Shares of Globe Life (GL) were down 2.5% in pre-market trading on Thursday after the life insurance company reported mixed Q3 results and also lowered its FY2021 and FY2022 guidance.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Adjusted earnings of $1.84 per share lagged analysts’ expectations of $1.93 per share. The company reported earnings of $1.76 per share in the prior-year period.

However, revenues jumped 6.9% year-over-year to $1.28 billion and exceeded consensus estimates of $1.26 billion. The increase in revenues reflected a surge in total life premiums, which increased 8% to $728 million, and health premiums, which increased 4% to $299 million.

On top of this, total health underwriting margins increased by 6% year-over-year, with 11% growth in life underwriting margins at the American Income Life Division and 10% at the Liberty National Division. (See Globe Life stock charts on TipRanks)

On the negative side, the company stated that the COVID-19-related life claims in the third quarter were much higher than expected, mainly due to the Delta variant, which led to much higher infection rates and deaths.

COVID life claims increased massively in the quarter to $3.5 million per 10,000 U.S. deaths, up from an average of $2 million per 10,000 U.S. deaths in prior periods.

The company forecast the level of losses per U.S. death to continue during the fourth quarter and range between $3 million – $4 million per 10,000 U.S. deaths in 2022.

Due to higher-than-anticipated COVID-19 losses, Globe Life lowered its earnings guidance for the year ending December 31, 2021, and 2022. For FY2021, the company forecast net operating income per share to be in the range of $6.85 to $7.05, while the consensus estimate is pegged at $7.27. For FY2022, net operating income per share is likely to range between $7.95 and $8.75.

Ahead of the earnings announcement, Credit Suisse analyst Andrew Kligerman decreased the price target on Globe Life to $130 (32% upside potential) from $135 and reiterated a Buy rating.

Kligerman notes that Globe Life is trading at attractive levels of 11.6x its 12-month forward EPS, lower than its 10-year and 5-year averages of 13x and 13.5x, respectively.

The analyst believes that the valuation discount is “unwarranted” despite the probability of extended COVID-19 mortality. He forecast that heightened mortality rates may not exceed a low single-digit impact on EPS.

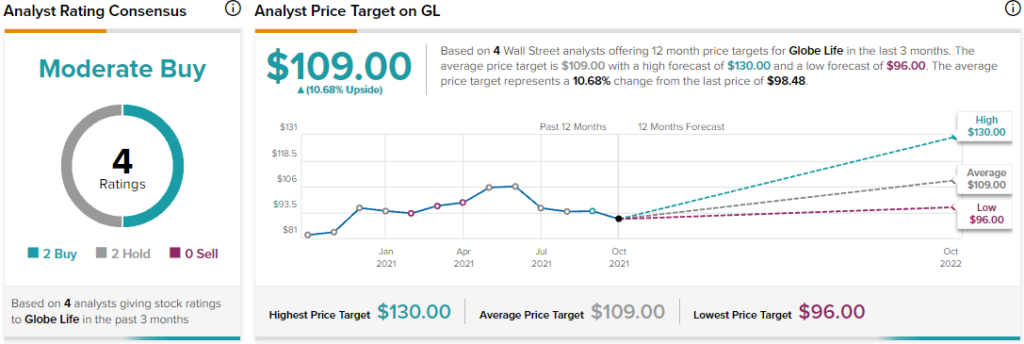

Overall, the stock has a Moderate Buy consensus rating based on 2 Buys and 2 Holds. The average Globe Life price target of $109 implies 10.7% upside potential from current levels.

Related News:

Winnebago Industries Posts Q4 Beat; Shares Pop 2.4% in Pre-Market

Stride Delivers Upbeat Revenues in Q2; Shares Gain 5% After-Hours

Intuitive Surgical Beats Q2 Earnings Expectations; Shares Rise