My long-term investing strategy centers on buying high-quality businesses on sale and holding them for the long haul. Comprised of 30 of the best businesses in the world, the Dow Jones Industrial Average (DJIA) stands out as one of the most prominent stock market indices. One of the more heavily weighted stocks in the index is the pharmaceutical giant, Amgen (AMGN). Overall, I am bullish enough about the stock to initiate coverage with a Buy rating.

In my view, the company’s third-quarter results made it clear that its operating fundamentals are healthy. Amgen’s deleveraging efforts are also coming along. The dividend is well-covered, with room to keep growing. Finally, the stock looks to be a solid value at the current share price.

Amgen Delivers a Standout Third Quarter

On October 30th, Amgen shared third-quarter earnings, which were supportive of my Buy rating. The company’s total revenue surged 23.2% higher over the year-ago period to $8.5 billion. This was in line with the analyst consensus for the quarter. The company’s topline growth was primarily driven by its acquisition of Horizon Therapeutics. Backing this acquisition out of the mix, product sales still would have grown by 8%, thanks to 12% volume growth. That was fueled by double-digit sales growth from 10 of its products, including the bad cholesterol-lowering drug Repatha and the post-menopausal osteoporosis drug Evenity. Amgen’s non-GAAP EPS climbed 12.5% year-over-year to $5.58. This exceeded the analyst consensus by $0.31.

Catalysts Are Emerging for Amgen

Amgen also looks poised to keep delivering for shareholders in the future, which backs up my Buy rating. The company has a few developments that will arguably provide tailwinds. More immediate boosts shortly include the launch of biosimilars for major drugs. EVP of Global Commercial Operations Murdo Gordon noted in his opening remarks that the company recently launched Pavblu in the U.S., a biosimilar to the blockbuster eye injection Eylea. Gordon went on to indicate that feedback from customers has been enthusiastic thus far, which should be a positive for the uptake of the drug. Amgen is also preparing to launch its Stelara biosimilar, called Wezlana, in the U.S. in the first quarter of 2025. The U.S. launch of its Soliris biosimilar, named Bekemv, is expected to follow in the second quarter.

CFO Peter Griffith indicated that the integration of Horizon is progressing well. The company expects to reach $500 million in pretax cost synergies by year three post-acquisition. The majority are anticipated to be realized by the end of 2024. Amgen also has dozens of compounds in various stages of clinical development for numerous indications. That means the company should have plenty of product launches coming, not just in 2025 but far beyond. As a result, the analyst consensus is that non-GAAP EPS will rise by 6.8% in 2025 to $20.82. Another 3.2% increase in non-GAAP EPS to $21.49 is being anticipated for 2026. These come on top of a projected 4.5% uptick in non-GAAP EPS to $19.49 in 2024.

Amgen’s Dividend Is Safe and the Balance Sheet Is Improving

Amgen’s 3.4% dividend yield registers at twice the healthcare sector average yield of 1.6%, which is another reason for my Buy rating. This superior starting income is bolstered by a low payout ratio: In 2024, Amgen’s payout ratio is likely to be in the mid-40% range, which leaves it with the flexibility to keep handing out dividend hikes, like its most recent 5.8% increase announced earlier this month. In other words, Amgen offers an ideal mix of immediate income and future income growth.

Following its Horizon acquisition, the company is also paying down debt at a solid pace. In the third quarter, Amgen retired $2.5 billion of debt. According to Griffith, this puts the company on track to return to its pre-Horizon acquisition capital structure by the end of 2025. That explains why S&P Global (SPGI) awards an investment-grade BBB+ credit rating to Amgen.

AMGN Stock Could Be Discounted

Amgen’s valuation is what puts my bullish case over the top. The stock is priced at a forward P/E ratio of 12.6, which is moderately less than the 10-year normal P/E ratio of 14.6. In my view, this offers an attractive entry point into the stock. This is because Amgen’s mid- to high-single-digit annual non-GAAP EPS growth potential is about in line with its 10-year average of 7.8%. That’s why I believe fair value is right around $300 a share, which would provide a solid upside from the present valuation.

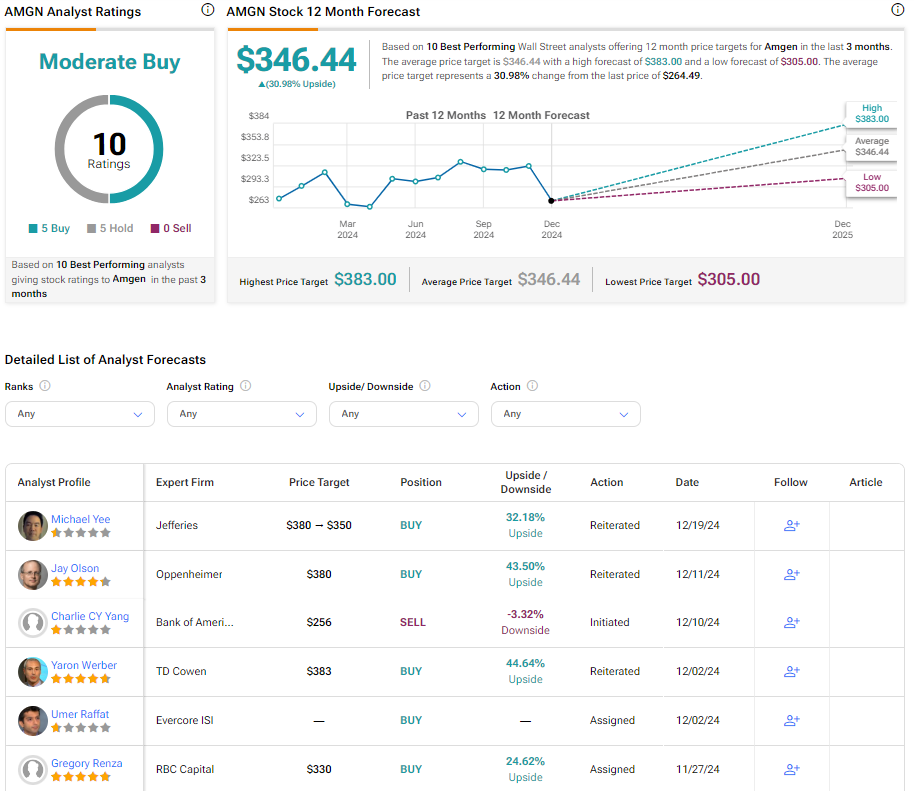

What Is the Future of Amgen Stock?

Shifting to Wall Street, analysts have a Moderate Buy rating consensus on Amgen. Among 10 analysts, five have assigned Buy ratings, and another five have issued Hold ratings in the past three months. The average 12-month price target of $346.44 suggests a 30.98% upside from the current share price.

Key Takeaway

As one of the largest pharmaceutical companies in the investment universe, Amgen is a qualitative player in its space. The company possesses both an admirable existing drug portfolio and an equally impressive drug pipeline. Amgen also has the means to keep growing its payout to shareholders in the years to come. Best of all, the valuation is reasonably cheap. Ergo, the rationale for my Buy rating.