China is the world’s largest automotive market, and its car industry is shaking up the US car industry with significant force.

Don't Miss Our New Year's Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

That’s the thesis behind a new note from Morgan Stanley analyst Adam Jonas. The automotive expert points out that China is producing far more vehicles than its domestic market requires and, in 2023, overtook Japan as the world’s largest vehicle exporter. In 2024, China has continued to widen this lead. Moreover, China dominates the electric vehicle (EV) market, outcompeting US manufacturers not just in volume but by offering lower prices.

This bodes ill for US automotive companies, both the Detroit stalwarts and the EV companies. Jonas advises investors to exercise caution, particularly recommending a ‘hold off’ on buying shares of Rivian (NASDAQ:RIVN) and Ford Motor (NYSE:F).

But is the rest of Wall Street as cautious as Jonas? We’ve turned to the TipRanks database to investigate further. Let’s dive in.

Rivian

We’ll start with Rivian, an EV company in the American market notable for having survived its development years – the pre-production period when costs are high, designs are not ready for prime time, and investors can expect quarterly losses – to enter the production stage of its business.

Rivian has been in business since 2009 and began making production deliveries of its fully electric R1T pickup truck in 2021. While a year behind schedule, this still made Rivian the first US company to put an all-electric pickup into the consumer market. Today, the company has two models, the R1T and the R1S, in production, with the R2 and R3 models under development. The R2, the next scheduled for production, is expected to launch in 2026.

Each of these models is based on a common chassis, a feature that Rivian has described as its ‘skateboard.’ The chassis is a four-wheeled platform, designed to fit multiple vehicle configurations, with varying body styles, seating arrangements, battery packs, and motor types, all tending toward a built-in maximum flexibility. Each wheel features its own electric motor, a feature that allows for weight savings by avoiding a large and complex common drivetrain.

Rivian has not limited its innovation to hardware. The company has made Driver+, its driver assistance and vehicle autonomy platform, standard on all of its Gen 2 vehicles. The system is designed to assist and back up drivers, rather than replacing them. Features include highway assistance, lane change assistance, and adaptive cruise control. Rivian’s assistance platform can help the driver brake the vehicle, detect potential oncoming threats, and adjust lighting to best meet the driving conditions. Parking and reverse warnings and assistance are also included.

Development of this technology, at a mass production level, does not come cheap – but Rivian has deep pockets. The company finished Q2 this year, the last reported, with more than $7.8 billion in cash and other liquid assets, and in June of this year announced an agreement to enter a joint venture (JV) partnership with Volkswagen. The JV will focus on developing vehicle software for both companies. As part of the agreement, Volkswagen has invested $1 billion in Rivian, and another $4 billion in investments are planned.

The company’s cash position is an important asset, since Rivian has been running net quarterly losses. In 2Q24, the EPS loss came to $1.27 per share, even while the company reported $1.158 billion at the top line. The company is predicting it will turn to profitability in Q4 of this year.

A potential profit in several months was not enough to impress Morgan Stanley’s Adam Jonas, who sees costs piling up for Rivian. In particular, he notes that the autonomy and driver assistance technology will require a high capital investment, and that we just don’t know if the VW joint venture will cover that.

“We downgrade RIVN to EW from OW… The downgrade reflects our incorporation of the capital intensity of AV/ADAS which may be required to fulfill the technological underpinnings that attracted Volkswagen as a JV partner; as such, we increase estimates of annual capex by $200-300mn per year beginning in 2026 (management has provided guidance of $1.2bn and $1.5bn for 2024 and 2025, respectively). We note that Rivian has not yet announced details around JV cost structure,” Jonas noted.

