Hewlett Packard Enterprise’s (NYSE:HPE) proposed acquisition of networking product maker Juniper Networks (NYSE:JNPR) is under regulatory review. The U.K.’s competition regulator is investigating whether the transaction will lead to competition issues.

HPE announced the acquisition of Juniper Networks in January 2024. The all-cash deal valued Juniper at approximately $14 billion. The Competition and Markets Authority (CMA) must decide by August 14 whether to conduct a deeper investigation into the acquisition.

Importance of Juniper Deal for HPE

The deal is strategically important for HPE. It will shift HPE’s business portfolio towards higher-growth, higher-margin sectors and significantly enhance its free cash flow potential. Further, the business combination will enable HPE to boost shareholder returns and invest aggressively in growth areas such as artificial intelligence (AI).

HPE anticipates that the acquisition will double its networking business. Further, networking will become a core component and architectural foundation for HPE’s Hybrid Cloud and AI solutions.

Also, the deal will be accretive to HPE’s earnings, accelerating its long-term revenue growth and expanding its gross and operating margins.

Is HPE Stock a Good Buy?

The acquisition’s completion is subject to regulatory approval. Meanwhile, HPE expects the deal to close by late 2024 or early 2025. The acquisition is poised to reshape HPE’s business landscape and accelerate its growth. Thus, any negative development could hurt its share price.

HPE stock has risen over 30% year-to-date, reflecting solid demand for its AI systems. However, the heightened competitive environment keeps Wall Street sidelined on HPE stock.

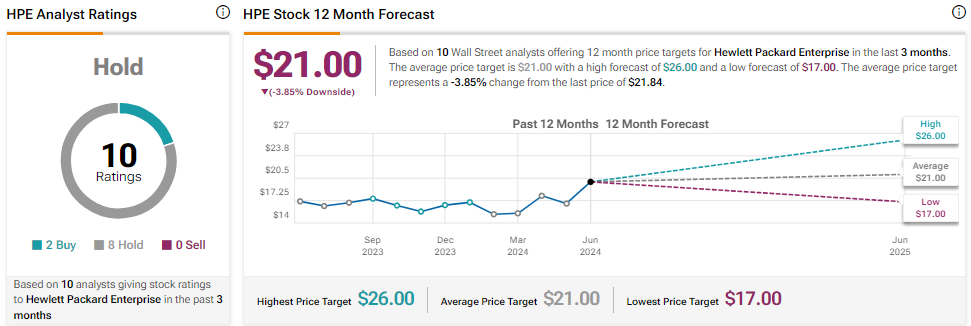

With two Buys and eight Hold recommendations, HPE stock has a Hold consensus rating. The analysts’ average HPE stock price target is $21, implying 3.85% downside potential from current levels.

Questions or Comments about the article? Write to editor@tipranks.com