Among the major Hong Kong stocks, XPeng, Inc. (HK:9868) recently unveiled its Q1 results for 2024. DBS reaffirmed a bullish stance on the stock in reaction to upbeat first-quarter results. The company reported a narrower-than-anticipated loss for Q1 and forecasted higher sales growth for the second quarter. Year-to-date, XPeng stock has declined 42% due to subdued demand for electric vehicles (EVs) and macro pressures in China. Nonetheless, DBS expects the company’s solid Q1 results and favorable medium-term outlook to support the stock over the near term.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Based in China, XPeng specializes in the design, development, manufacturing, and sales of smart EVs.

Snapshot of XPeng’s Q1 Results

In the first quarter, XPeng achieved revenue of ¥6.55 billion, marking a 62.3% year-over-year rise. However, the top line declined by almost 50% as compared to the previous quarter. The company delivered 21,821 units in Q1, which was 19.7% higher on a year-over-year basis.

The non-GAAP net loss decreased by 36% year-over-year to ¥1.4bn, surpassing expectations. This was primarily attributed to higher-than-anticipated gross margins of 12.9%, compared to 1.7% in the same period last year.

In terms of outlook, XPeng expects its second-quarter vehicle deliveries to be between 29,000 and 32,000 units, reflecting year-over-year growth of 25% to 37.9%. Additionally, Q2 revenues are expected in the range of ¥7.5 billion to ¥8.3 billion.

DBS’ Views on XPeng’s Q1 Performance

Analyst Rachel Miu from DBS noted that Q1 revenue gained from higher volumes and a contribution from the platform and software strategic technical collaboration with Volkswagen AG (DE:VOW).

Further, DBS remains confident about the company’s second brand, MONA, which is targeting the affordable segment to expand its customer base. The first car in this segment is expected to be launched in June, with deliveries anticipated in the third quarter of 2024. The car will be priced between ¥100,000 and ¥150,000, notably lower than XPeng’s previous brand, which was priced at over ¥200,000.

Another catalyst for XPeng stock is its partnership with Volkswagen AG. The collaboration enables the company to benefit from VW’s supply chain capabilities, thereby enhancing cost efficiency.

Miu also highlighted the company’s three-year extensive product launch cycle, which will commence in Q3 2024 and include the rollout of models across major price segments ranging from ¥100,000 to ¥400,000. The analyst noted that XPeng is targeting gross profit margin in the low-to-mid teens level by the end of this year, supported by cost reduction via technology and supply chain efforts.

Overall, with a price target of HK$47.30, Miu sees upside potential in the XPeng share price, fueled by the MONA brand, revenue contribution from the Volkswagen partnership, and a positive medium-term outlook. The analyst said that the price target is under review.

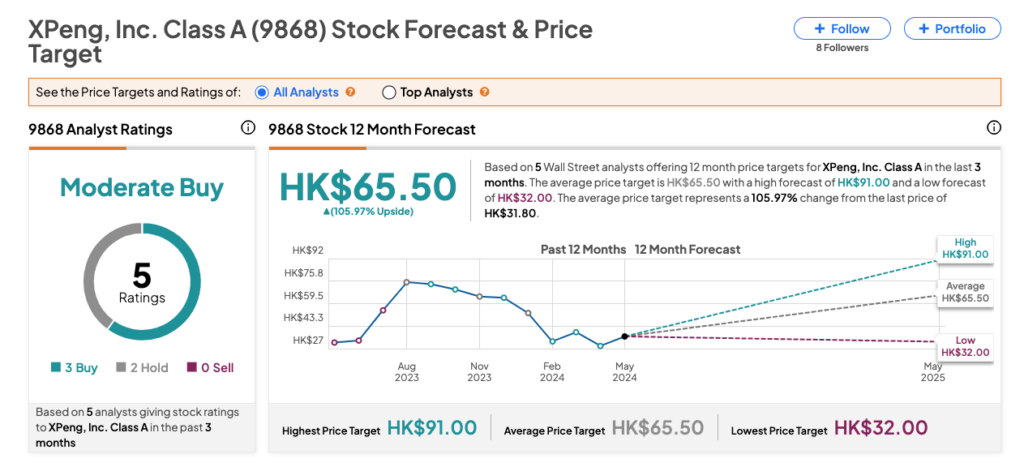

Is XPeng a Good Stock to Buy?

On TipRanks, 9868 stock has received a Moderate Buy consensus rating from analysts based on three Buy and two Hold recommendations. The XPeng share price forecast is HK$65.50, which implies a huge upside of 106% from the current level.