Tesla (NASDAQ:TSLA) is a story that has always hinged on being much more than an automaker, and this narrative is only set to grow stronger over time.

These days, the EV leader has other priorities – something Oppenheimer analyst Colin Rusch believes the company will emphasize during its upcoming Q4 earnings call, scheduled for this Wednesday (Jan 29).

“We anticipate TSLA to continue focusing resources and its narrative on Physical AI technology leadership while further moderating vehicle sales growth expectations in 2025 under the guise of preparation for Model 2 and autonomous vehicle introduction,” notes Rusch who ranks amongst the top 1% of Wall Street stock pros.

The 5-star analyst’s projections for 2025 include 9% unit growth, rising to 12% in 2026. However, these estimates carry potential downside risk if the Model 2 captures market share from lower-end Model 3 configurations. Rusch also expects the company to reiterate its intention to start production of the Model 2 in 2H25.

Beyond vehicles, Tesla is likely to continue emphasizing the “strong demand and margin strength” of its stationary storage projects. Rusch foresees the impact of new Chinese battery import tariffs but predicts Tesla will mitigate the effects by passing most of the costs onto customers and collaborating with non-Chinese suppliers to “supplement supply and leverage its purchasing power into a cost advantage.”

That kind of stuff, however, has been taking a backseat to the Tesla narrative recently, given Musk’s relationship with Trump and his position in the new administration. That is a bit of a risky game, however, with Rusch viewing the Trump/Musk relationship as a “key variable for shares.”

The analyst expects Musk will bring attention to his influence on the US political landscape, but there’s still considerable risk to the relationship between Trump and Musk, which could potentially threaten Tesla’s advantage from it.

“We anticipate a challenging budget fight for Trump’s tax cuts and view DOGE-related savings as essential in financing those cuts,” Rusch opined. “We see DOGE’s success as the first test of Trump/ Musk’s relationship and precursor to Trump supporting TSLA’s regulatory agenda.”

As for the financials, Rusch has now lowered most of his estimates to account for slowing demand in the US and EU. The analyst’s respective FY24E delivery, revenue, and adjusted EPS forecasts now stand at 1.79 million, $99.5 billion, and $2.52 (previously 1.81 million, $100.3 billion, and $2.52). For FY25, Rusch’s respective delivery, revenue, and adjusted EPS forecasts are now 1.95 million, $111.6 billion, and $3.08 (previously 2.20 million, $123.6 billion, and $3.51).

“We remain cautious on TSLA’s underlying fundamentals and relative autonomous technology position,” Rusch summed up. Consequently, the analyst assigns a Perform (i.e., Neutral) rating to Tesla shares, without suggesting a price target. (To watch Rusch’s track record, click here)

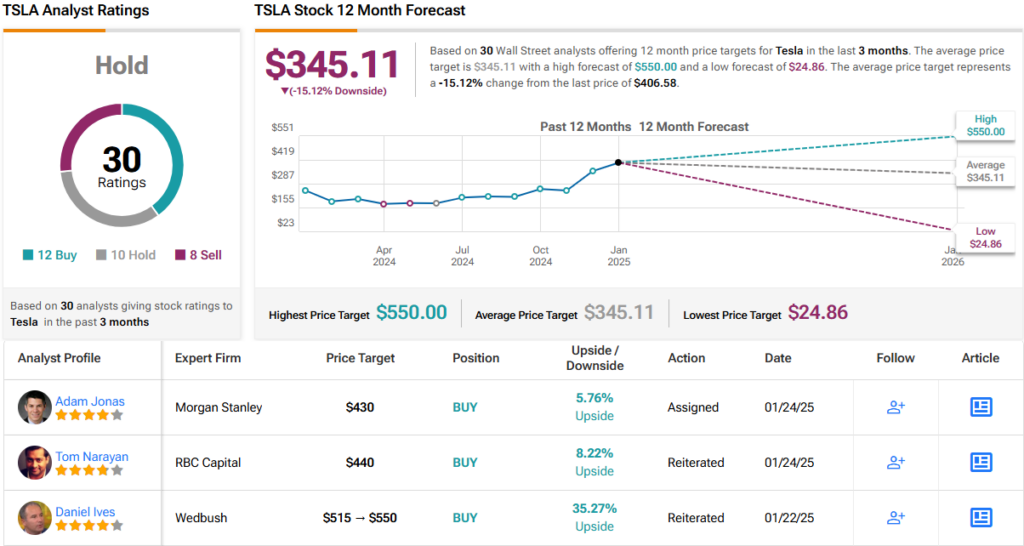

Other analysts do have targets, with the Street’s average landing at $345.11 – indicating a potential 15% downside. As for ratings, Tesla holds a Hold consensus rating, derived from a mix of 13 Buys, 12 Holds, and 9 Sells. (See TSLA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.