Shares of Plug Power (PLUG) have had a rough go this past month. The stock fell post-election on fears of what a Trump administration might mean for green energy stocks, and the company reported lower-than-expected revenues for Q3 while also lowering full-year expectations and providing future projections that fell below consensus expectations. Yet, despite these setbacks, the stock has bounced back, posting a 9.5% increase over the past few days. The company continues to carve out its position in the green hydrogen ecosystem, making it a solid long-term option for investors dedicated to green energy stocks and willing to be patient.

Plug Power Continues Its Ambitious Plans

Plug Power is building a comprehensive green hydrogen ecosystem and is leading in deploying hydrogen fuel cell technology, with over 69,000 fuel cell systems and 250 fueling stations in operation. It is also the largest purchaser of liquid hydrogen. Plug plans to construct a green hydrogen highway across North America and Europe, backed by the production capabilities of a Gigafactory. The company also plans to establish various green hydrogen production plants to be commercially operational by 2028.

For the third quarter, the company reported a significant rise in electrolyzer sales, a 285% increase quarter-over-quarter, marking an inflection point for company revenue growth. This was driven by contributions from a 5 MW system sale and a large-scale order. In the same quarter, the company announced a new order for 25 MW from a joint venture between BP and Iberdrola.

Plug Power has also effectively leveraged its internal network of hydrogen plants to improve hydrogen fuel margins. Its joint venture hydrogen plant with Olin Corporation in Louisiana is currently in commissioning, with a significant liquid production ramp-up expected in Q1 2025. Meanwhile, the company continues to increase its Basic Engineer and Design Package (BEDP) contracts, reaching an overall 8 GW globally.

Plug Powers Recent Financial Results

The company recently reported its Q3 2024 financial performance. Revenue was $173.7 million, driven by a significant appreciation in electrolyzer deployments, its in-house hydrogen network expansion, and an amplified manufacturing footprint. The firm’s operating cash flows reported a 31% improvement quarter-over-quarter, a trend expected to continue due to enhanced leverage on existing inventory and fixed manufacturing costs. However, the net loss for the quarter was $211.2 million, an improvement on Q2’s $262.3 million loss. The earnings per share (EPS) loss of $0.25 also showed improvement from a loss of $0.36 in Q2.

Following Q3 earnings, PLUG’s management has issued revised guidance, expecting 2024 revenue to fall between $700 million and $800 million. This expected rise in revenue is due to an anticipated increase in orders across their electrolyzer, cryogenic, and material handling businesses during the latter half of 2024.

Is PLUG a Buy?

The stock has been on a rollercoaster ride recently, showing volatility almost three times that of the overall market (beta 2.92) as it has cascaded downward 54% year-to-date. It trades at the lower end of its 52-week price range of $1.60 – $5.14, though it has shown some positive price momentum lately as it trades above the 20-day (2.03) and 50-day (2.08) moving averages.

Analysts following the company have taken a cautious stance on PLUG stock. For instance, BTIG Research downgraded the shares post-earnings from Buy to Neutral due to the company’s FY 2025 revenue guidance falling 20% below the consensus at the midpoint.

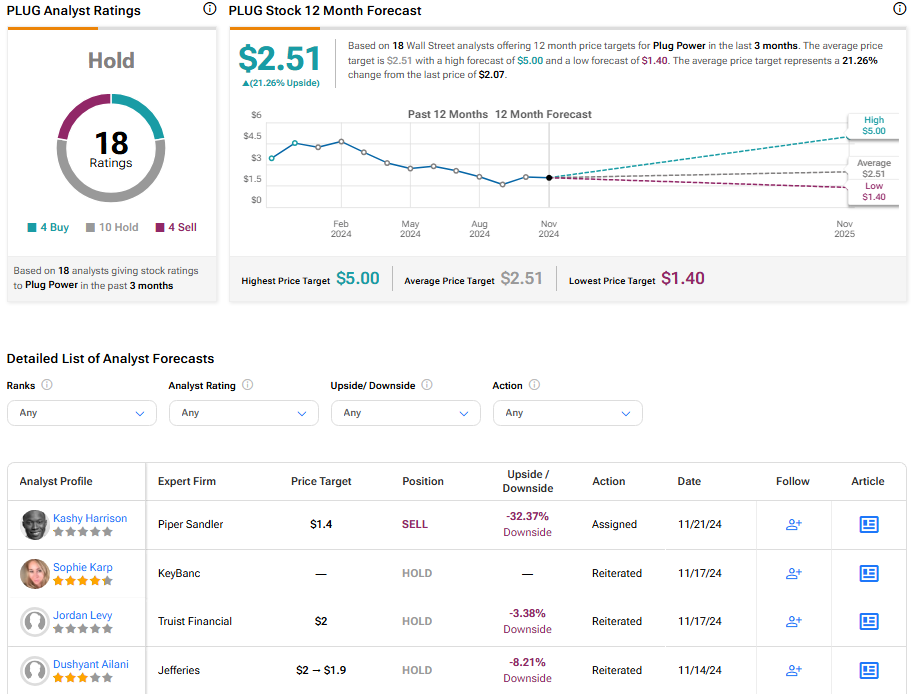

Overall, Plug Power is rated a Hold based on the recommendations of 18 analysts. The average price target for PLUG stock is $2.51, representing a potential upside of 21.26% from current levels.

Bottom Line on PLUG

Plug Power has faced considerable volatility recently, with shares taking a hit in the wake of post-election uncertainty and lower-than-anticipated revenues for Q3. However, the company’s revenue is anticipated to rise due to growing orders across various segments of its business. The rollercoaster ride of PLUG shares warrants a cautious approach. Nevertheless, the company’s progressive growth strategy and dedication to green energy development suggest optimistic prospects for patient investors.