Moderna (MRNA) stock has experienced considerable volatility to start the year, and while this may interest traders, the long-term investment prospects for this stock aren’t overly attractive. The company isn’t expected to turn a profit during the forecasting period and, despite an impressive pipeline, commercialization of its more promising vaccines may still be some years away. For these reasons, I’m bearish on MRNA stock.

Moderna’s Infectious Disease Solutions

While I’m bearish on Moderna, I acknowledge that some investors might find the near-term volatility attractive. Earlier this week, vaccine-maker stocks surged on reports of rising flu and Covid-19 cases in the U.S. There have also been concerns about an outbreak of human metapneumovirus (HMPV) in China, as well as the first death in the U.S. caused by bird flu. Collectively, these outbreaks and reports have caused significant swings in this $18-billion stock.

While the HMPV virus isn’t very virulent, it can result in severe symptoms among the very young and elderly. Moderna has a vaccine trial ongoing for a two-in-one vaccine to prevent RSV and HMPV. This may have peaked investor’s interest, but it’s worth remembering that HMPV was first discovered more than two decades ago and hasn’t typically represented a major threat to humans.

With regards to bird flu, in July 2024, Moderna received a $176 million grant from the U.S. government to support the development of its H5N1 (bird flu) vaccine, which remains in the early stages of testing. As of January, the government has reported 66 confirmed cases of H5N1 in the U.S., and a vaccine is unlikely to represent a blockbuster product for Moderna. Future developments in infectious diseases may well cause Moderna’s share price to spike, but the likelihood of another Covid-type event is very low. As such, long-term investors may want to focus on the company’s pipeline and fundamentals.

Moderna’s Pipeline

Moderna’s pipeline has immense potential to benefit humankind and generate revenue but remains years away from commercialization, rendering an investment somewhat speculative. While the company’s advancements in MRNA technology and partnerships, such as with Merck (MRK) on personalized cancer therapies, highlight its innovative capabilities, most of its programs are still in clinical trial stages.

For example, the oncology collaboration, particularly the V940-Keytruda combination, is promising, with Phase III data expected by 2026. However, regulatory approvals and commercial launches could take until 2027 or later. More generally, the company’s shift from pandemic-driven revenues has been challenging. With Covid-19 vaccine sales declining, Moderna has faced financial pressures despite its substantial cash reserve. These pressures have pushed management to conduct a recent pipeline reprioritization, which aims to focus resources on high-impact programs.

Moreover, investors should consider near-term risks, including heavy research and development (R&D) spending, uncertain trial outcomes, and a competitive landscape in oncology. For now, Moderna’s pipeline is not lacking in long-term potential but requires patience and risk tolerance as the company navigates the path to commercial success.

Moderna Isn’t Expected to Turn a Profit

One of the core reasons for my bearish outlook on MRNA stock is the company’s earnings outlook. The company has pushed back its breakeven target to 2028, indicating ongoing financial challenges. This delay in profitability, coupled with reduced R&D spending, may impact Moderna’s ability to develop new products and maintain its competitive edge in the rapidly evolving biotech sector. Analysts agree with this forecast, with the consensus indicating continued losses through 2027.

A closer look at Moderna’s valuation data reveals mixed signals. The company’s Earnings-to-Sales (TTM) of 1.7 times is 53.4% below the sector median, suggesting potential undervaluation. Similarly, its Price-to-Book (TTM) ratio of 1.4 times is 40.7% below the sector median, indicating the stock may be trading at a discount relative to its book value. However, Moderna’s forward Price-to-Sales ratio of 5.1 is 35.7% above the sector median, suggesting potential overvaluation based on future sales expectations.

However, these metrics are not conclusive and aren’t always the best indicators when a company is so many years away from profitability. The absence of key valuation metrics makes it challenging for investors to accurately assess Moderna’s financial health and future prospects.

Is Moderna Stock a Buy?

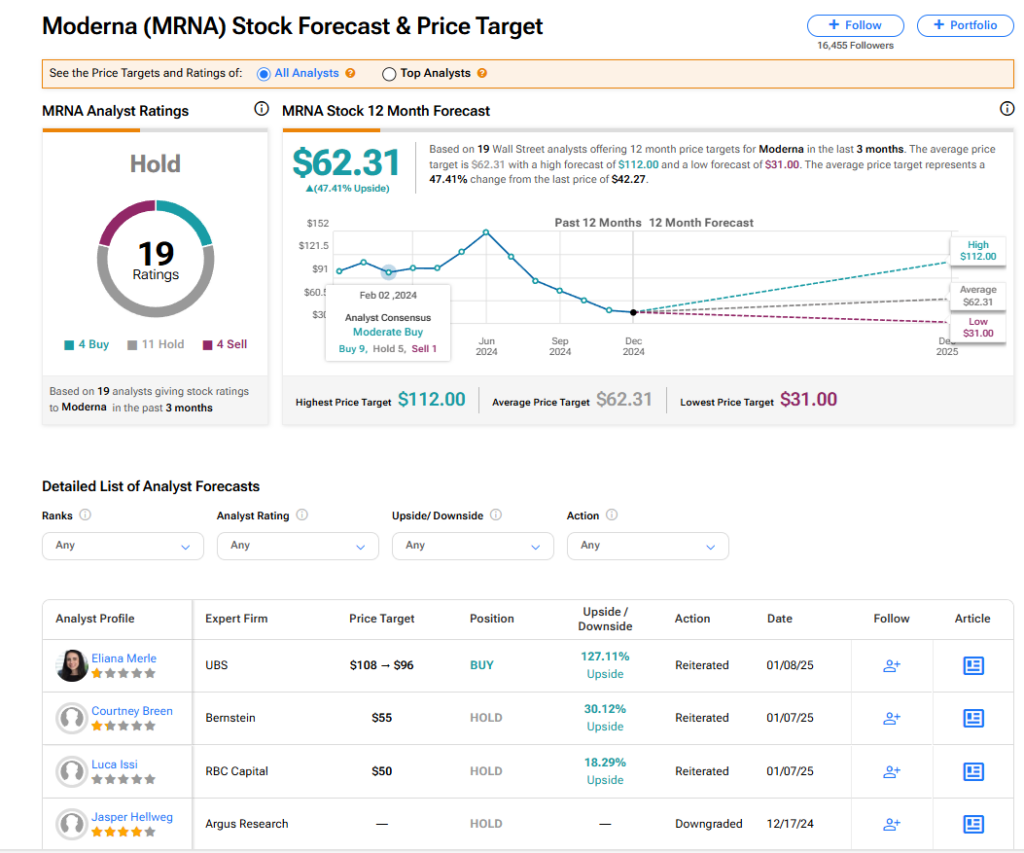

On TipRanks, Moderna’s stock has a Hold rating based on four Buys, 11 Holds, and four Sell recommendations assigned by analysts in the past three months. The average MRNA stock price target is $62.31, implying 47.41% upside potential.

Read more analyst ratings on MRNA stock

The Bottom Line on MRNA Stock

I’m bearish on Moderna due to its lack of near-term profitability and reliance on a pipeline that’s still years away from commercialization. While its MRNA technology shows long-term promise, heavy R&D spending, competition, and delayed breakeven projections to 2028 pose significant risks. Recent volatility driven by disease outbreaks highlights speculative appeal, but long-term investors may prefer companies with stronger fundamentals. With declining Covid-19 vaccine sales and limited blockbuster potential in the near future, Moderna remains a speculative investment best suited for those with patience.