Broadcom (AVGO), one of the most important semiconductor and infrastructure software players, recently reported its third-quarter earnings for Fiscal 2024. Despite the company posting impressive revenue and earnings growth, the stock dropped on the announcement, raising questions about whether the pullback presents a buying opportunity. I believe this is indeed the case. While Broadcom’s valuation might seem rich, the company’s leading role in the chip space makes it worth a premium. Accordingly, I am bullish on the stock.

Broadcom’s Q3 Growth Driven by AI and VMware

Let’s begin by reviewing Broadcom’s Q3 results, which showed its top-line revenue reaching $13.1 billion, up 47% from the previous year. This marks the best year-over-year growth Broadcom has posted in the past six years and demonstrates a strong upward trend. The growth was driven by multiple factors, including rising demand for AI solutions and the contribution of VMware, the cloud computing firm that Broadcom acquired for $61 billion in 2023.

During the company’s earnings call, Broadcom CEO Hock Tan stated that AI-related revenue keeps snowballing, driven by a mix of networking hardware and custom AI accelerators. The company’s AI solutions have become integral to hyperscalers’ data centers. As for VMware, it contributed $3.8 billion in revenue during Q3 through Broadcom’s infrastructure software segment, leading to 200% year-over-year growth.

Tan also emphasized that the VMware Cloud Foundation (VCF) is seeing strong adoption, particularly among enterprise data centers. Overall, the integration of VMware appears to be going smoothly, helping to power Broadcom’s industry-leading growth in both hardware and software markets critical to the AI infrastructure buildout. Looking ahead, management forecasts Q4 revenue of $14 billion, which suggests year-over-year growth of 51%. The guidance indicates that Broadcom’s momentum is likely to remain vigorous, particularly in AI and enterprise software.

AVGO’s Margins and Profitability Remain Strong

Let’s now move down the income statement to margins and profitability. Some investors expressed concern that Broadcom’s gross margin saw a decline, notably in the semiconductor segment. The semiconductor solutions division, which made up 56% of total revenue, posted a gross margin of 68%, down 270 basis points year-over-year. This decrease was largely due to a higher mix of custom AI accelerators, which tend to have lower margins. Regardless, Broadcom’s overall profitability remains impressive.

The company’s operating margin for the quarter was 61%, with an adjusted operating income of $7.9 billion, up 44% from a year earlier. The infrastructure software segment saw a particularly strong operating margin of 67%, reflecting high margins for the VMware business.

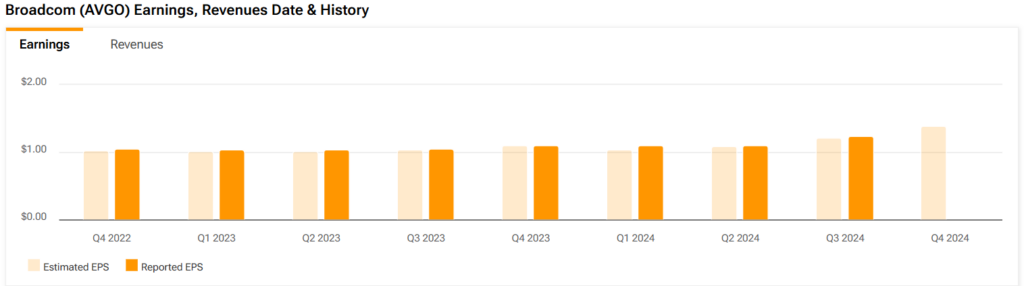

Broadcom’s adjusted earnings per share (EPS) rose an impressive 18% to $1.24, while the company generated $4.8 billion in free cash flow during the quarter, equal to 37% of revenues. CFO Kirsten Spears noted that, despite increased expenses related to the VMware acquisition, Broadcom is on track to maintain solid cash flow, bolstered by its efficient cost structure. As such, investors should continue to expect impressive bottom-line results from Broadcom in the coming quarters.

A Premium Valuation

Now that we have examined Broadcom’s financial results, let’s look at whether the post-earnings stock price drop has created a buying opportunity. I believe it has. The stock might seem expensive, trading at nearly 29 times this year’s expected EPS of $4.85. However, it’s important for investors to understand why AVGO commands a premium price and why the current valuation is not unreasonable.

