Chipmakers have been an important driver of the tech revolution, but the rapid growth of AI made them even more essential. AI depends on chips for executing complex computations and processing data at high speeds, powering machine learning and deep learning tasks.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

And as the need for AI-related chips has surged, investors have been leaning into the opportunity to capitalize on the growing demand with shares of semi firms reaping the benefits.

That said, not all chipmakers have thrived equally. While some firms have taken full advantage of this surge, others have struggled to keep pace. Yet, even those currently trailing may soon catch up and join the boom.

With that in mind, Raymond James analyst Srini Pajjuri has been taking the measure of two industry giants, Intel (NASDAQ:INTC) and Micron (NASDAQ:MU), and he sees an opportunity being more pronounced in one than the other. Let’s dive deeper into both to see what’s behind Pajjuri’s analysis.

Intel

We’ll start with Intel, a company that might be a fitting description of the term “fallen giant.” The chipmaker’s downfall can be attributed to a combination of factors – botched opportunities, leadership missteps, and increased competition have all had their part to play.

For years, Intel dominated the semiconductor market, but its failure to innovate quickly enough—particularly in areas like mobile processors and advanced manufacturing—allowed competitors like AMD to gain ground. Product delays, along with internal struggles and a lack of strategic vision have left the company playing catch-up in a market that is evolving at a fast pace.

Meanwhile, the shares have been taking a proper hammering, having retreated by a huge 60% year-to-date. A look at the company’s latest earnings release, for Q2, makes the bear case clear to see. Revenue fell by 0.9% year-over-year to $12.83 billion, missing the consensus estimate by $150 million, while adj. EPS of $0.02 also fell short of expectations – by $0.08. There was more disappointment with the outlook too; Intel called for Q3 revenue in the range between $12.5 and $13.5 billion, and adj. EPS of $(0.03), well below the respective $14.39 billion and $0.31 expected on Wall Street.

While the company has been focusing its efforts on a turnaround, Raymond James’ Srini Pajjuri sees too many issues piling up and has therefore altered his stance on the chip giant.

“AI PC growth is turning out to be a bigger headwind to margins as the higher cost of external wafers is more than offsetting modest ASP premiums” Pajjuri explained. “While management sounded confident about longer-term targets, GM headwinds are expected to persist through 2025, and we see limited incremental revenue drivers near-term. As such, we expect profitability to remain under pressure and are moving to the sidelines despite the attractive valuation (<1x P/B) and our view that an eventual Foundry separation could unlock significant value.”

All in all, Pajjuri rates Intel shares a Market Perform (i.e., Neutral) rating, while taking his price target off the table.

The Street is mostly in agreement here. INTC stock claims a Hold consensus rating, based on a mix of 26 Holds, 6 Sells and 1 lone Buy. That said, most seem to think the shares are now undervalued; at $26.09, the average target represents one-year upside of 33%. That upside, however, doesn’t justify the risk in the eyes of the analysts. (See Intel stock forecast)

Micron Technology

The next stock on Raymond James’ radar is Micron, a leading global player in memory and storage solutions, specializing in dynamic random-access memory (DRAM), NAND flash memory, and solid-state drives (SSD). As a key name in the semiconductor industry, Micron supplies critical components for a wide range of applications, from consumer electronics and smartphones to data centers and automotive systems. The company’s innovations enable faster data processing, efficient storage, and overall improved performance in modern tech.

Micron is well-positioned to benefit from the rapid growth of AI due to the increasing demand for high-performance memory and storage solutions. For instance, its HBM3 (high bandwidth memory) is designed to meet the high-speed, high-capacity demands of AI workloads, particularly in advanced applications like machine learning and neural networks, where vast amounts of data need to be processed simultaneously. This key tech positions the company to gain significant traction in the AI market.

The growth on tap at Micron is easy to see when looking at its third quarter of fiscal 2024 report (May quarter). Revenue climbed by an impressive 81.6% compared to the year-ago period, landing at $6.81 billion while also trumping Street expectations by $140 million. At the other end of the equation, adj. EPS of $0.62 beat the analysts’ forecast by $0.09.

Assessing Micron’s prospects, Raymond James’ Pajjuri highlights the company’s HBM as a key element moving forward.

“Data Center demand remains strong driven by HBM while on-device AI is driving strong content growth in Smartphones,” the analyst said. “Industry supply growth remains disciplined as recent capex increases are primarily targeted for HBM and clean room space, giving managements added flexibility in case of a demand slowdown. Micron appears firmly on track to achieve its HBM targets, and we expect ongoing yield improvement to remain a tailwind to margins. We continue to see $11-12 peak EPS power ($2+ from HBM) and believe a higher peak multiple is justified given the secular growth from HBM,” Pajjuri opined.

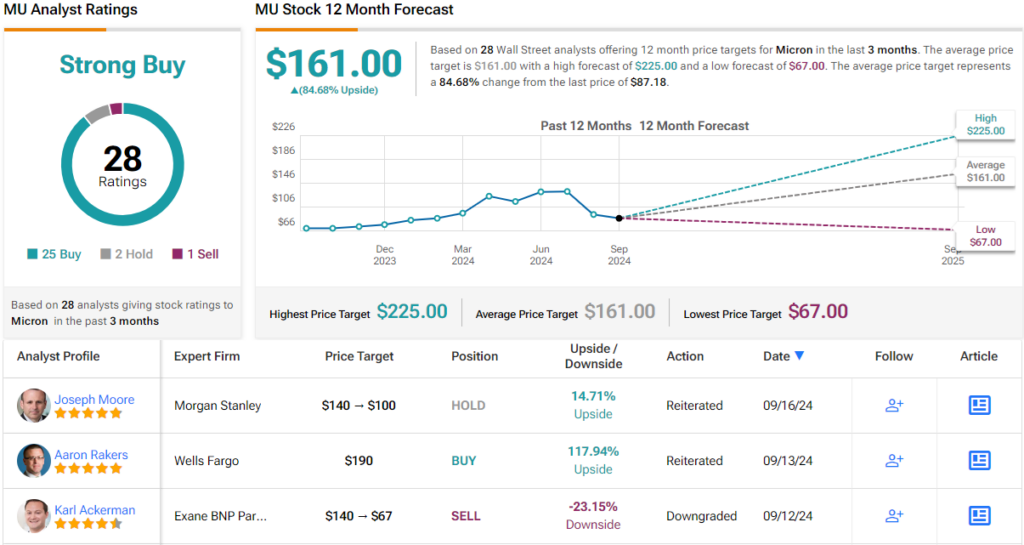

These comments underpin Pajjuri’s Outperform (i.e., Buy) rating on MU, while his $125 price target factors in one-year returns of 43%. (To watch Pajjuri’s track record, click here)

Most of Pajjuri’s colleagues are on the same page here. With an additional 24 Buys vs. 2 Holds and 1 Sell, the analyst consensus rates Micron stock a Strong Buy. The average price target is more bullish than Pajjuri will allow; at $161, the figure suggests shares will climb ~85% higher over the coming months. (See Micron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.