Hydrofarm Holdings Group (HYFM) has agreed to acquire Aurora innovations for $161 million. The acquisition is likely to close in July. Shares of the company spiked 4.3% in Thursday’s extended trading session after closing nearly 4.5% lower on the day.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Hydrofarm manufactures and distributes hydroponics equipment and supplies for controlled environment agriculture (CEA), while Oregon-based Aurora manufactures and supplies organic hydroponic products.

Hydrofarm will be adding Aurora’s brands such as Roots Organics, Soul soil, and Procision to its portfolio of branded products. Additionally, the company will benefit from new domestic production and distribution capabilities on the east and west coast, along with a peat moss harvesting facility in Canada.

Hydrofarm Chairman and CEO Bill Toler said, “We are pleased to welcome Aurora into our portfolio of quality brands, as our momentum continues to build on the acquisitions front. Aurora has blazed trails for earth-friendly growers, and their Roots Organics line is very popular – a standout for its focus on microbe stimulants.” (See Hydrofarm Capital stock chart on TipRanks)

Hydrofarm is strategically looking to add high-growth businesses with strong margin profiles and in-house brands to its operations. Therefore, the acquisition of Aurora builds on the company’s other acquisitions of hydroponic nutrient brands such as HEAVY 16, House & Garden, and Mad Farmer.

For the calendar year 2021, Aurora is expected to generate net sales of $60 million.

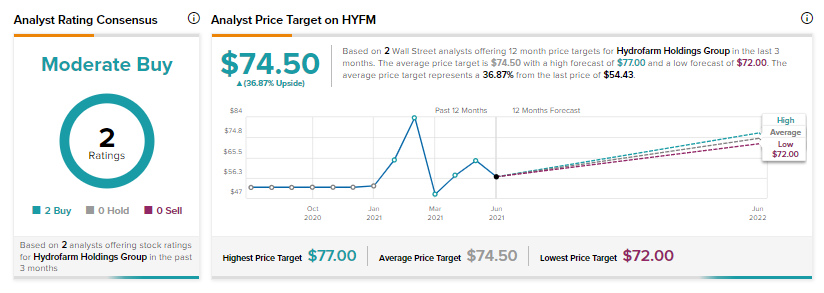

Stifel Nicolaus analyst W. Andrew Carter has reiterated a Buy rating on the stock but increased the price target to $72 (32.3 upside potential) from $70.

During Hydrofarm’s recent Q1 earnings call, Carter asked for more color on the company’s weak margin outlook for 2021.

To this, John Lindeman, Hydrofarm’s CFO answered that as the full impact of the commodity cost cycle is yet to be seen, the company is taking steps to lock costs such as freight costs for the rest of 2021, but there may be other rising costs as well. In light of the cost environment, Lindeman noted that the company issued appropriate guidance.

The other analyst covering the stock, Deutsche Bank’s Kevin Marek also has a Buy rating on the stock but has lowered the price target to $77 (41.5% upside potential) from $88.

The two ratings add up to a Moderate Buy consensus rating. The HYFM average analyst price target of $74.50 implies 36.9% upside potential.

Related News:

Clean Energy Reveals Plans to Develop Natural Gas From Dairies; Shares Roar

Bentley Systems Snaps Up SPIDA to Accelerate its Grid Resilience

Bank of America Expands Financial Centers in Kentucky