Cannabinoid prescription medicines stock GW Pharmaceuticals (GWPH) has reported particularly strong first quarter earnings results, with US sales of Epidiolex at $116.1M, up over 215%. This cannabidiol oral solution is approved in the US and Europe for the treatment of seizures associated with Lennox-Gastaut syndrome (LGS) or Dravet syndrome in patients two years of age or older.

First quarter GAAP EPS of -$0.02 beat Street expectations by $0.05, and revenue of $120.6M (up an eye-watering 207.3% year-over-year) beat by $15.5M. GWPH shares popped 9% in after-market trading on Monday, bringing the stock’s year-to-date gain to 4%.

“In the first quarter of 2020, we have seen continued strength of the Epidiolex brand in both the U.S. and Europe and remain confident about prospects for growth in the remainder of the year,” stated Justin Gover, GW’s CEO.

For the second quarter, management noted a “solid” April for US Epidiolex sales and expects flat to modest growth throughout the quarter in the US, due to the current environment. GWPH’s global manufacturing and supply chain is currently uninterrupted by COVID-19.

Looking ahead, GW Pharma has also submitted applications in both the US and Europe to expand the indication for Epidiolex to include seizures associated with Tuberous Sclerosis Complex (TSC), for which it has reported positive Phase 3 data, and is carrying out a Phase 3 trial in Rett syndrome.

“Having been granted priority review by the FDA for our proposed label expansion to include TSC, our US commercial team is actively preparing for the launch of this indication in August” Gover said. The FDA action date is July 31.

“With further potential upside levers in the near-term (launch progress, TSC label expansion) and mid- to long-term (off-label use, Epidiolex IP extension beyond 2027, and pipeline/nabiximols progress), we continue to see a favorable set up for GWPH” cheered JP Morgan’s Cory Kasimov following the results. He has a buy rating on the stock and $187 price target (71% upside potential).

“Near-term label expansion opportunities (Tuberous Sclerosis) and the potential for off-label use in the broader population of general epilepsy patients could contribute significantly to the top line” he continued.

Indeed, GWPH boasts a deep pipeline of additional cannabinoid product candidates, in particular nabiximols, for which it is advancing multiple late-stage clinical programs for the treatment of spasticity and PTSD. It also has additional cannabinoid product candidates in Phase 2 trials for autism and schizophrenia.

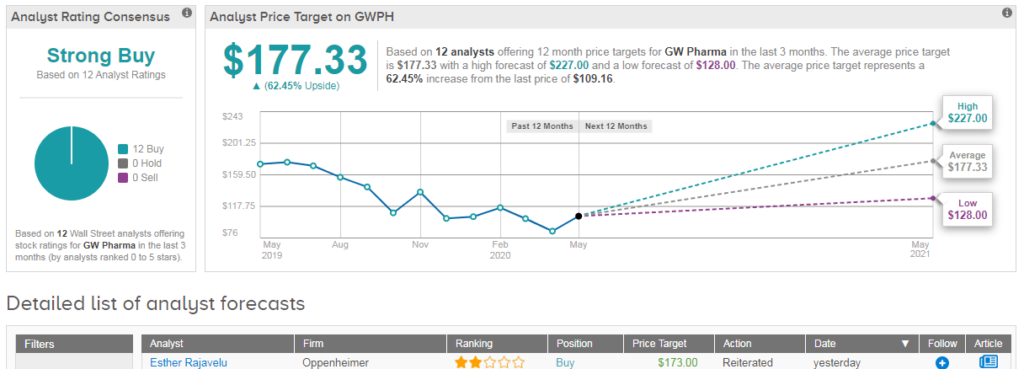

Overall the stock has a firm Strong Buy analyst consensus with 12 recent buy ratings- and no hold or sell ratings. The average analyst price target stands at $177 (62% upside potential). (See GWPH stock analysis on TipRanks).

Related News:

Qantas Said to Halt Plane Deliveries From Boeing, Airbus Amid Travel Freeze

3 Stocks Needham’s Top Analysts Are Raving About

AMC Pops 11% Amid Potential Acquisition Talks by Amazon