In a research note on November 9, Needham analyst Matt Dezort reiterated a Buy rating on CyberArk Software (CYBR) stock and boosted the price target to $410 (20.2% upside potential) from $360. What’s more, Needham named CyberArk as its Top Pick for 2025 in the Security market and placed the stock in its Conviction List. After an impressive 54% rally in the stock last year, Dezort sees continued upside potential in 2025 due to several tailwinds, including an accelerating threat environment and a growing customer base.

Needham Remains Upbeat About CyberArk in 2025

Needham’s Dezort believes that CyberArk stock is well-positioned to sustain last year’s momentum due to the following three reasons:

- Optimism about 2025 ARR Outlook: Dezort thinks CYBR’s initial calendar year 2025 ARR (annual recurring revenue) guidance is likely to come in line with or above the consensus estimate of $1.39 billion, reflecting more than 21% year-over-year growth. The consensus ARR estimate includes the impact of the Venafi acquisition but reflects a slight decline in the organic core CyberArk ARR. However, the analyst thinks that such a decline is “unlikely given new logo momentum and durable demand for PAM [Privileged Access Management]/Identity security,” as revealed by Needham’s channel checks. In fact, the analyst sees a slight upside in organic estimates in 2025, with a possibility of beat-and-raise quarters. Dezort thinks at least mid-20% ARR growth is achievable.

- Venafi Synergies: Needham’s checks also indicated that CYBR’s customers and investors were positive about the company’s recent Venafi acquisition. Dezort sees a massive cross-sell opportunity. He expects CyberArk’s large, underpenetrated customer base and extensive channel reach to boost Venafi’s growth toward core-CYBR ARR expansion rates (more than 25%) in calendar years 2026 and 2027, with the improvement expected to begin in the second half of this year.

- Attractive Valuation: The analyst noted that at 12.2x EV/Revenue (Next 12 months estimate), CYBR stock trades almost in line with the peer group’s average multiple of just under 12x. However, based on the Street’s sales growth estimate of 31% for 2025, Dezort contends that at an Enterprise-Value-to-Sales-to-Growth (EV/S/G) of 0.38x, the stock is trading at a more than 20% discount to the comparable group and such a discount in “unwarranted.” He sees an upside to 2025/2026 estimates due to the company’s solid execution.

Overall, Dezort is confident about the continued strength in CyberArk’s performance, driven by the strong demand trends in the PAM and Identity security markets, ARR growth, encouraging multi-product enterprise pipeline, and synergies from the Venafi acquisition.

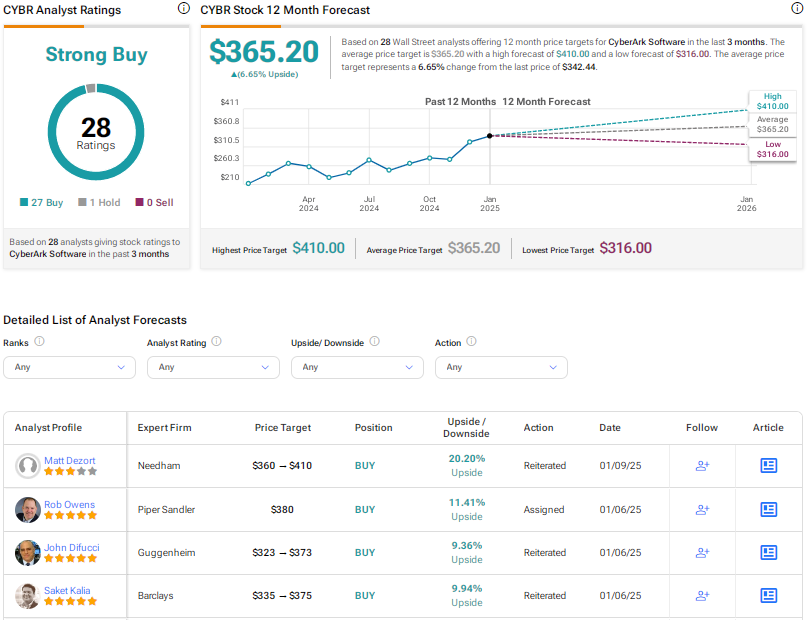

Is CYBR a Good Stock to Buy?

Including Dezort, 27 analysts have a Buy rating on CyberArk Software stock, while only one analyst has a Hold recommendation. Overall, CYBR stock scores a Strong Buy consensus rating. The average CYBR stock price target of $365.20 implies about 7% upside potential.

Questions or Comments about the article? Write to editor@tipranks.com