Broadcom is unique in that it is gaining ground in both AI-enabling hardware and enterprise software. The company supplies key components for hyperscale data centers, which are fueling the next generation of AI computing. Adding VMware has cemented the company’s role in software infrastructure, particularly in cloud and on-premise enterprise solutions. Broadcom’s products are critically important to modern networks, data storage, and computing environments.

Also, management’s guidance for AI-related revenues of more than $12 billion in 2024 suggests Broadcom’s momentum is building. I believe that this AI-driven demand, coupled with Broadcom’s leadership in networking technology, justifies the premium valuation. Given how rapidly the company’s earnings are growing, Broadcom’s stock could experience a margin expansion moving forward.

Is AVGO Stock a Buy, According to Analysts?

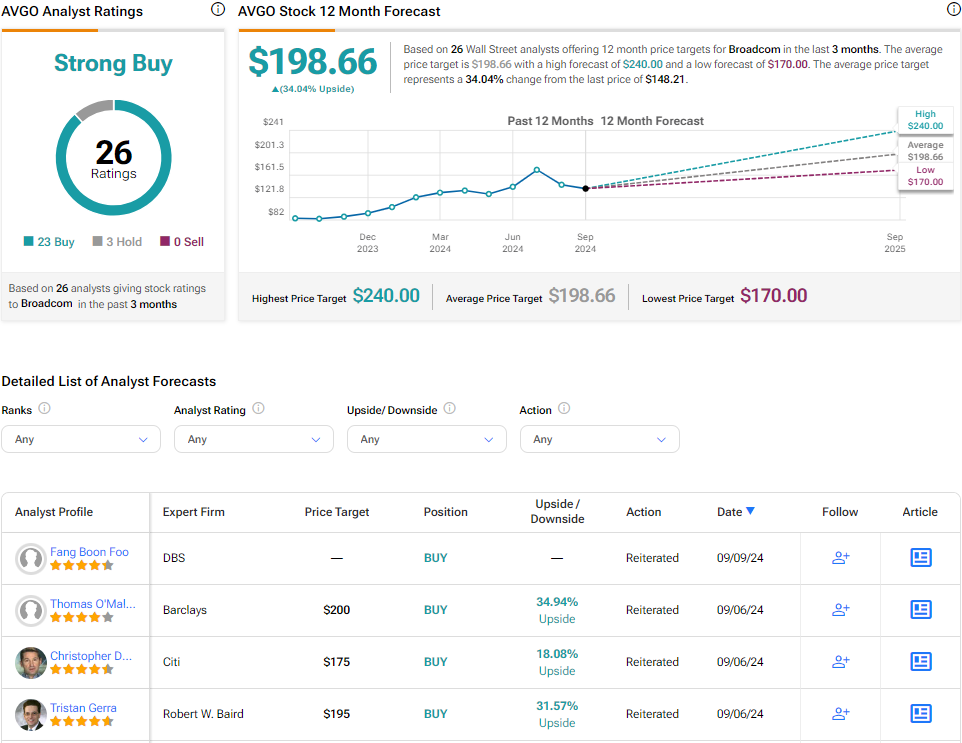

Wall Street’s view on the stock remains bullish despite the recent pullback. Broadcom currently has a Strong Buy consensus rating based on 23 Buy and three Hold recommendations assigned in the past three months. At $198.66, the average AVGO stock price target implies 34% upside potential.

If you’re wondering which analysts to follow if you want to buy and sell AVGO stock, the most profitable analyst covering the stock (on a one-year timeframe) is Vivek Arya from Bank of America Securities (BAC), with an average return of 54% per rating and an 84% success rate.

Conclusion- AVGO Is Critical in AI Infrastructure and Enterprise Software

To sum up, Broadcom’s Q3 results highlighted its critical role in both AI infrastructure and enterprise software, with the VMware acquisition starting to bear fruit. Despite a modest decline in semiconductor margins, the company’s overall profitability remains strong, backed by solid cash flow and accelerating AI revenues.

While Broadcom’s valuation may seem rich, the company’s strong position in the market, particularly in AI and data center solutions, justifies a premium. For these reasons, I remain bullish on the stock and believe that it presents a solid buying opportunity for long-term growth investors.

Questions or Comments about the article? Write to editor@tipranks.com