Honeywell (HON) announced on Monday that it is considering the potential separation of its Aerospace business. The industrial conglomerate stated that this is part of an evaluation of its comprehensive business portfolio undertaken this year by its Chairman and CEO, Vimal Kapur.

HON Could Be Exploring a Breakup Driven by Elliott

The company’s exploration of this alternative may have been influenced by activist investor Elliott Investment Management. Elliott holds a $5 billion stake in the company and has been urging Honeywell to pursue a breakup to unlock value in its aerospace and automation segments.

Furthermore, the company’s board stated that it has made “significant progress” in reviewing strategic alternatives and plans to share updates with its Q4 results.

In response, Elliott welcomed the decision, stating, “We believe the portfolio transformation Vimal and his team are leading represents the right course for Honeywell, and we look forward to the upcoming completion of the review and to supporting Honeywell as it implements the necessary steps to realize its full value.”

HON’s Aerospace Is Its Largest Segment

Honeywell’s aerospace unit is the company’s largest segment and serves major clients like Boeing (BA) and Airbus (EADSY). This business reported revenues of $13.62 billion in FY23, with 46% of these revenues coming from commercial repairs and spare parts. While rising jet production has bolstered the business, supply chain disruptions have posed challenges.

In the third quarter, this business accounted for more than 35% of the company’s total revenues.

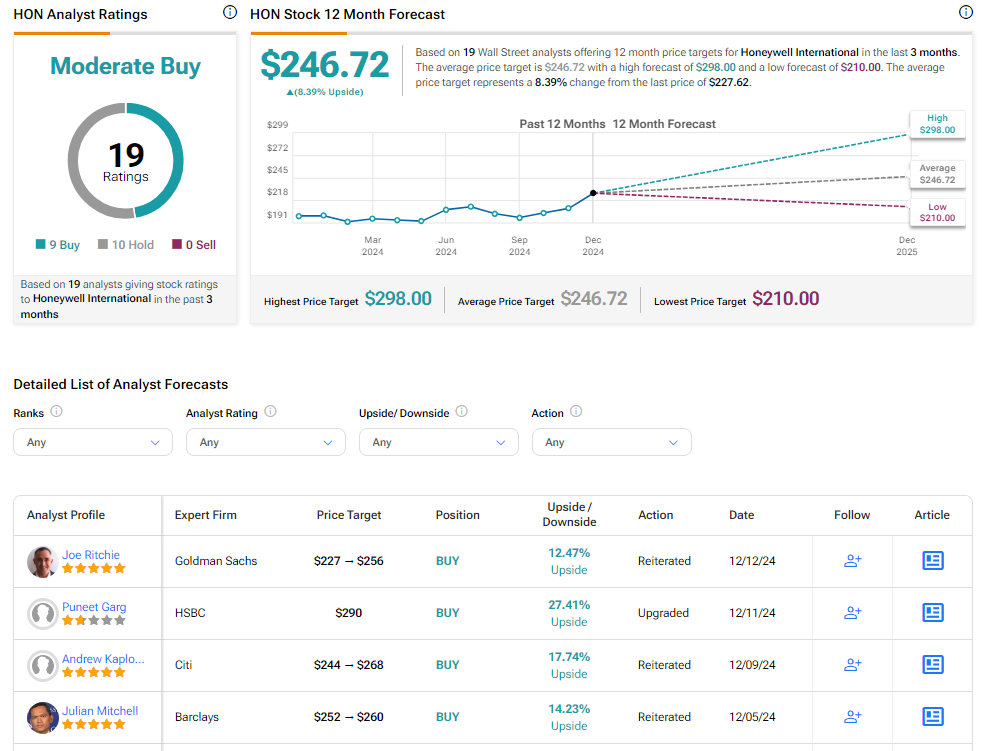

Is HON a Good Stock to Buy?

Analysts remain cautiously optimistic about HON stock, with a Moderate Buy consensus rating based on nine Buys and 10 Holds. Over the past year, HON has increased by more than 10%, and the average HON price target of $246.72 implies an upside potential of 8.4% from current levels.