume, total cross-border volume, and processed transactions rose by 8%, 13%, and 10% for the quarter. That was due to the continued adoption of Visa’s payment network in emerging markets and steady consumer spending.

The company’s earnings per share (EPS) climbed by 16.3% to $2.71 during the quarter. Visa’s business model allows it to scale volume and processed transactions without growing its operating expenses as fast as net revenue. That led the company’s net profit margin to expand by 50-basis points to 56.4%. Combined with share repurchases, this is how adjusted EPS growth surpassed net revenue growth for the quarter.

While I acknowledge the U.S. Justice Department’s antitrust lawsuit against Visa, accusing the credit card company of holding an illegal monopoly over debit payments, I don’t expect this to have a long-term impact on the company or its stock. Visa has called the Justice Department’s lawsuit “meritless” and vowed to fight it in court. Ultimately, this action by the U.S. government shouldn’t materially impact Visa’s business or its growth prospects.

Future Opportunities for Visa

The best days for Visa are yet to come, which is why I’m bullish on the stock. The company has major catalysts working in its favor. Visa’s business model is one inherent advantage. Not only does the company receive a fixed amount for each processed transaction but it also gets paid a percentage of total dollar volumes handled. In the latter case, inflation is an organic means of how dollar volumes rise.

Another reason for optimism is that in the company’s new flows business, the estimated annual payment volume is $200 trillion. By itself, that’s almost 13x Visa’s Fiscal year 2024 payment volume. The carded business-to-business opportunity comprises about 10% of that at $20 trillion. That means Visa’s sub-$2 trillion in commercial payments volumes are less than 10% of this opportunity, which means the company is in the early innings of growth. Recent moves in the cross-border business-to-business space have led to a 40% surge in the number of banks signed onto Visa’s B2B Connect service.

These elements explain why the analyst consensus continues to expect firmly double-digit annual EPS in the years ahead. In Fiscal year 2025, a 12.6% rise in adjusted EPS to $11.17 is anticipated. For Fiscal year 2026, another 12.4% increase in adjusted EPS to $12.56 is being projected.

Continued Dividend Growth

The potential for future dividend growth is another reason to be bullish on V stock. At a glance, Visa’s 0.8% dividend yield isn’t that impressive versus the 1.3% yield in the S&P 500 index (SPX). Diving deeper into the dividend, though, the story is clearly about dividend growth. In the past five years, Visa’s dividend has cumulatively risen by 96.7%. That’s equivalent to a 14.5% compound annual growth rate (CAGR).

Visa’s most recent dividend raise implies that the rate of these payout hikes remain constant in the low teens. Visa’s payout ratio is going to be in the low 20% range in Fiscal 2025, which is quite sustainable. That’s why I believe the company has a realistic path to keep handing out dividend boosts that are at least as fast as its EPS growth.

Balance Sheet and Valuation

Visa also maintains an enviable financial position and attractive valuation. As of September 30, the company’s net debt balance was $5.7 billion (cash and cash equivalents, plus investment securities minus long-term debt). Against the $24.6 billion in Fiscal 2024, this is a net debt-to-EBITDA ratio of just 0.2x. That explains why Visa possesses a high grade, AA- corporate credit rating from S&P Global (SPGI) on a stable outlook.

Visa looks to be priced at a discount relative to its fundamental outlook. The company’s price-to-earnings (P/E) ratio of 26.2 is moderately below its 10-year normal P/E ratio of 29.2. This is despite steadily expanding profit margins and EPS growth potential in the high teens annually.

Is V Stock a Buy?

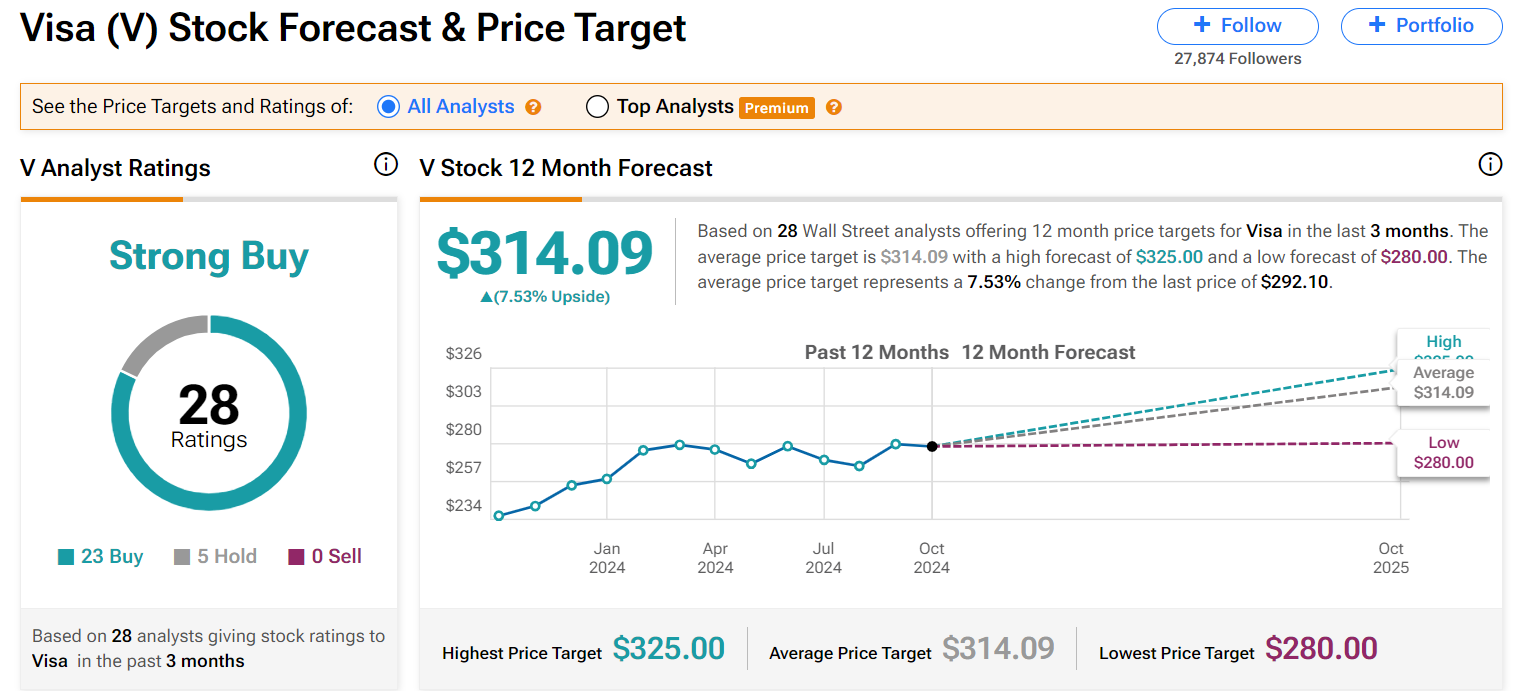

Shifting our focus to Wall Street, analysts have a Strong Buy consensus rating on Visa. This is based on 23 Buy ratings and five Hold ratings assigned in the past three months. At $292.10, the average 12-month price target of $314.09 suggests 7.53% upside.

Conclusion

Visa is a sound business. The company has ample catalysts to keep posting strong growth. While the U.S. Justice Department’s antitrust action is an issue, it doesn’t take away from Visa’s fortress balance sheet or the lengthy runway for the company’s dividend growth. The moderate undervaluation is what seals the deal for me to give this stock a bullish rating.