Business owners of any size know how crucial keeping track of accounting can be, and Intuit (INTU) makes it that much easier with its line of financial software tools. Recently, Intuit offered up a look at its own financials. Those reports delivered fantastic results and sent the stock higher in after-hours trading today. Intuit’s earnings report featured wins all around, with the company posting adjusted earnings of $1.10 per share. That was well past TipRanks estimates that called for $0.98 per share.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Revenues also came in ahead of forecasts; Intuit posted $2.41 billion in sales against FactSet estimates that called for $2.34 billion.

Intuit took a bit of a hit this quarter, however, thanks to a tax filing deadline in the United States that came earlier than normal. Despite this hit, the company ultimately came out on top of estimates.

Intuit’s results are good enough on the surface to catch attention, but a closer look at where all that revenue came from offers an even brighter outlook. The company has a range of tools for businesses of all sizes. That’s going to give it an edge in the field, and that’s why I’m bullish on Intuit.

The last 12 months for Intuit shares are down somewhat so far. A year ago, at this time, Intuit was just over $550 per share. Mid-November got Intuit up over $713 per share.

That high didn’t last long, though, as, by mid-May, Intuit lost nearly half of its value, dropping to as low as ~$339. Now, the stock is near $474 in after-hours trading.

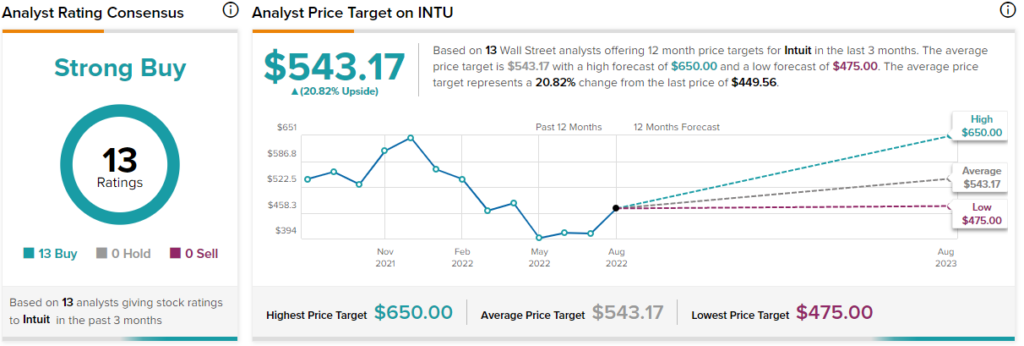

Is Intuit a Good Stock to Buy?

Turning to Wall Street, Intuit has a Strong Buy consensus rating. That’s based on 13 Buys assigned in the past three months. The average Intuit price target of $543.17 implies 20.82% upside potential.

Analyst price targets range from a low of $475 per share to a high of $650 per share.

Investor Sentiment May Prompt Some Concerns for INTU Stock

Financial software has long been valuable enough to make the companies that offer it powerhouses in the field. Intuit is one such powerhouse; it currently has a Smart Score on TipRanks of 9 out of 10, suggesting an “outperform” rating. This suggests that Intuit has an excellent chance of doing better than the broader market. Considering the state of the overall market these days, that’s a point worth knowing. Despite that clear win, however, Intuit isn’t regarded as a universal win.

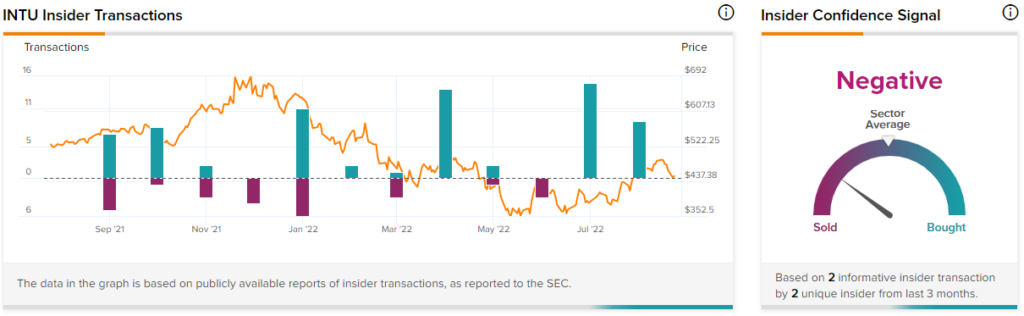

Insider trading at Intuit is somewhat Buy-weighted, but it’s a fairly complex story here. Much of the insider trading activity in the last three months is focused on buying. However, the buying is uninformative buying, which weighs less on perception than informative activities do.