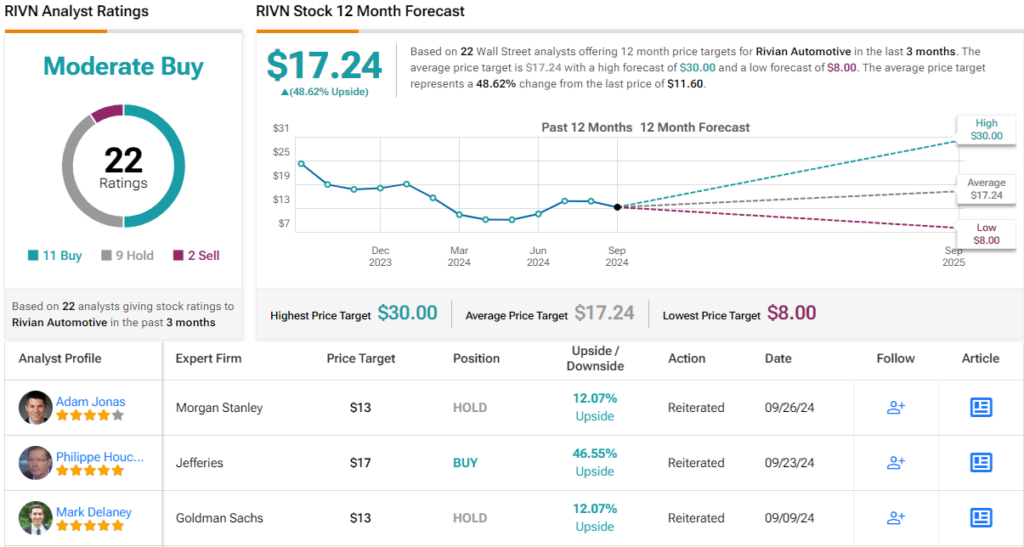

While Jonas has, as noted, downgraded his rating here to Equal Weight (i.e. Hold), his price target of $13 still points to a one-year upside potential of nearly 12%. (To watch Jonas’ track record, click here)

Overall, the consensus view on Rivian is more bullish than the Morgan Stanley view. The stock has a Moderate Buy rating, based on 22 reviews that include 11 Buys, 9 Holds, and 2 Sells. The shares are priced at $11.60 and the $17.24 average target price implies a gain of ~49% in the next 12 months. (See RIVN stock forecast)

Ford Motor

Next up is one of Detroit’s great automakers, Ford Motor. Ford is famous as one of the early leaders in the car industry, and as one of the companies that turned Detroit into the Motor City more than a century ago. Ford has long been known for both technological innovations and for a keen sense of what customers want. On the first, the company introduced the assembly line production technique to the US auto industry; on the second, Ford is maker of such iconic vehicles as the Mustang and the F-series trucks.

The F-series trucks, and to a lesser extent the Mustang, form the core of Ford’s current business. Both lines have proven long-lasting – the F-series was introduced in 1948, and the Mustang in 1964 – and both are profit generators for the company. The F-series trucks, in particular, have proven to be a flexible product line, with light-, medium-, and heavy-duty trucks, featuring plenty of options in cab size, bed size, and engines, and are Ford’s best-selling vehicle line – and one of the best-selling vehicles lines in the entire North American market.

The industry, however, is feeling strong pressures to move toward electric vehicles, and Ford has been developing EV models in response. The company has moved to leverage the popularity of its Mustang and F-series models in this switch, and prominent among its EVs are an electric Mustang and an electric F-150 truck. We should note, however, that American-made EVs still face headwinds from high prices and customer resistance – Ford’s electric vehicles, despite the headlines generated by featuring popular names in the line-up, make up only a small part of the company’s total sales – just 8,944 pure electric and 16,394 hybrid electric vehicles out of 182,985 vehicles of all types sold in the last month. Those EV monthly figures compare poorly to the more than 70,000 F-series trucks sold in August.

EVs run a net loss for Ford, but the company compensates through other segments of its business. In the last quarterly results made public, from 2Q24, Ford reported total revenues of $47.8 billion. Automotive revenue, at $44.81 billion of the total, was up 5.6% year-over-year, but was $70 million below the forecast. Ford remained profitable in the quarter, with a non-GAAP EPS of 47 cents – but that was 21 cents per share less than had been forecast and was down 25 cents per share from the prior-year quarter.

Turning to the Morgan Stanley view, we find that analyst Jonas sees Ford beset by too many headwinds. He is especially worried by the pricing and mix issues in the EVs, and by difficulties with regulatory compliance in the new automotive tech segments.

“We downgrade Ford from OW to EW… Our downgrade to F is underpinned by our expectation for greater share loss through end of decade (lower normalized units), price/mix headwinds, and regulatory compliance/EV/AV/ROW/Other risk which can impact profitability (lower normalized EBIT margin) driving lower normalized earnings and valuation. We reduce Normalized EPS by 15.1%,” Jonas explained.

His downgraded rating of Equal Weight (i.e. Hold) is accompanied by a price target of $12, which points toward a ~11% gain in the year ahead.

The gain that Jonas sees ahead for Ford is just half the Wall Street consensus. The stock is selling for $10.78 and its $13.19 average price target suggests it will appreciate by 22% on the one-year horizon. The shares have a Hold consensus rating, with 15 reviews that break down to 4 Buys, 10 Holds, and 1 Sell. (See Ford stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.