Rivian (NASDAQ:RIVN) has been getting plenty of praise for its vehicles from both consumers and reviewers, yet that hasn’t translated into stock performance. Rivian shares have shed 56% year-to-date, as strong reviews haven’t been enough to boost the company’s underwhelming sales volumes.

The Q3 deliveries reached 10,000 units, some distance below the Street’s expectation of 13,000 units. The company also produced just 13,200 units and lowered its production guide for the year from ~57,000 to 47-49,000 units, laying the blame on a shortage of a component used for both the R1 and EDV/RCV.

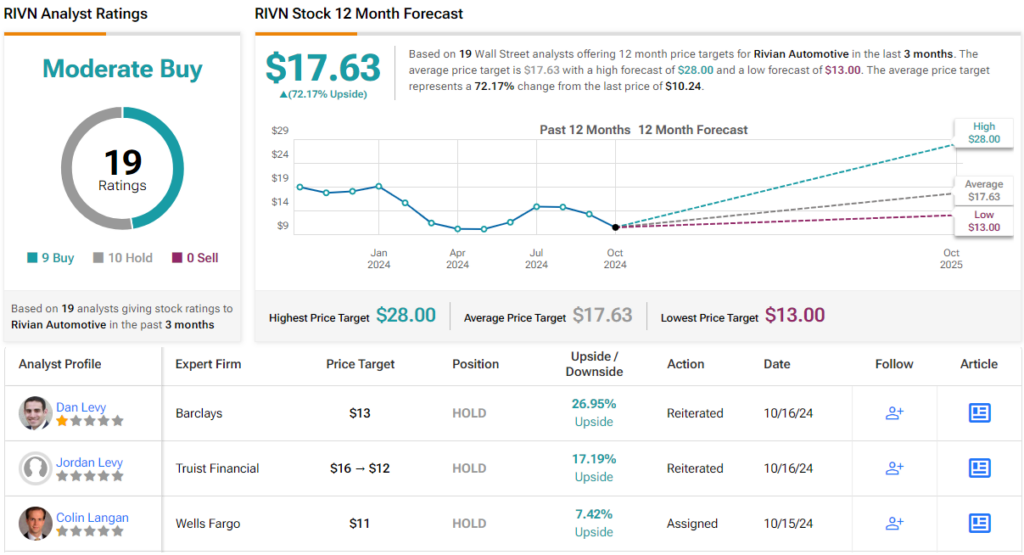

When taken alongside the production cut, Barclays analyst Dan Levy says the delivery result was “particularly disappointing.”

The EV maker, however, did reiterate its intention to deliver the same number of vehicles as expected previously (50.5-52k units), but given the unfavorable seasonality of Amazon van deliveries, Levy notes that a step up in Q4 volumes will be needed for the company to hit that target. “Moreover,” the analyst goes on to say, “we’d suspect that the production guide cut was at least in part attributable to inventory management, an indication of potentially softer-than-hoped R1 demand post-refresh.”

As a result, Levy anticipates deliveries in 2024 will trend towards the lower end of the expected range, also believing forecasts for 2025 will be “tamped down by the reduced exit rates.”

The other big problem for RIVN has been the fact it is losing money on every car it sells. The company has targeted Q4 as the period when it expects to become gross profit positive. While Levy thinks it’s possible the company will reiterate this objective on the Q3 earnings call, given the lower-than-expected volumes and factoring in “indications of softer-than-hoped demand,” the analyst now thinks the company will slightly miss hitting the target.

“We appreciate reg credit recognition and LCNRV (lower of cost and net realizable value), could potentially still enable this target to be met, but we suspect most investors will scrutinize a result driven by these factors,” Levy summed up.

Bottom line, Levy rates RIVN shares an Equal Weight (i.e., Neutral), and lowered his price target from $16 to $13. Nevertheless, the new figure still suggests shares will climb 28% higher over the coming months. (To watch Levy’s track record, click here)

The broader analyst community remains divided, with 9 Buy ratings and 10 Holds, leading to a Moderate Buy consensus. The average price target of $17.63 indicates a more optimistic potential one-year return of 72%. (See Rivian stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com