United Parcel Service (UPS) is scheduled to release its Q2 results on Tuesday, July 23. Wall Street expects flat revenues and a significant drop in earnings per share due to lower volumes, increased costs, and an unfavorable product mix hurting margins. Despite these challenges, the package delivery giant’s results are ultimately set to normalize and return to growth in the near future. In the meantime, following the stock’s underperformance over the past year, UPS stock appears attractively priced today. Thus, I am bullish on UPS stock.

UPS Coming Off a Weak Q1 Performance

As UPS prepares to release its Q2 results, it’s important to note that the company faced challenges in Q1, a trend expected to persist in its upcoming report. UPS posted total revenues of $21.7 billion last quarter, a 5.3% decrease year-over-year, with notable weakness registered both domestically and internationally.

The company’s U.S. Domestic segment, which accounts for the most significant portion of its operations, posted a 5.0% revenue drop from nearly $15 billion last year to $14.2 billion in the previous quarter. The drop was primarily due to a 3.2% decrease in average daily volume, reflecting a slowdown in domestic shipping activities.

Internationally, the company recorded $4.3 billion in revenue, also a decline from $4.6 billion in the same quarter of the previous year. Economic slowdowns in key regions, including Europe and Asia, affected the international market, which led to lower export volumes. Finally, Supply Chain revenues fell by 5.3% to $3.2 billion due to market rate declines in forwarding.

In the meantime, UPS faced considerable pressure on its margins and profitability. One major factor was the higher labor costs associated with the first year of the new Teamster’s contract. This agreement led to a 13% rise in union wage rates, significantly impacting operating expenses.

Management argued that they mitigated these costs through productivity headways and cost management initiatives. In particular, the company downsized total operational hours by 6.6% and closed 18 sorts, reflecting their efforts to match volume levels with resources. However, UPS’ adjusted operating margin still fell by 400 basis points to 5.9%. Along with the decline in revenues, the company’s adjusted EPS plunged by 35% to $1.43.

Weak Results to Persist in Q2, But Start Improving Thereafter

The rather subdued market conditions that UPS experienced in Q1 are likely to persist in its upcoming Q2 results. Wall Street anticipates revenues to come in relatively flat and adjusted EPS to plunge by 21.3%, implying continued pressures on margins. That said, market conditions are expected to improve in the second half of the year, which, along with ongoing efforts to improve operating efficiencies, is expected to lead to a major rebound in the bottom line.

Consensus revenue estimates for Q3 and Q4 indicate a return to growth for UPS, with projected revenue increases of 6.6% and 6.0%, respectively. Given the company’s sensitivity to revenue fluctuations, these gains are expected to significantly impact margins. As a result, adjusted EPS is expected to rise by 31.3% in Q3 and 9.7% in Q4.

UPS’ Valuation Seems Attractive Here

Despite the current volatility in the industry affecting UPS, I find the stock’s valuation compelling at its present levels. By adopting a forward-looking perspective and overlooking short-term fluctuations in earnings, it becomes clear that the stock is now trading at a discount following last year’s decline.

To elaborate, while UPS is trading at 18x this year’s expected adjusted EPS, this figure is influenced by depressed bottom-line numbers related to the company’s performance during the first half of the year. Profitability is expected to rebound notably thereafter, with Wall Street anticipating an 18.6% surge in adjusted EPS in FY2025. This implies that UPS is currently trading at 15.2x next year’s adjusted EPS, a rather attractive valuation for the package delivery giant.

In that sense, UPS may not necessarily look like a screaming buy before its Q2 results, which could show weakness. However, the stock does seem to present a strong buying opportunity today for investors looking to enter at a favorable price and hold this quality operator over the medium to long term.

Is UPS Stock a Buy, According to Analysts?

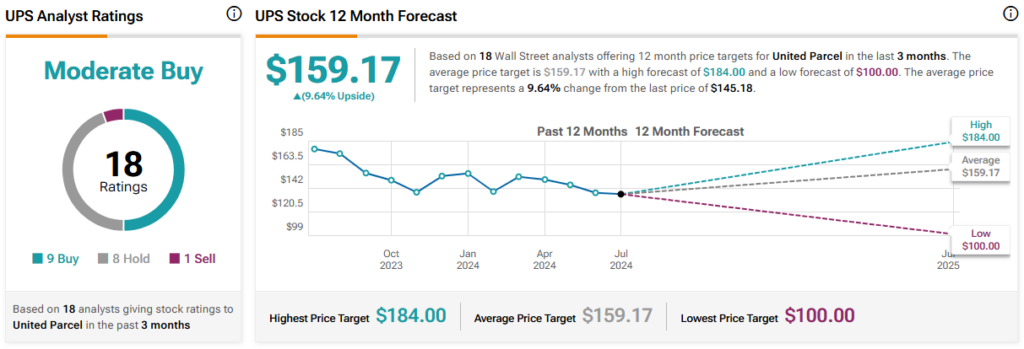

With a rebound in earnings anticipated from the second half of this year onwards, Wall Street analysts remain relatively bullish on UPS. The stock features a Moderate Buy consensus rating based on nine Buys, eight Holds, and one Sell assigned in the past three months. At $159.17, the average UPS stock price target implies 9.6% upside potential.

The Takeaway

The upcoming Q2 results for UPS are expected to show continued challenges with flat revenues and a significant drop in EPS, reflecting ongoing pressures from lower package volumes and increased costs. Despite these near-term difficulties, Wall Street forecasts signal a potential rebound in the year’s second half, driven by improved market conditions and operational efficiencies.

Accordingly, with the stock now trading at an attractive valuation relative to its future earnings prospects, I believe UPS offers a strong opportunity for investors focusing on long-term gains.