It might surprise some investors that the price of gold has meaningfully outperformed the stock prices of companies that mine gold as their primary business. Logically, one would expect that the cost structure of those companies would make their operations highly leveraged to any rise in the price of gold. However, that hasn’t been the case, as the SPDR Gold Shares ETF (GLD), which approximately tracks the price of the yellow precious metal, has risen about 31% over the past year, 10% more than the VanEck Gold Miners ETF (GDX) and approximately 4.5% more than the VanEck Junior Gold Miners ETF (GDXJ). This article will evaluate the cause of this gap in returns and present why I believe GDXJ is preferred over GDX for those who are waiting for the gold miners to catch up.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

Gold Miners’ Commodity Price Leverage

For the uninitiated, gold miners commonly report what is called the All-In-Sustaining-Cost, or AISC, of their operations. While companies have some leeway in calculating this metric, AISC is intended to represent the total cost of producing an ounce of gold. If a company’s average gold sales price exceeds AISC, it will realize an operating profit. The larger the gap between the price of gold and AISC, the larger that profit would be.

Let’s use a hypothetical example. Suppose I operated a gold-mining firm called JeffGold, with an AISC of $1,600/ounce. At today’s gold price of ~$2,700, I should be earning an operating profit of $1,100/ounce, or about a 41% margin. If the price of gold rose to $3,000, my theoretical operating profit should rise to $1,400/ounce or about a 46.7% margin. In this example, my profit has risen 27.3% from a gold price increase of only 11.1%. That’s the commodity price leverage inherent in profitable mining operations.

Logically, therefore, it stands to reason that gold mining stocks should outperform gold in a rising price environment, but that actually hasn’t been the case (yet). There are likely several reasons for that, including:

- Market participants don’t want to bank on gold staying at its elevated levels

- Concerns that gold miners are likely to bring less profitable projects into production

- Concerns that gold mining companies will lose operational discipline

- Increasing costs associated with the development or acquisition of new mines

Looking at the five biggest public gold miners in the world, only one of them has seen their forward P/E ratio rise over the past year: Agnico Eagle (AEM). As a group, the major gold miners, despite profitability increases, have seen their P/E multiples contract over a period that saw broad market valuation multiples reach almost unprecedented levels. That’s likely due to investor impatience, but also the four concerns listed above.

Evaluating GDXJ versus GDX

The GDXJ ETF, also managed by VanEck, serves as the best-known proxy for junior gold miners. There are no large-cap stocks in this fund, and the company with the largest weight, Alamos Gold (AGI), has a market cap of about $8 billion and currently produces less than 600,000 ounces of gold annually. That’s compared to sector leader Newmont (NEM), which produces more than 6 million ounces per year.

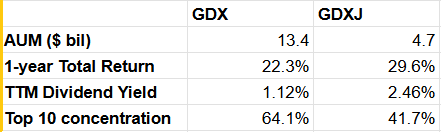

Here are some other select comparative metrics between GDX and GDXJ:

One of the most surprising facts is that GDXJ has actually paid a higher dividend recently, while over a 5-year time horizon, the two ETFs trade off the dividend yield leadership. Smaller miners not only typically have lesser cash inflows to work with but also more difficult access to capital markets. The fact that some junior miners are paying dividends above 5%, such as B2Gold (BTG) is relatively surprising.

The smaller concentration within GDXJ is not surprising. A handful of mega-caps dominate the gold industry and, by relation, the GDX ETF.

My Preference for GDXJ

While I do hold some individual large-cap gold miners, I much prefer GDXJ over GDX. This preference isn’t due to its recent outperformance or its higher dividend. It is related to the lower concentration, but indirectly. GDX shareholders are beholden to capital decision-making by a small number of management teams. Junior gold miners are more likely to be overlooked by capital markets, and when gold prices rise, as they have, it makes those small gold projects look a lot more economically enticing.

The big boys – companies like Newmont, Agnico Eagle, Barrick, and a few others – are more susceptible to going on a spending spree. One of these firms could start a domino effect by acquiring smaller gold projects or mining companies, naturally leading to the others wanting to keep up. Acquisitions could possibly take place at overly rich prices and/or be dependent on gold prices remaining at high levels. One key thing that investors may not realize is that major gold miners generally no longer hedge their exposure to gold. That would make them vulnerable to deteriorating economics on any high-AISC projects they take on.

Junior gold miners are also susceptible to a pullback in the price of gold, of course. My strategy is to either fully or partially hedge that risk. I strongly believe that junior gold miners (as a whole) look good at gold prices north of $2,500/ounce. Investors can place bearish positions against the price of gold as security against any meaningful pullbacks. My preferred vehicle for hedging gold is Shorting the CME Gold Futures, which also allows investors to capture contango gains given the upward-sloping Futures curve.

Source: CME Group

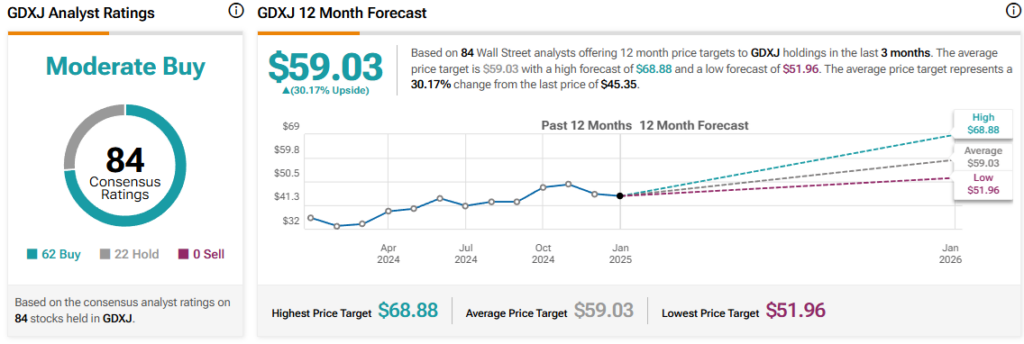

Do Wall Street Analysts Recommend GDXJ?

The VanEck Junior Gold Miners ETF is covered by a large number of Wall Street analysts. Of the 84 who do, they offer GDXJ a total of 62 Buy ratings and 22 Hold ratings. No Wall Street analyst has a Sell rating on this ETF. The average GDXJ price target is $59.03, which represents a potential upside of about 30.2% from the recent market price.

Conclusion

I hold shares of GDXJ and am bullish on the prospects for junior miners. I much prefer this ETF over GDX, which focuses on large gold miners. At current gold prices, I believe the juniors have room to run. As a safeguard, however, I’m hedging against a drop in gold prices by Shorting the Gold Futures traded on the CME.

I’m bullish on GDXJ. Meanwhile, I carry a Hold rating on GDX.