AT&T (T) is an American telecom and media company based in Texas. It provides wireline and wireless phone and internet access services. Its media unit WarnerMedia produces and distributes films, television shows, gaming content, and more.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

For Q4 2021, AT&T reported a 10.4% year-over-year decline in revenue to $41 billion but still modestly exceeded the consensus estimate of $40.7 billion. It posted adjusted EPS of $0.78, which rose from $0.75 in the same quarter the previous year and beat the consensus estimate of $0.76.

AT&T has decided to spin off its WarnerMedia unit in a transaction expected to generate $43 billion. WarnerMedia will merge with Discovery (DISCA) to form a new public company known as Warner Bros. Discovery (WBD). AT&T shareholders are expected to own 71% of WBD while existing Discovery shareholders would control 29% of the business.

With this in mind, we used TipRanks to take a look at the newly added risk factors for AT&T.

Risk Factors

According to the new TipRanks Risk Factors tool, AT&T’s top risk categories are Finance and Corporate, Tech and Innovation, and Legal and Regulatory, each containing 6 of the total 26 risks identified for the stock. Macro and Political and Production are the next two major risk categories with 5 and 2 risks, respectively. AT&T has recently updated its profile with 8 new risk factors across the various categories.

Although AT&T expects to close the WarnerMedia transaction in Q2 2022, it cautions that the deal still requires certain approvals before it can be completed. But even if the transaction is completed, the company cautions that it may not achieve the anticipated benefits.

For example, it explains that there are events that could trigger a significant increase in the tax liability related to the transaction. The company warns that failure to achieve the expected benefits of the transaction could adversely affect its revenue, expenses, and operating results.

AT&T tells investors in another newly added risk factor that it has experienced cost pressures and cautions that the problem may continue. It explains that the costs of the devices it sells and the components that go into its network have been rising. Furthermore, labor expenses have gone up. The company says that while it may attempt to offset the cost pressures by raising the prices of its products and services, such actions may not be successful. For example, customers may stop purchasing its products or services, resulting in revenue loss.

In another newly added risk factor, AT&T cautions that the effects of climate change, such as extreme weather events, could damage its network infrastructure and disrupt its operations. It also warns that regulatory measures in response to climate change could increase its operating costs and adversely affect its business.

Analysts’ Take

Morgan Stanley analyst Simon Flannery recently reiterated a Buy rating on AT&T stock with a price target of $28, which suggests 17.85% upside potential. The analyst commented that AT&T would consider share repurchases once its debt drops to a certain level.

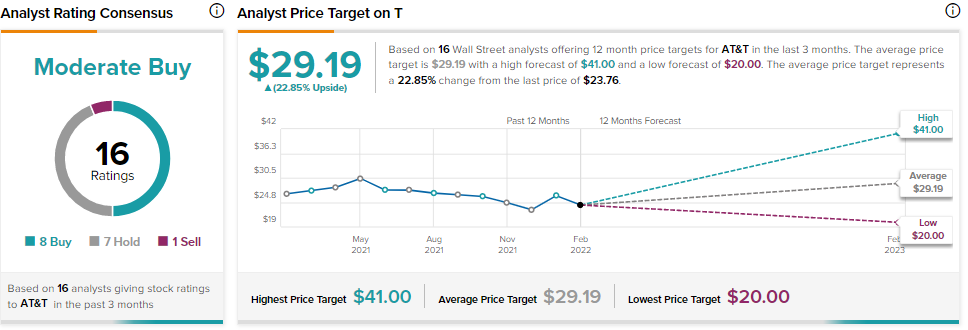

Consensus among analysts is a Moderate Buy based on 8 Buys, 7 Holds, and 1 Sell. The average AT&T price target of $29.19 implies 22.85% upside potential to current levels.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure

Related News:

BMO Enters Financing Agreement with Seaspan

O’Reilly Automotive Could Benefit from Inflation

Dye & Durham Partners with Software Provider NexOne