Delta Air Lines (DAL) stock has continued to demonstrate elevated levels of volatility over the past couple of weeks. Last week, the stock fell on concern that rising fuel prices would put fresh pressure on costs. And this comes shortly after the company reported more than $500 million in damages due to the IT outage in the summer. Despite rising oil prices, the stock still looks like good value, as supported by the stock’s attractive earnings multiples and lofty analyst price targets. I remain bullish.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Delta’s Recent Ups & Downs

Delta Air Lines is the world’s largest airline by revenue, market cap, asset value, and fleet size. Although I’m bullish on the shares right now, the company and stock experienced significant volatility in Q3, notably following the CrowdStrike (CRWD) outage in July 2024, which caused widespread disruptions to the airline’s operations. The incident led to thousands of flight cancellations, affecting approximately half a million passengers. It ultimately resulted in substantial financial costs for the company.

Delta stock plummeted in the immediate aftermath of the incident, as investors reacted to news of the disruptions and analysts mulled the potential long-term impacts. The company initially estimated a $500 million financial hit, which included both lost revenue and additional expenses related to customer compensation and recovery efforts.

The stock dipped further when, on August 8, 2024, Delta provided more detailed financial guidance, revealing that the outage would result in $380 million in lost revenue and $170 million in additional costs for the third quarter.

However, DAL stock staged a remarkable comeback in late August and September as sentiment improved. This reflected Delta’s reassurance that full-year earnings would be at or above the midpoint of its previous guidance. This was buttressed by strong demand for travel and lower fuel costs as oil sank.

What Do Higher Oil Prices Mean for Delta?

While oil prices softened in September, they have surged again in recent weeks as the conflict between Israel and Iran, and Iran’s proxies, escalated further. In fact, the price of Brent Crude jumped 5% after U.S. President Joe Biden said the United States was discussing possible strikes by Israel on Iran’s oil industry.

Fuel costs account for a significant portion of Delta Air Lines’ operating expenses — typically between 18–20%. In Q2, Delta’s adjusted fuel expense was $2.8 billion, which was a 12% increase year-over-year, while total operating expense came in $14.4 billion, suggesting that fuel was accounting for 19.4% of costs.

Unlike many European carriers, none of the big three U.S. carriers, including Delta, hedge fuel. The strategy of fixing future prices for fuel needs is no longer widely practiced. As such, U.S. airline stocks are quite exposed to fuel price volatility and sentiment.

On the other hand, Delta does still own an oil refinery to control a portion of its fuel supply chain. The refinery benefited Delta to the tune of 20¢ per gallon in 2022 when fuel prices surged. So, while Delta doesn’t hedge conventionally, the refinery is a form of security.

Is Delta Still Good Value?

Delta still seems to have good value. For one, Delta stock trades at 8x forward earnings and given analysts’ expectations for high-single-digit earnings growth throughout the medium term, the price-to-earnings-to-growth (PEG) ratio sits at 0.94. That’s not expensive at all and represents a 49.7% discount to the industrials sector as a whole.

Furthermore, the airline is set to deliver Q3 earnings on October 10, with analysts forecasting earnings per share (EPS) of $1.55 and revenues of $15.1 billion. All of the last 15 revisions have been downgrades due to the CrowdStrike outage.

Also, the impact of CrowdStrike event appears to have been essentially nullified by a stronger-than-expected civil aviation trends. Airline stocks rose in late September as Southwest Airlines (LUV) raised its Q3 revenue forecast and authorized a $2.5 billion buyback plan. The company also announced cautious capacity guidance that supports industry pricing, with 1% and 2% growth in 2025 and 2026 respectively. Southwest said it would reduce flights from Atlanta, which is Delta’s home.

A Word on Hurricane Milton

It’s important to note that, at the time of writing, U.S. airlines have braced themselves for Hurricane Milton’s arriving impact on Florida, with over 1,700 flights canceled on Wednesday 9 October. Major airports, including Orlando and Tampa, are closed, disrupting travel plans. Delta has canceled 207 flights, fewer than Southwest, but still a significant number. The hurricane is expected to bring life-threatening conditions, but may also cause lasting damage to civil aviation infrastructure. This will likely cause another significant one-time financial cost on Delta.

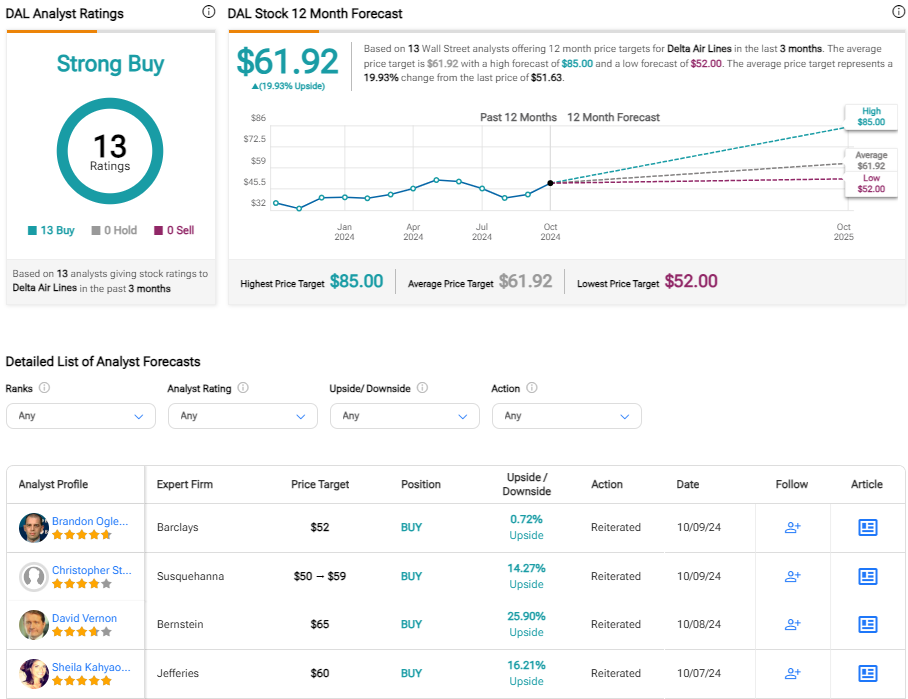

Is Delta Stock a Buy, According to Analysts?

On TipRanks, DAL comes in as a Strong Buy based on 13 Buys, zero Holds, and zero Sell ratings assigned by analysts in the past three months. The average DAL stock price target is $61.92, implying nearly 20% upside potential.

The Bottom Line on Delta Stock

Delta Air Lines stock trades at a handsome discount to the average Wall Street share price target and carries appealing P/E and PEG ratios. The company has seemingly overcome the challenges presented by the CrowdStrike outage and looks set to deliver EPS above the previously guided midpoint. Rising oil prices could represent a near-term concern, but I’m bullish overall.