Shares of Hut 8 Mining, a cryptocurrency mining company, fell more than 10% in early trading on Monday after the company announced it has finalized a power purchase agreement with Validus Power to support Hut 8 operations in Alberta.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

As part of the agreement, Hut 8 (HUT) can secure up to 100 MW of new project power initially on the basis of physical off-take at very competitive prices. The deal includes an option to expand Hut 8 Mining’s operations if the company decides to move beyond the first 100 MW. The launch date for the planned commercial operation of an initial 35 MW is the start of the fourth quarter of 2021.

Hut 8 Mining’s CEO Jaime Leverton said, “We are thrilled to have the opportunity to announce this cutting-edge power expansion project. This project is key to Hut 8’s Mining strategy of being a leader in procuring cost effective power and advancing innovative mining practices.”

Meanwhile, Validus Power’s President and CEO Todd Shortt noted, “We are seeing the convergence of bitcoin adoption and energy grow at a rapid pace which is creating demand for power that is generated efficiently, delivered faster, and with the environment as a priority. Our commitment to innovation and efficiency, enables us to provide highly scalable and competitively priced power.”

Some of the project’s power will be generated from captured waste gas and converted into electricity by leveraging advanced mobile power plant solutions provided by Validus Power. (See Hut 8 Mining stock analysis on TipRanks)

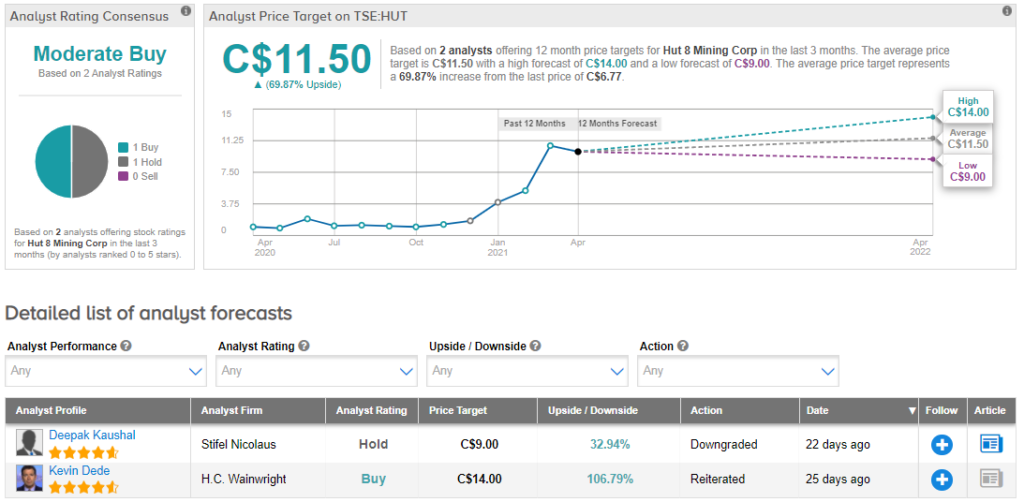

Three weeks ago, Stifel Nicolaus analyst Deepak Kaushal downgraded the stock to Hold from Buy. Additionally, he increased his price target to C$9.00 from C$2.50 (33% upside potential).

Kaushal told investors that while he’s “impressed” with new CEO Jaime Leverton and expects continued innovation and capital discipline, he thinks mining margins may have peaked for the current bitcoin halving cycle and that Hut 8’s “current roadmap is priced in.”

Overall, Hut 8 Mining stock scores a Moderate Buy consensus rating based on 1 Buy and 1 Hold. The average analyst price target of C$11.50 implies upside potential of about 70% to current levels.

Related News:

CareRx To Acquire The LTC Pharmacy Division Of Medical Pharmacies; Shares Pop 9%

Franco-Nevada Publishes 2021 Asset Handbook And ESG Report

Aphria Shareholders Approve Tilray Merger