Rivian (NASDAQ:RIVN) investors’ 2025 began with a bang after the EV maker released its 4Q24 delivery haul. Shares got a welcome new year bounce, surging by 24.5% in the subsequent session with Wall Street applauding a better-than-expected readout.

The company made 14,200 deliveries, surpassing the Street’s estimate of 13,400 and rising from Q3’s 10,000 deliveries. Rivian produced 12,700 vehicles in the quarter, exceeding the Street’s forecast of 11,500 but slightly below Q3’s production of 13,200 vehicles.

These results enabled the company to surpass its prior FY24 production guidance of 47,000–49,000 vehicles, reaching 49,500. The firm also met its FY24 delivery guidance of 50,000–52,000, achieving 51,600.

Rivian further disclosed that a supplier issue – a copper wiring timing mismatch affecting its Enduro motors – that disrupted production in the second half of FY24 has now been resolved as the company transitions into the new year. Recall, in Q3, the company revised its 2024 production guidance downward from 57,000 to 47,000–49,000 vehicles, citing supply constraints affecting the R1 and RCV platforms.

RBC analyst Tom Narayan believes the Q4 delivery figures show that the supply issues were limited to Q3. Following the strong delivery haul, with Rivian having set its sights on turning gross profit positive in Q4, Narayan has increased confidence it will be able to do so.

“We do think it likely that Rivian will hit this critical benchmark, in part thanks to $275M in contracted regulatory credit revenues all coming in Q4,” the analyst explained. “This would represent over 70% of the sequential improvement in gross profit to get to breakeven, and leaves $111M of sequential cost improvement necessary to hit this target. The better volumes should alone help given operating leverage.”

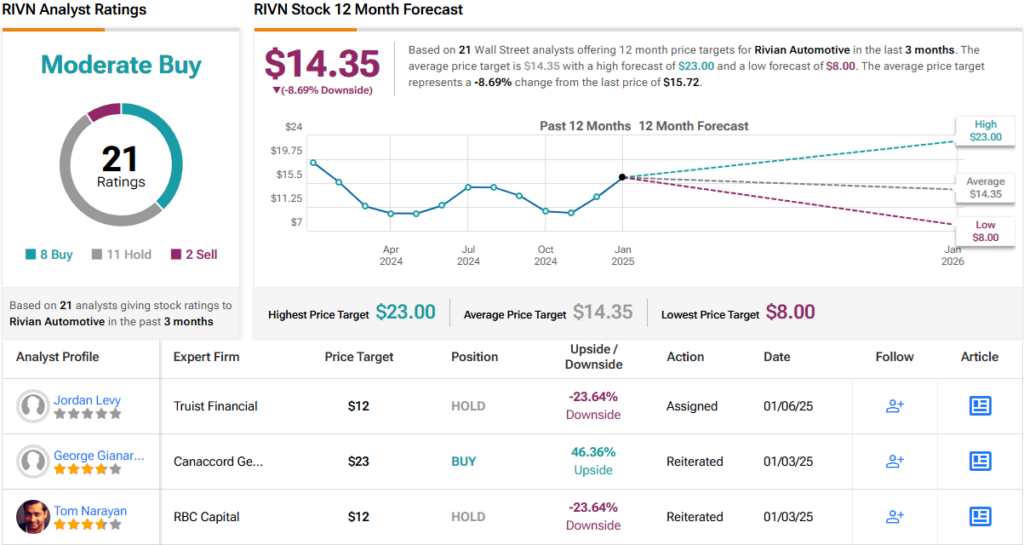

It’s not quite enough, however, for Narayan to turn bullish on Rivian. The analyst remains on the sidelines with a Sector Perform (i.e. Neutral) rating and a $12 price target. That said, Narayan might as well have said Sell, as that figure suggests the stock has overshot by ~24%. (To watch Narayan’s track record, click here)

There is no such conundrum in CFRA analyst Garrett Nelson’s assessment. While Nelson concedes that Q4 volumes exceeded expectations, given the actual amount reported, he remains skeptical Rivian achieved positive gross margins for the quarter. That will only be known when the company reports Q4 earnings on February 20.

Nelson also thinks Rivian’s cash burn rates “remain very concerning.” As such “on cash flow and EV demand-related concerns,” the analyst rates RIVN a Sell, with an $8 price target, suggesting a potential downside of 49% from current levels. (To watch Nelson’s track record, click here)

As for the rest of the Street, based on an additional 8 Buys, 11 Holds, and 1 Sell the analyst consensus rates this stock a Moderate Buy. However, the $14.35 average price target factors in a one-year decline of ~9%. (See Rivian stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.