iRobot Corp (NASDAQ:IRBT), the maker of autonomous home appliances, is at a critical juncture after a failed merger with Amazon (NASDAQ:AMZN). While strategic restructuring by the interim CEO aims to return the company to financial stability, IRBT stock is trading at all-time lows. The stock may potentially offer value with upside potential at these levels. That said, market pressures and uncertainties warrant caution, as reflected in the analysts’ consensus rating.

The Journey Thus Far

Massachusetts-based iRobot Corp was founded in 1990 by a trio from MIT’s Artificial Intelligence Lab to build groundbreaking robots, initially for space exploration and military defense. Since then, the company has evolved into creating autonomous home appliances, including the popular Roomba vacuum cleaners and Braava floor moppers.

In August 2022, Amazon announced a planned takeover of iRobot for $1.7 billion. After intense antitrust scrutiny from the European Commission, the takeover deal was called off in January 2024.

The fallout resulted in a $94 million reverse breakup fee paid by Amazon, a substantial operational restructuring of the company, including a 31% reduction in the company’s workforce, and the departure of CEO Colin Angle.

Tough Road Ahead

Despite facing stiff competition and dealing with the impact of the canceled Amazon merger, the iRobot team trudges on. Interim CEO Glen Weinstein has committed to financial stability by managing cash responsibly and improving liquidity while executing the operational restructuring plan, which aims to simplify the cost structure and create a sustainable business model.

It will be a tough road, as evidenced by the financial results for the fourth quarter and full year ending December 30, 2023. iRobot’s revenue was $307.5 million compared to $357.9 million last year (a 14% slide), and adjusted loss per share increased to $1.82 from a net loss per share of $1.54 last year (though beating analysts’ expectations of a loss per share of $2.11).

Management expects full-year 2024 revenue between $825 and $865 million and a net loss per share in the range of $3.30 to $3.73.

What is the Outlook for IRBT in 2024?

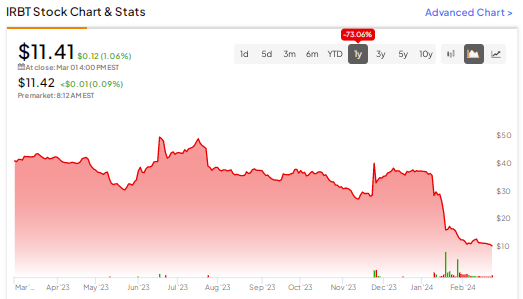

Shares of IRBT are trading at the low end of the 52-week range of $11.52 to $51.49, below the 20-day moving average price of $14.93 and a 50-day moving average price of $21.86. It is currently trading below industry and historical averages on a Price-to-Book and Price-to-Sales basis, so may represent a value at this level.

In a recent research note, Needham analyst James Ricchiuti reiterated a Hold rating, saying that the earnings call clearly reflected the challenges ahead for iRobot. While the company is taking initiatives to improve its gross margins, the analyst thinks that “it’s a tall order, in our view, given the competitive landscape and difficult macro.”

IRBT has a Hold consensus rating based on ratings by two Wall Street analysts in the last three months. The average price target is $14.00, representing 22.7% upside from current levels.

Final Sweep

iRobot’s performance for 2023 and the Amazon merger fiasco indicate a struggle to regain footing. However, the new leadership shows commitment to drive the company back to financial stability with a robust operational restructuring plan.

iRobot’s projections for 2024 suggest a challenging road ahead. The ongoing market pressures and uncertainties highlight the importance of caution for potential investors.