Humana (HUM) has agreed to acquire One Homecare Solutions (onehome) from its private equity owner WayPoint Capital Partners. It did not disclose financial details of the deal but expects to complete the acquisition in the second quarter of 2021, subject to regulatory approvals.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Onehome provides home-based health services, pioneering a value-based model in Texas and Florida. It is also a care and risk manager. It offers infusion care, nursing, and durable medical equipment services. Launched in 2013, Onehome serves more than a million health plan members across the U.S., including Humana members since 2015.

Humana counts on onehome to expand its value-based home care offering. It said that the deal for onehome aligns with its recent announcement to acquire Kindred at Home. The need for home-based patient care has increased during the COVID-19 pandemic, according to onehome, which says it shares Humana’s mission of bringing healing home.

“We are proud of the longstanding partnership between onehome and Humana, and their shared vision to offer value-based care in the home,” said WayPoint’s Philip Edmunds.

“We believe we can create a transformational value-based offering to serve more people, including non-Humana plan members, nationwide,” said Susan Diamond, Humana’s interim CFO and segment president for Home Business.

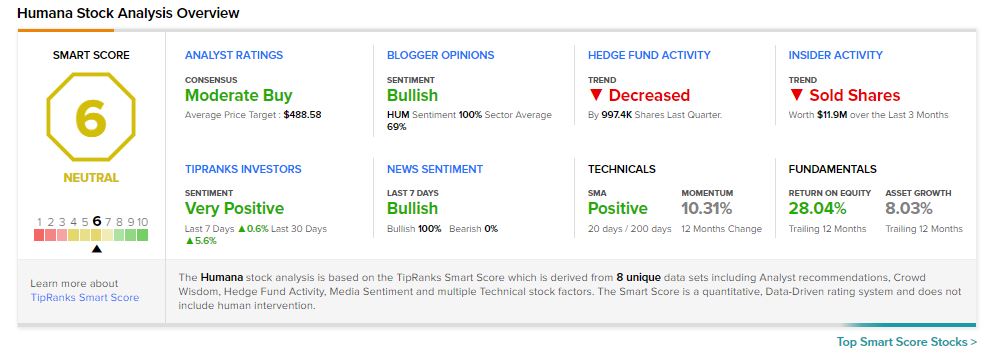

Humana does not expect the pending Onehome acquisition to materially impact its 2021 earnings. (See Humana stock analysis on TipRanks)

Wells Fargo analyst Steve Baxter initiated coverage on Humana stock with a Hold rating and a price target of $472. Baxter’s price target implies 13.7% upside potential.

The analyst observed that Humana has the greatest exposure to Medicare Advantage’s most attractive end market. However, competition could cause its enrollment growth to lag the market.

“HUM is clearly a strong company in good markets, but from a stock perspective we see better risk/reward elsewhere,” noted Baxter.

Consensus among analysts is a Moderate Buy based on 8 Buys and 4 Holds. The Humana average analyst price target of $488.58 implies 17.7% upside potential to current levels.

HUM scores a 6 out of 10 on TipRanks’ Smart Score rating system, suggesting that the stock is likely to perform in line with market averages.

Neha’s News:

Starbucks Applies for Stadium Naming Rights – Report

Tesla’s German Gigafactory Project Faces Resistance – Report

Amazon Prime Video to Stream France’s Ligue 1 Soccer Games