PayPal (PYPL) has been a leader in fintech for years, but 2024 was volatile. The big question is: Has the company done enough to make it a good long-term investment? While PayPal has made big changes in its strategy and leadership, the competition is tough, and its growth story isn’t as exciting as it used to be.

If you wish to read more on PYPL, I recommend reading what our analyst at Tipranks, Oliver Rodzianko, had to say about the stock right here.

A New Era for PayPal?

Since Alex Chriss became CEO in September 2023, PayPal has been working hard to regain its edge. New projects like Fastlane, which makes guest checkouts easier, and PayPal Ads, which helps merchants use transaction data for better marketing, show that PayPal is pushing for innovation. The team now includes experienced executives like Mark Grether from Uber (UBER) and Enrique Lores from HP (HPQ), showing that PayPal is serious about change.

However, the big question is whether these efforts will lead to lasting growth.

The Competition Problem

PayPal isn’t just trying to stay relevant; it’s up against giants. Apple Pay (AAPL) is leading the mobile payments space, handling a massive $6 trillion in transactions globally and holding a 54% share of in-store mobile payments. With 640 million users and growing, Apple’s ecosystem is a big threat to PayPal’s market position.

Meanwhile, PayPal’s unbranded payment processing business, a key part of its revenue, grew by just 2% in Q4 2024, down from 29% a year earlier. This slowdown is a warning sign for investors who once saw PayPal as unstoppable in digital payments.

Is PayPal a Smart Investment Right Now?

For long-term investors, PayPal’s financials don’t look great. Revenue growth has been modest at 6.8% year-over-year, and earnings per share have only increased by 3.9%. Its price-to-sales ratio of 2.5 suggests it’s fairly valued, but its price-to-earnings ratio of 16 is higher than the sector median of 12, raising concerns about profitability.

That said, PayPal is betting big on the future. Management aims for earnings growth of low teens+ by 2027 and hopes to hit 20%+ long-term. But for now, many investors are waiting for more solid evidence before moving.

A Short-Term Play?

PayPal’s stock offers some interesting opportunities for traders. The 14-day Relative Strength Index (RSI) is around 30, suggesting a potential bounce. A short-term rally could be in the cards, making it an interesting pick for those looking for a quick gain. However, the fintech giant still has much to prove for those seeking a long-term investment.

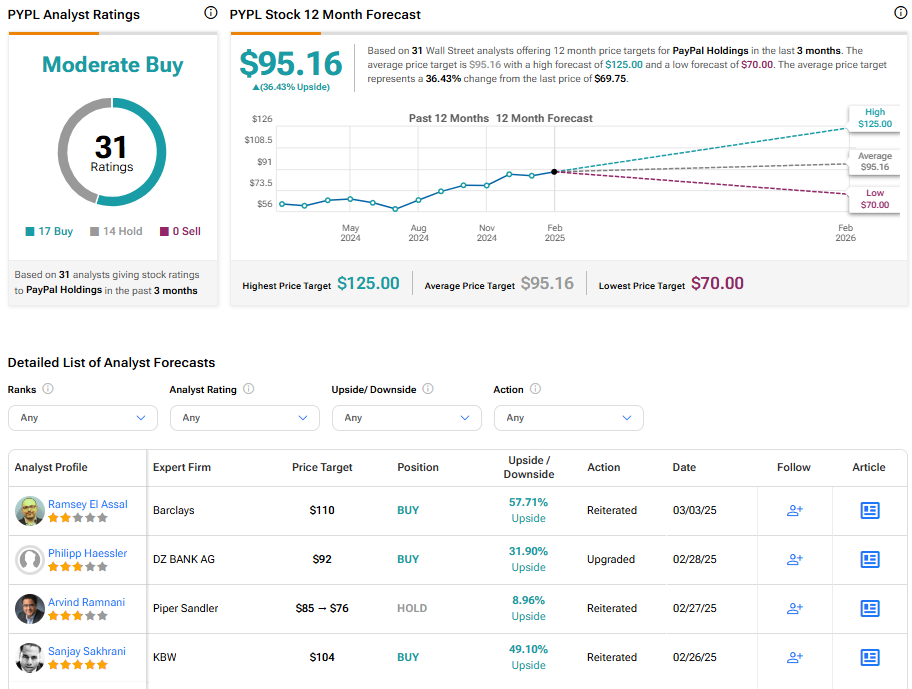

Is PYPL a Good Buy?

Turning to Wall Street, PayPal is considered a Moderate Buy. The average price target is $95.16, implying a 36.43% upside potential.

Final Verdict

PayPal’s turnaround is ambitious, but it is uncertain whether it can regain its former dominance. While the company has set the stage for future growth, competition is fierce, and its financial performance is still lacking.