Nio (NYSE:NIO) had an early start in the EV game, and its status as one of the first pure NEV (new energy vehicle) players in China ensured brand recognition for its premium segment offerings.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Additionally, being a pure BEV (battery electric vehicle) rather than PHEV (plug-in hybrid electric vehicles), compared to peers, Nio has the highest battery installation size, positioning it to benefit from the ongoing decline in battery prices.

These are both strong points made by Goldman Sachs analyst Tina Hou when assessing Nio’s prospects. However, they are countered by other, less appealing developments.

Despite its early mover advantage, Nio has been losing market share in China’s NEV market, its take falling from 3.9%/3.1% in 2020/2021 to 1.9% in November 2023. That has also been the case specifically in the >Rmb300k NEV segment, with its share dropping from 37%/33% to 15%.

“While we see early mover advantages, growth momentum could remain soft on relatively fewer new model launches given its mature product portfolio vs. Peers,” Hou said on the matter.

Primarily driven by 40% volume growth, Hou forecasts revenue growing at a CAGR (compound annual growth rate) of 31% between 2023E-2025E but her 2024E-2025E volume expectation growth is 11%-14% below Visible Alpha consensus as the analyst thinks the Street’s implied monthly sales volume of 7.8k per model for its Alps sub-brand in 2025E, is too high compared to 1.8k for its existing models.

“As Nio has a more comprehensive product portfolio (8 models) vs. peers, we expect a relatively softer new model pipeline over the next 2 years with 1 for the Nio main brand (ET9) and 2 for its Alps sub-brand,” Hou went on to add.

That is not the only issue. During 2018-2023, Nio amassed Rmb46 billion in negative FCF and Hou expects the company to remain FCF-negative until 2026E, suggesting an additional Rmb16 billion in cash burn during 2024E-25E. Following a December 2023 US$2.2 billion equity investment made by CYVN, Hou reckons Nio should show Rmb17 billion in net cash by the end of 2023. That should be enough to support its operations, ongoing R&D, and brand development. “From 2026E onward,” Hou added, “we expect positive FCF generation gradually helping to relieve Nio’s funding pressure.”

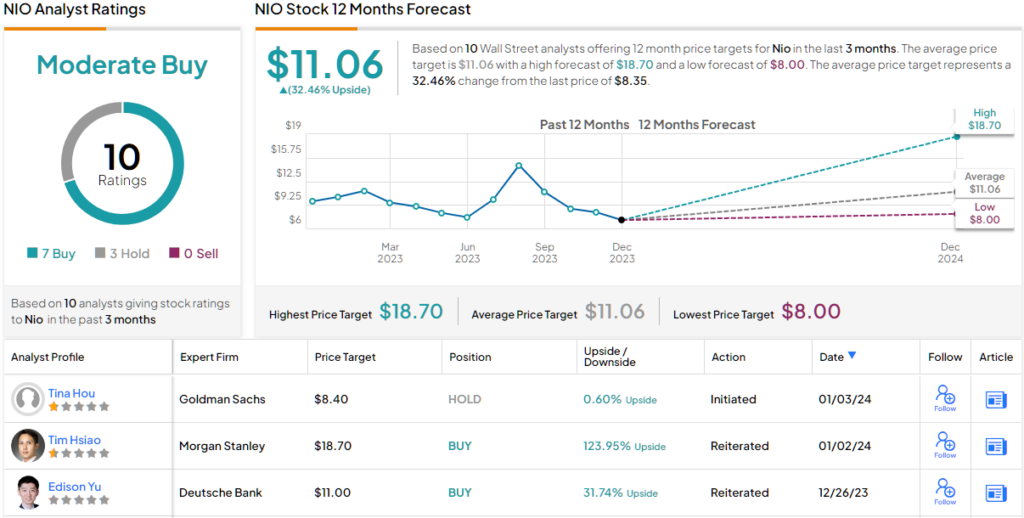

So, what does all the above ultimately mean for investors? Hou initiated coverage of NIO with a Neutral rating and a price target of $8.40, suggesting the shares are currently fully valued. (To watch Hou’s track record, click here)

Hou, however, is amongst a minority on Wall Street. Over the past 3 months, 10 analysts have waded in with NIO reviews and these break down into 7 Buys and 3 Holds, all culminating in a Moderate Buy consensus rating. Most think the shares are somewhat undervalued; Going by the $11.06 average target, a year from now, the stock will deliver returns of 32%. (See Nio stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.