Invitation Homes (NYSE:INVH) has managed to withstand rate hikes relatively well in recent quarters. The residential REIT, which owns about 85,000 homes in 16 states, has seen its profitability and overall growth prospects being negatively affected, but its overall performance has remained robust. In fact, profits are expected to hit new records this year despite the likelihood of rates remaining high. Regardless, I believe the stock’s valuation is quite pricy. Accordingly, I am neutral on INVH stock.

The Effect of High Interest Rates on Invitation Homes’ Performance

Invitation Homes’ performance, as is the case with all of its sector peers, is not immune to interest rate hikes. In fact, interest rate increases generally pose significant challenges for REITs, particularly those focusing on residential properties, like Invitation Homes.

This is mainly because rising interest rates translate to rising interest expenses, which can considerably impact a REIT’s profitability. At the same time, higher interest rates act as a deterrent to expansion efforts via acquisitions. The mounting cost of borrowing to acquire properties effectively becomes prohibitive under such conditions.

This explains why real estate stocks have underperformed the overall market considerably over the past couple of years. In the wake of the COVID-19 pandemic, wild consumer spending and an influx of cash into the financial system fueled rampant inflation. In an effort to temper the economy, the Federal Reserve enforced sharp interest rate hikes between 2022 and 2023, with the real estate sector being the first to take a strong hit.

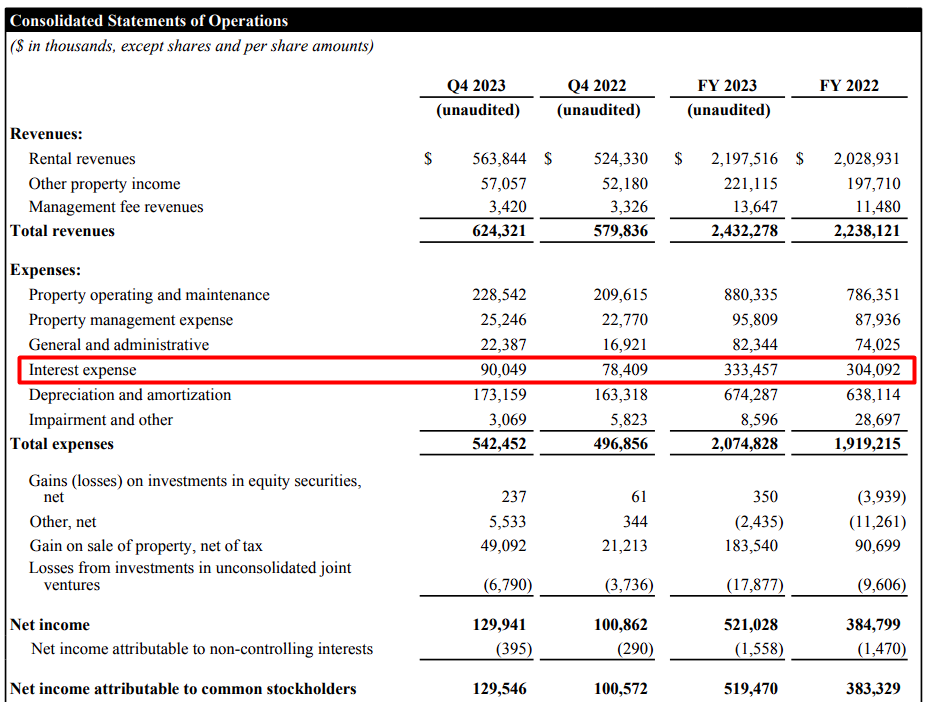

Nevertheless, INVH managed to withstand the sharp interest rate increases somewhat well. A look at its FY-2023 results clearly illustrates this. As you can see in the image below, while interest expenses grew by nearly 10% to $333.5 million, this is nothing compared to the massive increases seen in the reports of most REITs. Many REITs experienced year-over-year increases of 40%, 50%, and 60%, with some even seeing their interest expenses double, especially those with significant exposure to variable rates.

The reason Invitation Homes fared better is due to its healthy leverage and favorable credit position. The company did end the year with what appears to be a startling total debt position of $8.6 billion. However, this amount stands against $17.3 billion worth of residential properties.

Further, Invitation Homes benefit from a well-staged debt maturity ladder. At the end of the year, its debt had five years of weighted average maturity, meaning that Invitation Homes is not in a hurry to refinance a notable chunk of its debt soon, with interest rates quite high. The company, thus, managed to keep its borrowing costs under control and maintain a rather low weighted average interest rate of just 3.82%. In the meantime, only about $3.9 billion of its debt had exposure to variable rates at the end of the year.

Consequently, the company was able to maintain solid profitability. Its core FFO/share (funds from operations per share, a cash-flow metric used by REITs) rose from $1.67 to $1.77 for the year, and management also forecasts profits breaking new records in FY2024.

Notably, the company expects same-store core NOI growth of 3.5% to 5.5%, which is expected to drive same-store NOI growth per share of about $0.10. In the meantime, rising interest rates are expected to negatively impact FFO/share by just $0.03. Along with a couple of other factors involved, FFO/share is expected to rise to $1.86 at the midpoint of management’s outlook for the year.

INVH Stock’s Valuation Remains Rich, Nonetheless

Invitation Homes has managed to withstand the ongoing headwind from rising interest rates better than the average REIT. However, I believe that the stock’s investment case is being hindered by the notion that its valuation remains rather rich. At about 19 times the midpoint of management’s FFO/share outlook, the REIT appears quite richly valued. For context, the sector’s median forward price/FFO multiple stands at 12.9 times, a massive difference from that of Invitation Homes.

One could argue that Invitation Homes’ qualities deserve a premium valuation. These qualities include a robust property portfolio with an excellent occupancy rate of 95.7% and a favorable credit profile.

Nevertheless, the stock offers a thin dividend yield of 3.2% at its current price. Even if the company sustains a decent dividend growth pace (the most recent hike last December was by 7.7%), the stock’s capital return profile appears weak in the current market landscape. Given that rates are expected to stay high due to the continued strength of the economy, Invitation Homes’ praiseworthy yet modest growth and below-average yield can hardly justify owning the stock against the market’s current “risk-free” rate.

Is INVH Stock a Buy, According to Analysts?

Looking at Wall Street’s sentiment on the stock, Invitation Homes features a Moderate Buy consensus rating based on eight Buys and eight Holds assigned in the past three months. At $37.67, the average Invitation Homes stock forecast implies 8.8% upside potential.

The Bottom Line on INVH Stock

Overall, Invitation Homes has certainly exhibited resilience in the face of rising interest rates, outshining many of its sector peers. The company’s results are also poised to remain strong this year, even if interest rates remain high, backed by a strong property portfolio and a favorable credit profile. Nevertheless, the stock’s valuation appears rich, particularly when considering the modest capital return prospects. Thus, I suggest that investors ought to be cautious before considering Invitation Homes stock.