Thus, the fact that there have been 24 Buy transactions against just three Sell transactions should make Intuit seem like a champ. However, all of the Buys—and just one of the Sells—have been uninformative. Two Sells, from director Raul Vazquez and Executive Vice President of People and Places Laura Fennell, were the only informative transactions seen in the last three months.

Going back over the last year, however, is a different matter. Over the last year, insiders staged 71 Buy transactions, but only 26 Sell transactions overall. While insider confidence overall is considered negative, there’s also a solid body of evidence here that says things could be looking up.

A Bright Future, but Not Without Potential Trouble

Looking at Intuit in aggregate suggests a very positive future ahead. However, potential investors will do well to keep an eye on some potential problems to come.

A look at the company’s numbers for this quarter makes one thing clear: it is not dependent on any one point to succeed. The company grew Credit Karma revenue to $1.8 billion, and its Consumer Group revenue was up 10% overall this year, hitting $3.9 billion in total.

Intuit’s Small Business & Self-Employed Group revenue was up 38%, and Online Ecosystem revenue was up 61%. Better yet? When Intuit lost money to that early IRS filing deadline, the revenue from Mailchimp made up for part of it.

It’s clear that Intuit has a nicely diversified product line and market base that should allow it to weather economic downturns quite well. Certainly, some parts of that market base will experience a downturn, if not outright closure. Permanently closed businesses really don’t need email marketing tools or accounting software. That’s going to hit Intuit somewhat.

However, it’s just as clear that elements of Intuit’s market base will survive the downturn. That means they’ll keep buying Intuit products, and Intuit will likely come out the other side of an economic downturn whole and breathing.

In fact, there are signs that Intuit is augmenting its potential customer base further with new products and tools. Intuit’s Chief Technology Officer, Marianna Tessel, recently detailed how the company was using both artificial intelligence and machine learning to help small businesses better “categorize their data.”

This is a practice Intuit calls “AI at scale.” It should dovetail well with analytics programs to produce insights that businesses can put to work right away.

Intuit also has a stake in a new startup called Fernish. Fernish lets customers rent furniture. They can either buy it on a rent-to-own basis, or they can return it when finished. Fernish’s big difference is that it targets the higher-end consumer – generally, a professional who may have to move several times over the course of his or her career.

How that will turn out is anyone’s guess, but it’s not a bad idea. Right now, businesses are clamoring for help, so the idea that there will be a lot of mobility is sort of slim.

However, if that changes—like in a serious economic downturn—businesses may be able to demand that kind of flexibility from their employees once more. That should make Fernish attractive to investors and customers alike.

Conclusion: Too Much Positive Momentum to Ignore

Intuit has terrific potential to survive an economic downturn. Its focus on accounting and marketing will make it a big part of businesses desperate to survive the downturn themselves. It definitely doesn’t hurt that there’s so much upside potential left, according to analysts. Even with the surge in after-hours trading, Intuit is still trading just under its lowest price target. It’s got quite a way to go to even hit the average, which suggests some more recovery to come.

Granted, that three-figure price tag per share will scare off smaller investors and thus limit the pool, but take a widely-diversified product line that will draw interest as long as a business’ doors remain open, and that’s a recipe for likely success.

Sure, the insider picture is a little worrying. Potential economic downturns will hit Intuit in much the same way they will hit everyone else.

I remain bullish on Intuit, however. It’s got the product line, the market base, and the willingness to expand, which is what it will need to succeed in these conditions.