“Decimated” is one of those phrases that sounds like something bigger than it actually is. What it really means is to lose one in 10 of something. And that’s just what happened to cloud marketing stock HubSpot (NYSE:HUBS) in Thursday’s trading, down 10% at one point thanks to—or rather in spite of—its earnings report.

HubSpot’s earnings report was not what anyone would call bad news. Earnings per share (EPS) came in at $1.34, well ahead of analyst consensus calling for $0.99. Revenue, meanwhile, not only beat consensus, it also beat history. It came in at $529.1 million, ahead of analyst consensus of $504.4 million, but also beating revenue from this time last year by 25.5%. Customer count was on the rise, up 23% from June 30, 2022’s figures, and average subscription revenue was up slightly, at an extra 2% over 2022’s second quarter.

So perhaps the problem was in projections. That’s hard to see; HubSpot looks for third quarter revenue between $532 million and $534 million. Analyst projections expected $526.65 million, a likely beat in the making. Earnings per share, meanwhile, is projected between $1.22 and $1.24, again killing analyst projections of $1.14. About the only thing left is the fact that HubSpot is a cloud marketing company, and marketing is likely to be soft in the near-term future thanks to multiple strikes strangling content and consumer confidence on the decline.

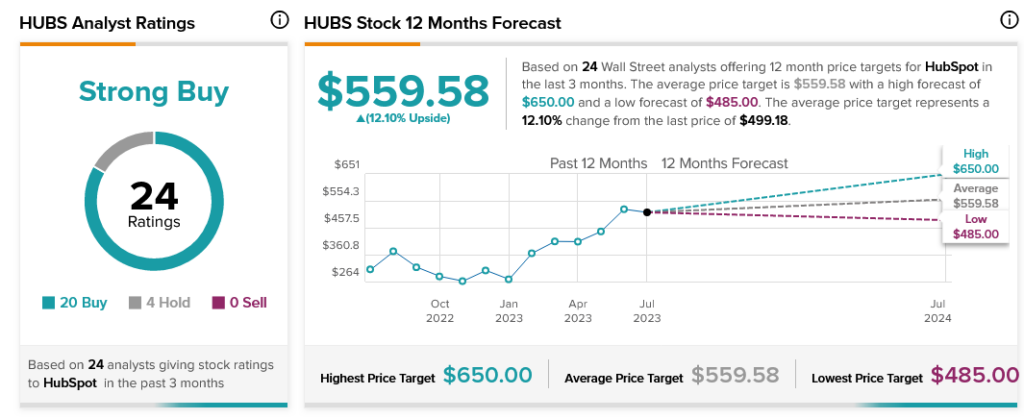

Regardless, analysts are pretty much all in on HubSpot. Currently, HubSpot is a Strong Buy, supported by 20 Buy ratings and just four Hold. Further, with an average price target of $559.58, HubSpot currently offers investors a 12.1% upside potential.