It’s time for Intel (NASDAQ:INTC) to get an upgrade. However, for investors feeling the pain of holding a stock that has mostly taken a beating in recent times, the message is to not get too excited by the reappraisal.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Having seen his bearish thesis play out since last July’s initiation of an Underperform (i.e., Sell) rating, Wolfe Research’s Chris Caso, an analyst ranked amongst the top 1% of Street stock experts, has now upgraded his rating to Peer Perform (i.e., Neutral) without offering a fixed price target. (To watch Caso’s track record, click here)

That said, Caso makes it clear his “cautious thesis” hasn’t suddenly turned positive. But given how far the stock has fallen (down 36% year-to-date while trailing the main semiconductor index, the SOX, by 55%), Caso believes the issues underlying the bear case are now understood. The information provided by the company during its foundry event and recent earnings have confirmed the 5-star analyst’s thesis, while “sentiment toward the stock is low.”

The central argument of Caso’s “cautious thesis” is that the chip giant’s current server CPU growth is insufficient to cover the substantial CapEx (capital expenditures) and depreciation costs associated with the company’s 5N4Y (five-nodes-in-four-years) manufacturing strategy. This concern is underscored by the recent disclosure indicating that its manufacturing operations are not expected to break even until CY2027. Furthermore, reaching profitability will necessitate a significant expansion of the foundry business by the end of the decade.

“That said,” Caso goes on to add, “this is now part of investor expectations, and we do expect some incremental GM improvement in CY25 as startup costs decline and as INTC begins to take more tiles in house, albeit modestly.”

Gross margin improvement between 2024 and 2026 is likely to be supported by a “cyclical recovery” in the PC and server markets, as well as a reduction in start-up costs. However, Caso anticipates a significant part of this benefit will be offset by the effects of tile outsourcing in 2025 and 2026. “While headwinds from outsourcing begin to recede in CY26, we don’t expect meaningful GM improvement until 2027+,” the analyst further said.

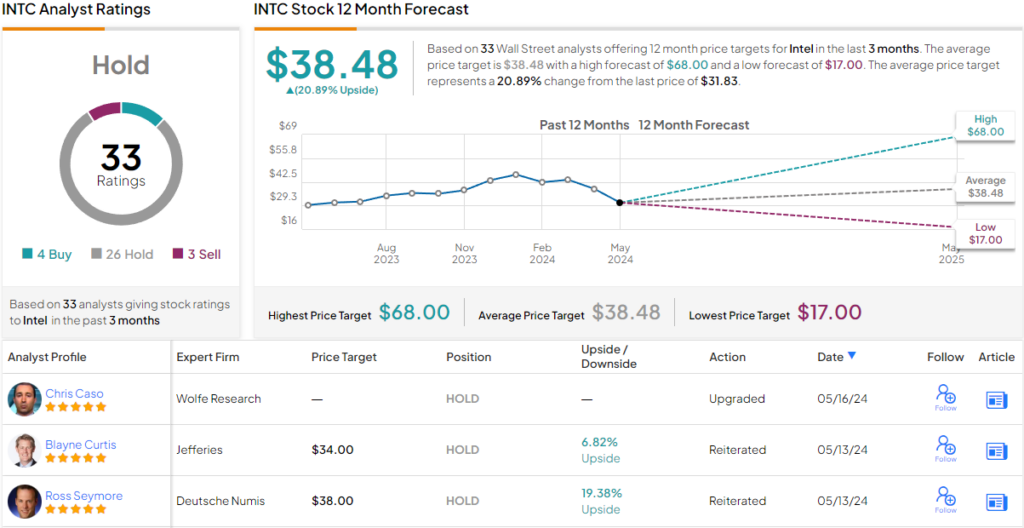

Turning now to the rest of the Street, where most analysts agree with the Wolfe take. Based on an additional 25 Holds, 4 Buys and 3 Sells, the consensus view is that Intel stock is a Hold. That said, at $38.48, the average price target points toward 21% gains over the next year. (See Intel stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.