Shoals Technologies (SHLS), a leading provider of critical electrical balance of system (EBOS) solutions for solar projects, has seen a rebound in its shares at year-end, as they have climbed roughly 10% in the past month. The company posted mixed results for Q3, beating revenue expectations but lagging in earnings. Looking forward, the company expects revenue for 2024 to be between $390 and $400 million, which would exceed consensus projections. Analyst confidence in the company’s earnings outlook remains relatively high, while the valuation seems reasonable, suggesting an opportunity for investors interested in industrial sector exposure.

Solar Energy Generation Is Exponentially Growing

Shoals manufactures electrical balance of system (EBOS) solutions for solar energy projects in the United States. EBOS consists of essential components that transfer the electric current produced by solar panels to an inverter, further connecting it to the power grid. Shoals’ range of EBOS elements, such as cable assemblies, inline fuses, combiners, and splice boxes, are critical to the success of solar energy operations.

Given the high stakes involved with the failure of these components, including financial loss, equipment damage, fire hazards, or even serious injury or death, customers prioritize selecting EBOS solutions based on reliability and safety rather than cost, giving the company pricing power.

The energy sector is experiencing significant transformation, driven by high power demands due to AI, onshoring, and unpredictable weather. Solar energy offers a low levelized cost of energy (LCOE) and quick deployment, yet faces hurdles due to regulatory and supply chain issues. Recent data reveals over 2,600 gigawatts of generation and storage capacity in a queue for grid interconnection, an eightfold rise within the past decade. This figure exceeds double the current installed capacity of the U.S. power plant fleet. By the end of 2023, solar, battery storage, and wind accounted for 95% of the active capacity in the queue.

Project Delays Take a Toll

The company recently announced third quarter 2024 financial results. Revenue was down year-over-year by 24%, to $102.2 million, yet it still exceeded analysts’ projections. This decline has been attributed to project delays. Despite this, gross profit saw an increase to $25.4 million from $14.2 million, resulting from a decrease in wire insulation shrink back expense, despite increased labor costs and reduced leverage on fixed costs.

General and administrative expenses also dropped to $18.7 million from $22.6 million, mainly due to lower stock-based and incentive compensation expenses. From a $10.6 million loss in the prior-year period, the company managed an income from operations of $4.5 million. The net loss significantly decreased to $0.3 million from $9.8 million.

Adjusted EBITDA and adjusted net income were both down, with the former declining to $24.5 million from $48.0 million and the latter decreasing to $13.9 million from $33.4 million. Q3 Non-GAAP EPS of $0.08 missed expectations by $0.02.

Management has issued financial guidance for the fourth quarter and 2024 overall. Projected revenue for Q4 2024 is estimated between $97 million and $107 million, with adjusted EBITDA ranging from $23 million to $28 million. For the full year 2024, the company anticipates revenue between $390 million and $400 million. Adjusted EBITDA and net income are expected to vary between $96-$101 million and $58-$62 million, respectively.

Positive Momentum and Value

The stock has been downward, shedding over 62% in the past year. It trades near the low end of its 52-week price range of $4.07 – $17.50 but shows positive price momentum by trading above the 20-day (5.00) and 50-day (5.07) moving averages. The P/E ratio of 15.24x suggests a relative discount to the industrial sector average of 19.2x.

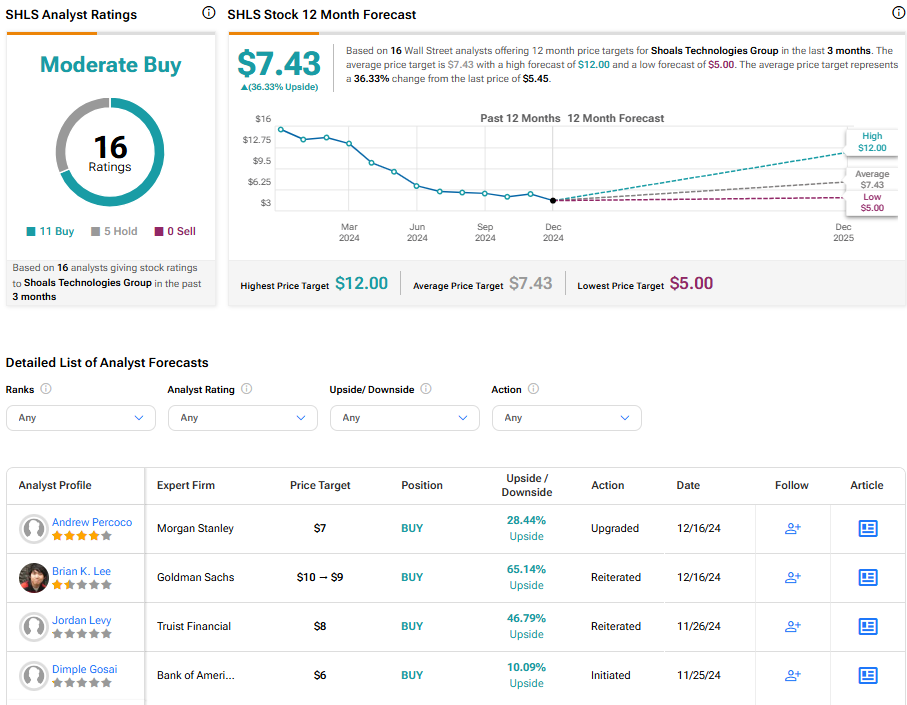

Analysts following the company have mostly been constructive on the stock. For example, Morgan Stanley’s Andrew Percoco recently upgraded the shares to Overweight from Equal Weight with a $7 price target, noting increased confidence with the earnings outlook and execution heading into 2025.

Shoals Technologies Group is rated a Moderate Buy overall, based on the recent recommendations of 16 analysts. Their average price target for SHLS stock is $7.43, representing a potential 36.33% upside from current levels.

Shoals in Summary

Project delays have led to a decline in revenue, but Shoals anticipates exceeding revenue expectations for 2024. Looking forward, the company’s stock shows positive momentum, and a P/E ratio of 15.24x indicates a relative discount to peers in the Industrials sector, offering a possible value opportunity for investors.